Significant changes in the market conditions for pension plans over the past three to five years have substantially decreased unrecognized loss bases on corporate balance sheets, in some cases resulting in an unrecognized gain. Prior to this favorable experience, some plan sponsors have been hesitant to execute de-risking strategies over concerns of the impact of accelerated recognition required under settlement accounting. Our October 2020 Insight, “New audit trends in settlement accounting,” provides a thorough review of the process and trends with the significant market movement during the first six months of the COVID-19 pandemic. Here, we will review the trends over the subsequent five years and what it means for plan sponsors, as well as update on the emerging strategy to enter a buy-in contract at the beginning of the plan termination process and convert it to a buy-out at the end.

Background

Going back to the economic downturn of 2008, followed by over a decade of historically low interest rates, many pension plans became significantly underfunded, creating a drag on companies’ balance sheets and income statements. This came on the heels of many plans being frozen in the early part of the 2000s, often due to concerns of the size of the pension plan(s) relative to the overall size of the company. The rapid rise in Pension Benefit Guaranty Corporation (PBGC) premium rates, combined with large unrecognized losses on the balance sheet, led to difficult decisions when considering de-risking strategies as “hibernation” became significantly more expensive.

Throughout the 2010s, many plan sponsors chose to de-risk in doses to alleviate some of the costs without fully locking in the losses from the 2008 investment losses and subsequent liability losses from declining interest rates. Many plans that weren’t already frozen took the step to freeze accruals. Once frozen, many implemented lump-sum windows for deferred vested participants. This enabled a significant decrease in headcount, saving on fixed-rate premiums, without settling a significant portion of the liability at a low interest rate, as deferred vesteds commonly carry the lowest liability per participant. This strategy also limited the one-time settlement charge due to the low percentage of the overall liability being settled.

Starting in 2022, interest rates began to rise significantly, leading to a corresponding decrease in liabilities. While the stock market underperformed during 2022, most plan sponsors saw their liabilities decrease by more than the plan assets, resulting in being better funded at the end of 2022 compared to the beginning of the year. From the end of 2022 until now, interest rates continued to rise, albeit at a slower pace, but investment markets rebounded and produced double-digit returns in each 2023 and 2024. Not surprisingly, this dynamic led to record transactions in the pension risk transfer space, mostly through plan terminations. With this run of favorable experience, the balance sheet shed much of the unrecognized loss base that built up in the 12-plus years prior and, in some cases, has become an unrecognized gain base.

Financial statements consideration

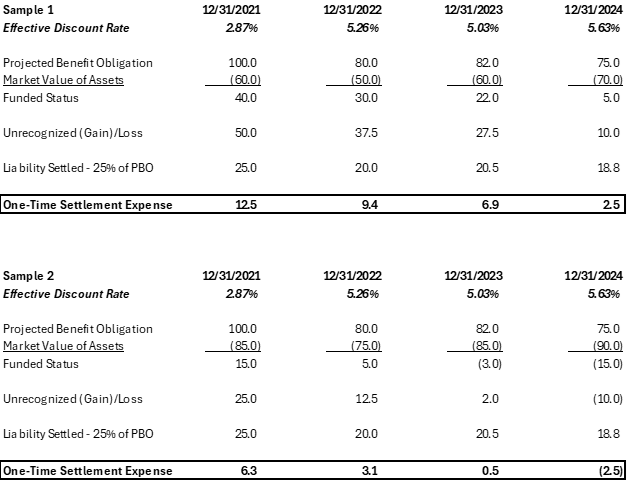

In Figure 1 are two examples of the progression of the one-time settlement expense in each of the last four fiscal years, assuming 25% of the liability is settled through de-risking activities. Note that in Sample 1, the settlement recognition portion of the expense decreased by 80% from fiscal year 2021 to fiscal year 2024, despite the same percentage of liability being settled, due to the decrease in unrecognized losses over this period. Sample 2 shows an instance where the settlement accounting actually produces an acceleration of the unrecognized gain resulting in income.

Figure 1: Two examples of progression of one-time settlement expense in 2023 and 2024

Emerging strategies

Similar to the audit trend discussed in the October 2020 Insight, which detailed the audit trend of recognition of settlement accounting before the threshold of required recognition (“… if the cost of all settlements during a year is greater than the sum of the service cost and interest cost components …” of pension expense, Accounting Standard Codification [ASC] 715-39-35-82), audit firms are considering the proper timing of accelerated recognition of the unrecognized gain/loss related to the population covered by the buy-in contract.

In our May 2022 Insight, “Settlement accounting,” coinciding with the start of the rise in interest rates, the conclusion on timing of settlement accounting remains at the point when the plan sponsor is relieved of the liabilities associated with the annuity contract, e.g., at the point it can be classified as a “buy-out.” Once markets stabilized and absorbed the impact of the interest rate increases, they subsequently produced strong returns in 2023 and 2024. The question then becomes: Does the signing of the buy-in contract reflect an irrevocable action that could be considered a settlement at that time? We continue to monitor auditor opinions on the matter.

Conclusions

If de-risking strategies were considered in the early part of the decade but not executed due to concerns over the impact on the corporate income statement, now might be an ideal time to reconsider taking advantage of the improved status of your plan. Additionally, with the market volatility and the potential of additional federal interest rate cuts on the horizon, locking in termination costs at the beginning of the process with a buy-in contract will protect the current favorable status and lessen volatility caused by changing interest rates and market swings.