The 2019 market landscape and the challenge ahead

Introduction

In April 2018, the Centers for Medicare and Medicaid Services (CMS) published a revised definition of “primarily health related” (PHR) benefits as applicable to Medicare Advantage (MA) organizations. CMS expanded the definition of a primarily health-related service starting in calendar year (CY) 2019 as one that is “… used to diagnose, compensate for physical impairments, acts to ameliorate the functional/psychological impact of injuries or health conditions, or reduces avoidable emergency and healthcare utilization.” These services are often used by individuals with chronic conditions in need of long-term services and support (LTSS). Many of these services are the same ones that private long-term care (LTC) insurance covers and reimburses.

This article will address how the MA marketplace responded in 2019 to CMS’s expanded definition of primarily health-related benefits, including which supplemental benefits plans are offering and where these benefits are offered. Finally, we will discuss the demand and costs for LTSS-type services among the elderly and the challenges that MA plans may face in developing these benefits.

2019 supplemental benefits under the expanded PHR definition

CMS’s April 27, 2018, guidance letter presented nine possible supplemental benefits that could be offered starting in CY 2019 under the expanded “primarily health-related” definition. We surveyed the approved MA benefit information for all organizations that submitted a CY 2019 bid, as published in CMS.gov,1 and found that many plans are offering some of these supplemental benefits in 2019. The table in Figure 1 shows six of the nine supplemental benefits described in CMS’s memorandum along with the number of plans covering them.

Figure 1: 2019 MA Plans Offering CMS's Suggested Benefits Under Expanded PHR Definition

| 2019 supplemental benefit | Count of plans |

| Adult day care services | 2 |

| Home-based palliative care | 8 |

| In-home support services | 60 |

| Support for caregivers (aka respite care) | 421 |

| Medically approved non-opioid pain management | None found* |

| Standalone memory fitness | None found* |

| *These benefits may potentially be offered as part of a larger package. | |

Although the CMS guidance also included “Home & Bathroom Safety Devices & Modifications” (PBP 14c), “Transportation” (PBP B10b), and “Over-the-Counter (OTC) Benefits” (PBP B13b), we did not include these benefits in our analysis as they are not new to CY 2019. While we were unable to definitively identify plans offering these benefits in CY 2019 under the revised definition, our research showed a significant increase in the number of plans that offered bathroom and safety devices and transportation services in CY 2019.

In addition to CMS’s list of nine potential new benefits under the revised PHR definition, we identified additional “other supplemental benefits” for 2019 that appear to qualify under the expanded PHR definition. We identified these potential benefits based on the descriptions outlined by CMS in its April 2018 guidance. The table in Figure 2 shows the count of MA plans offering these additional benefits in 2019.

Figure 2: 2019 MA Plans Offering New PHR Benefits in Addition to Those Outlined by CMS

| New 2019 Benefit | Count of Plans |

| Activity tracker/fitness tracker | 7 |

| Alzheimer/dementia bracelet: Wandering support service | 3 |

| Backup support for medical equipment | 2 |

| Housekeeping | 1 |

| Non-skilled home health | 8 |

| Personal care/personal care services/personal home care | 47 |

| Restorative care benefit | 4 |

| Social worker line | 91 |

| Supportive care | 5 |

| Therapeutic massage | 1 |

| Vial of Life Program | 10 |

LTSS services in 2019 MA plans

Many of the services in Figures 1 and 2 (such as “respite care” and “personal home care”) are LTSS-type services that qualify under the “primarily health-related” benefit expansion.

We found 577 MA plans that offer LTSS-type benefits in 2019 by searching in the other supplemental benefit descriptions for key words representing LTSS benefits, such as “adult day care,” “in-home support,” and “non-skilled home health.”2 The table in Figure 3 lists the number of MA plans offering LTSS-type benefits in 2019 by plan type.

Figure 3: 2019 MA Plans Offering LTSS-Type Benefits, Count by Plan Type

| Network/ plan type | Non-special needs plans | Dual- eligible SNP | Chronic or disabling condition SNP | Institutional SNP | Total |

| HMO | 340 | 62 | 25 | 6 | 433 |

| LPPO | 91 | 7 | 2 | 0 | 100 |

| HMO-POS | 18 | 3 | 0 | 0 | 21 |

| PFFS | 2 | 0 | 0 | 0 | 2 |

| RPPO | 11 | 4 | 6 | 0 | 21 |

| RPPO | 462 | 76 | 33 | 6 | 577 |

| Note: HMO = health maintenance organization, LPPO = local preferred provider organization, HMO-POS = HMO with place of service benefit, PFFS = private fee-for-service, RPPO = regional preferred provider organization. | |||||

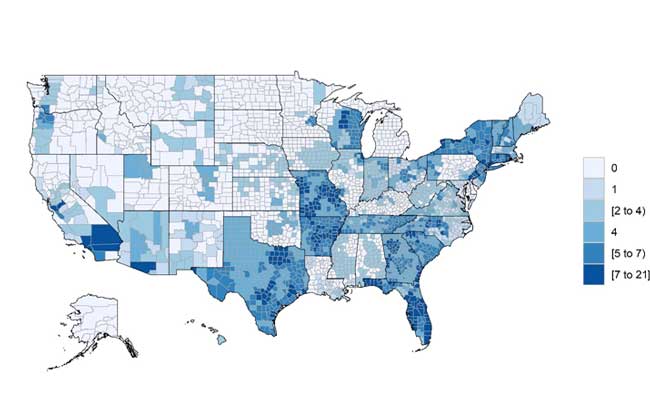

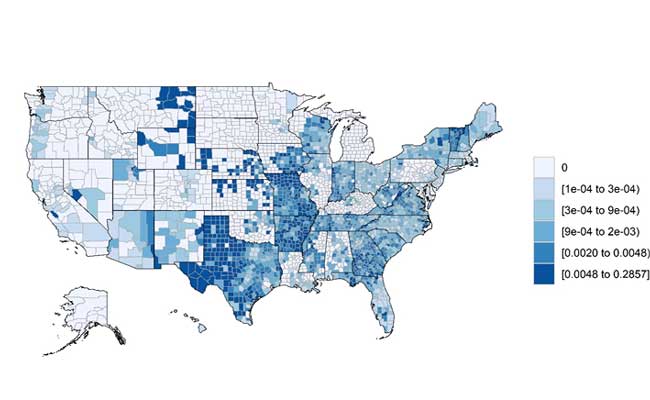

Finally, we show where these plans are concentrated nationwide, illustrating a heat map of the United States. Figure 4 highlights which counties have the most MA plans with LTSS benefits. Figure 5 shows the counties with the highest density of plans offering LTSS-type benefits for each MA-enrolled member as of January 2019.

Figure 4: MA Plans Offering LTSS-Type Benefits, Count by County

Figure 5: Density of MA Plans With LTSS-Type Benefits: Plans Offering LTSS-Type Benefits per MA Member Within Each County

LTSS demands and costs

The benefits approved by CMS for 2019 MA plans cover some of an individual’s long-term support needs. From the MA plan data we surveyed, the benefits offered cover only a small subset of the potential needs of someone requiring long-term custodial care.

More broadly, LTSS encompasses the services and support that individuals may require for their health over a long period of time. These services are most important for individuals who are chronically ill—unable to perform some of their activities of daily living (ADLs3) or who suffer severe cognitive impairment.

How many people are chronically ill in the United States, and what may LTSS services mean to them financially? To understand this we review some nationwide data.

The number of people in the United States expected to need LTSS is growing. In part, this stems from general improvements in population mortality: more people now survive to older ages where they have more LTSS needs. The U.S. Department of Health and Human Services (HHS) estimates that about half (52%) of Americans turning 65 will require long-term care services at some point over the remainder of their lives4 due to limitations with multiple ADLs or severe cognitive impairment. A January 2019 Issue Brief from the Commonwealth Fund5 found that, for Medicare beneficiaries aged 65+, 28% had a “High LTSS need” and 33% more had a “Limited LTSS need,” while only 39% had no LTSS need. Medicare beneficiaries who had income under 200% of the federal poverty line (FPL) or who were eligible for Medicaid had even higher rates of LTSS need.

Research by the Society of Actuaries (SOA) published in 2016,6 based on the National Long Term Care Survey (NLTCS) through 2004, shows that seniors face disability rates that increase by age. The table in Figure 6 shows a selection of disability rates for seniors needing assistance with instrumental activities of daily living (IADLs) such as doing laundry, managing finances, or doing light housework,7 as well as disability rates for seniors needing assistance with one or more ADLs. Note that the tables below show information as of 2004 and for disability triggers specified by the NLTCS.

Figure 6: Disability Group Estimates (%) by Age: NLTCS Age-Standardized to 2004 U.S. Population

| Severity of disability | ||

| Age range | IADL only | 1 or more ADLs |

| 65-74 | 1.79% | 6.22% |

| 75-84 | 2.54% | 15.20% |

| 85+ | 4.23% | 29.92% |

But what costs do the disabled or chronically ill face? For those needing round-the-clock assistance, a semi-private room in a nursing home may cost between $90,000 and $100,000 annually.8 The table in Figure 7 shows the 2018 median annual costs for various levels of LTSS care and the recent annual trend in costs.

Figure 7: Median Annual Costs and Trends of Certain LTSS7

| Description | Annual cost | Annual cost trend |

| Semiprivate room in a nursing home | $89,297 | 3% |

| Home health aide | $50,336 | 3% |

| Care in an adult day healthcare center | $18,720 | 2% |

| Assisted living facility | $48,000 | 3% |

HHS indicates that most of these LTSS services will be funded by out-of-pocket expenditures (55.3%) or through Medicaid (34.2%). Because private LTC insurance premiums are expensive and less healthy individuals will not pass underwriting, only a few insurance-type options are available.

A challenge for MA plans

The LTSS-type benefits that we see MA plans offering in 2019 appear to be more in line with lower-cost benefits such as providing in-home support services or adult day care. Nevertheless, MA organizations need to be aware of the large potential demand for LTSS services. In particular, CMS does not require10 that LTSS-type PHR benefits in MA plans be triggered by the inability to perform ADLs or severe cognitive impairment. While a plan will decide for itself any restrictions on PHR benefits within the rules established by CMS, looser eligibility requirements may imply higher benefit utilization than traditional LTC insurers see.

On January 30, 2019, CMS’s Advanced Notice letter11 laid out expanded MA benefits that plans may offer, labeled “Special Supplemental Benefits for the Chronically Ill” (SSBCI). SSBCI are non-PHR LTSS benefits available to enrollees if the services have a “reasonable expectation of improving or maintaining the health or overall function of the enrollee as it relates to the chronic disease.” Chronically ill enrollees must meet strict criteria,12 but “MA organizations have broad discretion in developing items and services they may propose as SSBCI.”

For people retiring today, financing an LTSS need is a major concern for maintaining adequate retirement funds. Seniors may be looking for new ways to obtain coverage for some of these LTSS benefits. The MA market is slowly expanding coverage to include more LTSS services as seen in the expanded definition of PHR benefits for CY 2019 and the SSBCI starting in 2020. Given the high demand and potential high costs of LTSS-type benefits, MA plans must make careful considerations when offering LTSS coverage as they enter into the 2020 bid season.

1We focused our survey in benefit 13d, e, and f, which are the benefit categories in the plan benefit package (PBP) for "Other supplemental services."

2The complete list of LTSS-type benefits in these data: "Adult Day Care," "Backup Support for Medical Equipment," "Caregiver Services," "Home-based Palliative Care," "In-Home Support," "In-Home Support Services," "Non-Skilled Home Health," "Outside Service Area Benefit," "Palliative Care," "Personal Care," "Personal Care Services," "Personal Home Care," "Restorative Care Benefit," "Supportive Care," and “Supports for Caregivers."

3The six ADLs that trigger most LTC insurance benefits are bathing, continence, dressing, eating, toileting, and transferring.

4HHS (July 1, 2015). Long-Term Services And Supports For Older Americans: Risks And Financing Research Brief. Retrieved February 5, 2019, from https://aspe.hhs.gov/basic-report/long-term-services-and-supports-older-americans-risks-and-financing-research-brief.

5Willink, A., Kasper, J., Skehan, M.E. et al. (January 24, 2019). Are older Americans getting the long-term services and supports they need? Commonwealth Fund. Retrieved February 5, 2019, from https://www.commonwealthfund.org/publications/issue-briefs/2019/jan/are-older-americans-getting-LTSS-they-need.

6Society of Actuaries (July 2016). Long Term Care Morbidity Improvement Study: Estimates for Non-Insured U.S. Elderly Population Based on the National Long Term Care Survey 1984 – 2004. Retrieved February 5, 2019, from https://www.soa.org/Files/Research/Projects/research-2016-06-ltc-morbidity-improvement.pdf (PDF download).

7Society of Actuaries, ibid. A complete list of these IADLs can be found on page 16 in this.

8Genworth. Cost of Care Survey 2018. Retrieved February 5, 2019, from https://www.genworth.com/aging-and-you/finances/cost-of-care.html.

10The April 2018 guidance specifies that the expanded supplemental benefits must “focus directly on an enrollee’s health care needs and be recommended by a licensed medical professional as part of a care plan…”

11CMS (January 30, 2019). Advance Notice of Methodological Changes for Calendar Year (CY) 2020 for Medicare Advantage (MA) Capitation Rates, Part C and Part D Payment Policies and 2020 Draft Call Letter. Retrieved February 5, 2019, from https://www.cms.gov/Medicare/Health-Plans/MedicareAdvtgSpecRateStats/Downloads/Advance2020Part2.pdf.

12A chronically ill enrollee according to the Bipartisan Budget Act of 2018 is one who:

1. Has one or more comorbid and medically complex chronic conditions that is life-threatening or significantly limits the overall health or function of the enrollee

2. Has a high risk of hospitalization or other adverse health outcomes

3. Requires intensive care coordination