This article summarizes the key financial results for medical professional liability (MPL) specialty writers from the second quarter of 2025, marking the 16th consecutive year that Medical Liability Monitor has tracked and published these results. As in prior years, it compares historical second-quarter financial results with full-year figures to provide insight into where 2025 annual results may be headed.

The analysis reflects the collective financial performance of a large group of insurers specializing in MPL coverage. It draws upon 20 years of aggregate statutory financial data compiled by S&P Global Market Intelligence. The current composite includes 170 MPL specialty companies that reported nearly $8.2 billion in direct premium written in 2024.

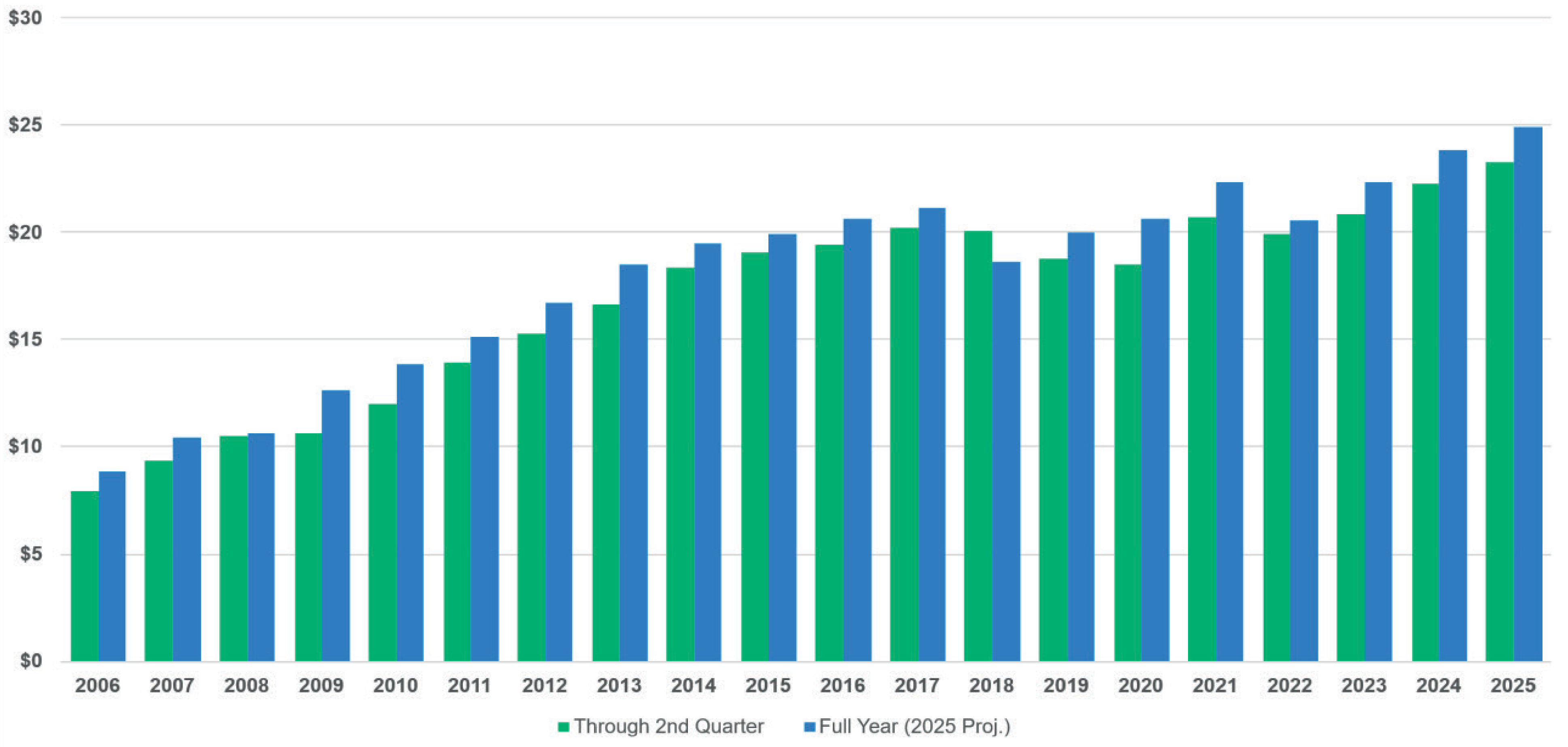

Premium growth continues

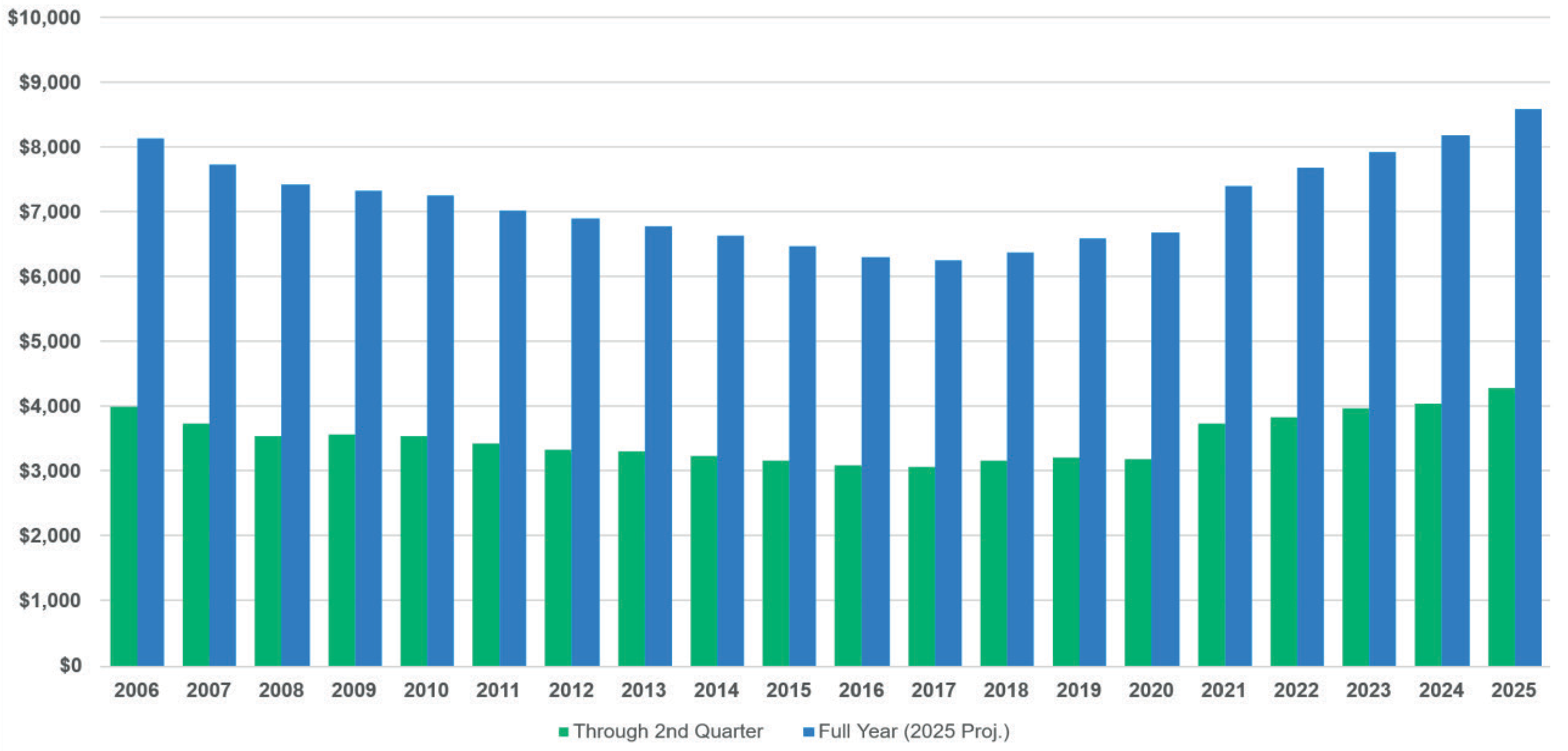

Emulating the first quarter of 2025, second-quarter direct written premium for our composite continued to grow. As shown in Figure 1, second-quarter 2025 premium represents the highest mid-year level in our composite’s 20-year history. Premium growth from mid-year 2024 to mid-year 2025 was approximately 5.8%, the second-largest increase in direct written premium since 2006.

The full-year projection for 2025 anticipates growth will taper off somewhat in the remainder of the year. Even so, our composite’s full-year premium is expected to reach its highest level in two decades, with direct written premiums exceeding $8.5 billion.

Figure 1: Direct written premium — Q2 vs full year ($millions)

Reserve development uncertain

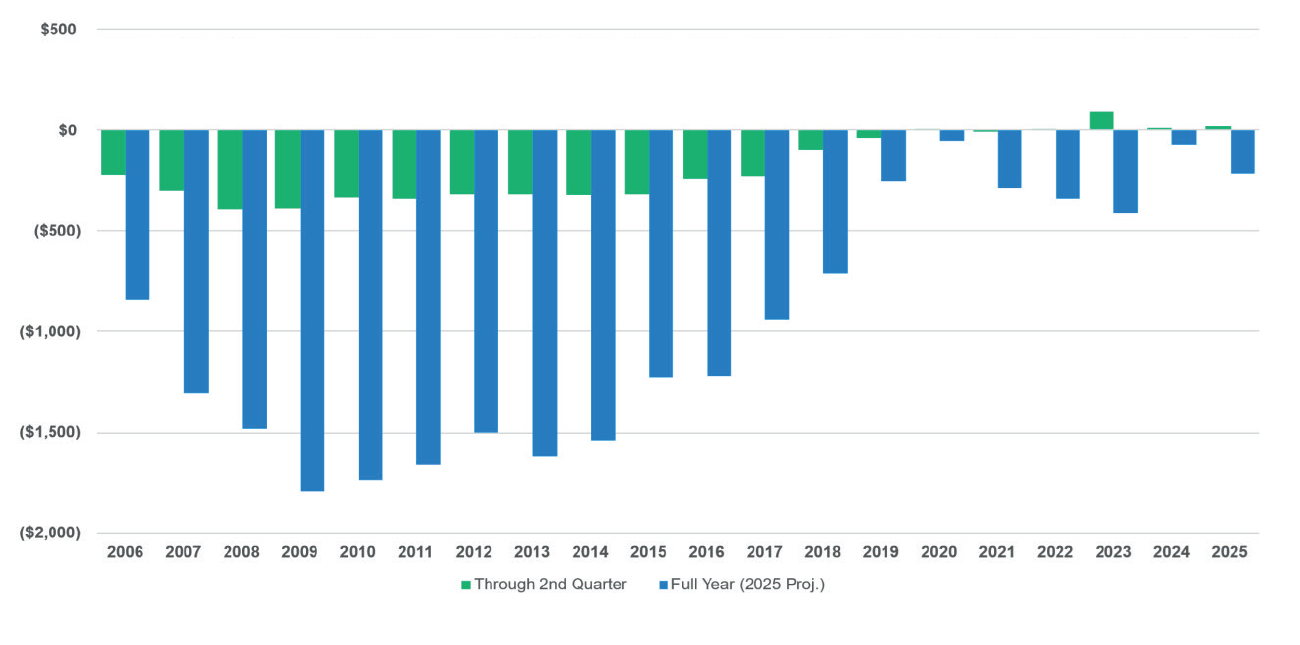

Second quarter 2025 continues the trend of modest adverse one-year reserve development tied to prior years. As shown in Figure 2, our composite recorded a $22 million increase in reserve development through the second quarter of 2025. During the past five years, mid-year reserve development has averaged roughly $21 million in adverse development. It is worth noting that although the past five years reflected minor adverse reserve development at mid-year, the annual results for each of those years were favorable. In a similar fashion, we expect full-year 2025 one-year reserve development to be favorable, though the magnitude remains uncertain.

Figure 2: Cumulative reserve development — Q2 vs full year ($millions)

Underwriting expenses climb

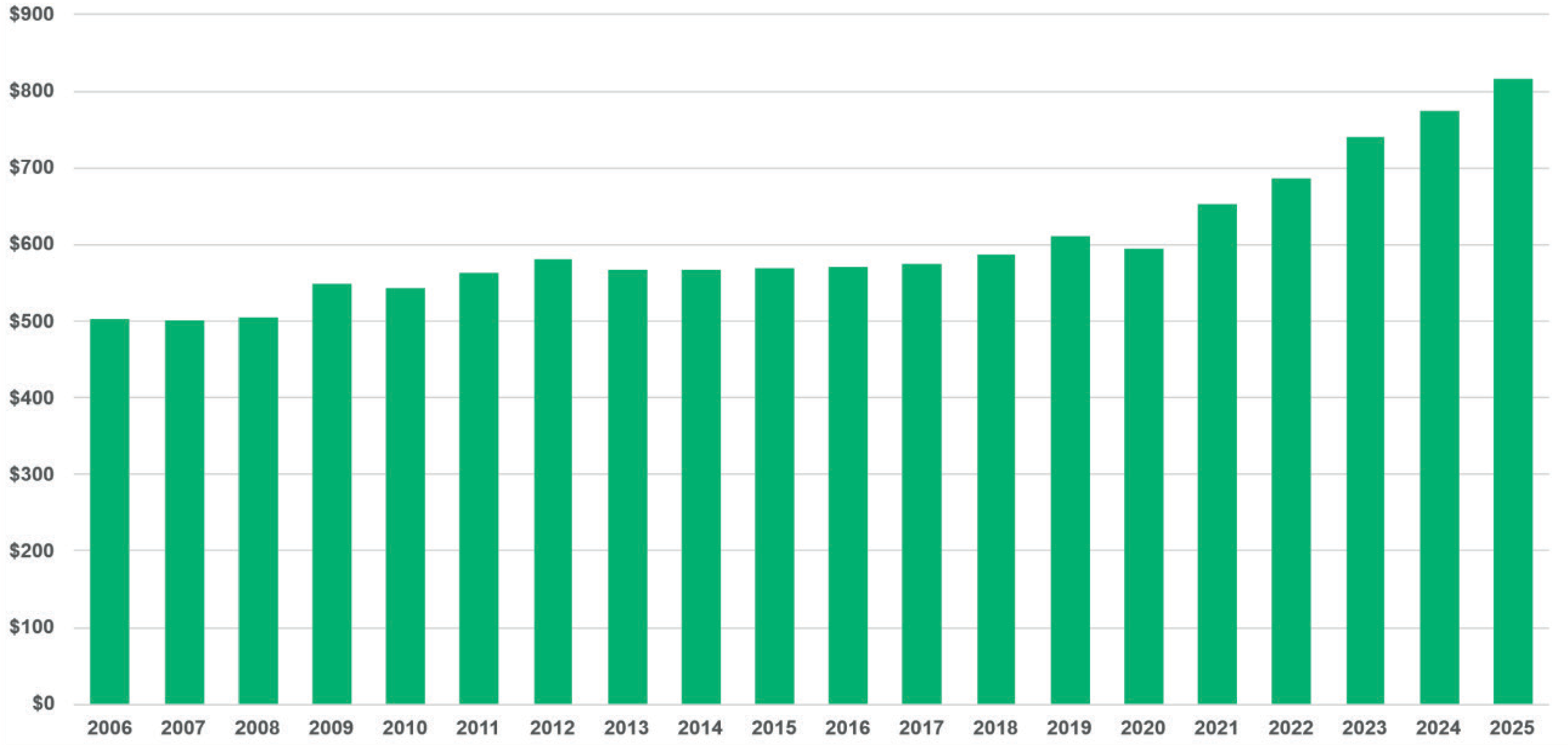

Our composite’s underwriting expenses continued to climb, surpassing $800 million through the second quarter of 2025, as shown in Figure 3. This is more than 40% above the $550 to $600 million range recorded between 2009 and 2018. Since 2019, underwriting expenses have risen an average of 6.5% per year. Elevated inflation has driven up salaries and other underwriting costs, fueling these higher expenses. Expense growth has also outpaced inflation for nearly three years.

Premium growth during the past several years has helped offset rising underwriting costs. The underwriting expense ratio, which compares underwriting expenses to net earned premium, measures the share of premium allocated to underwriting expenses during a given period. As a result, the expense ratio has not grown as sharply as absolute expenses. For the second quarter of 2025, the underwriting expense ratio was 25.3%, slightly higher than the five-year average of 24.6%.

Figure 3: Underwriting expenses ($millions) through Q2

Indemnity payments escalate

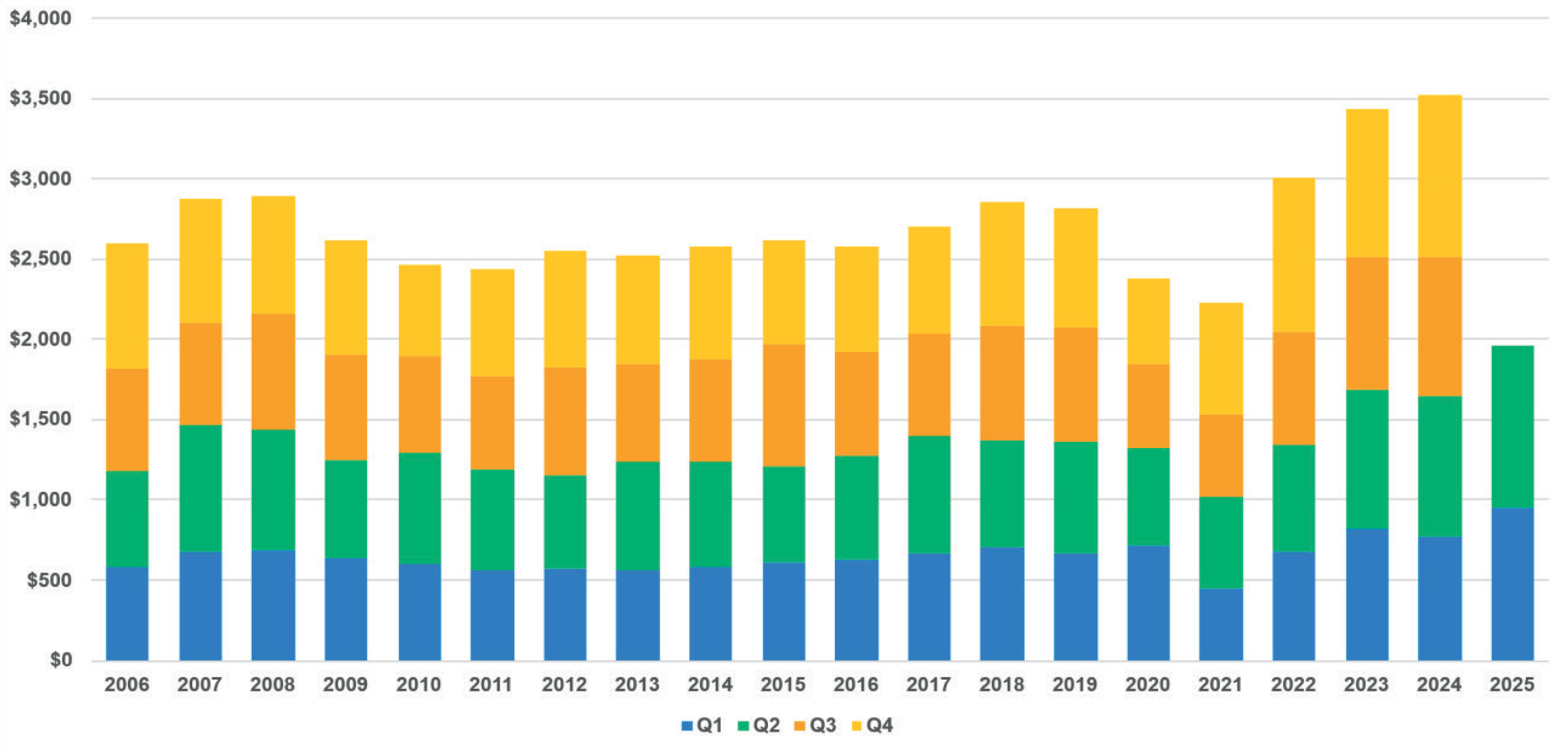

Indemnity payments for our composite continued to rise through the second quarter of 2025. As shown in Figure 4, COVID-19 court closures caused a prolonged slowdown in indemnity payments across 2020 and 2021. Since then, payments have not only rebounded but surged, with 2025 marking record highs. The first two quarters of 2025 produced the largest payments for the first half of any year in our composite’s 20-year history. Indemnity payments of more than $1.95 billion in the first two quarters represent an almost 20% year over-year increase compared to the same period in 2024.

COVID-19 court closures also created a backlog of open claims and contributed to longer claim duration, a trend that has yet to be fully resolved. Claim duration remains a critical factor for MPL companies, as its recent extension has lengthened reporting and payout patterns, potentially increasing claim severity. In addition, sustained economic and social inflationary pressures will continue to drive claim costs higher. The industry must closely monitor financial stability and regularly reassess pricing strategies to manage these higher indemnity costs.

Figure 4: MPL direct paid losses ($millions)

Policyholder surplus reaches new heights

As shown in Figure 5, the composite’s policyholder surplus grew more than 4% year-over-year in the second quarter of 2025, reaching approximately $23.3 billion, the largest surplus in the composite’s history. This is nearly three times higher than the second-quarter surplus of $7.9 billion in 2006, the earliest point in our 20-year review.

Figure 5 also indicates the composite’s full-year 2025 surplus will finish even higher, approaching $25 billion. Increased premiums collected from policyholders (Figure 1), modest reserve releases (Figure 2) and strong investment returns appear to be outpacing the rising expenses shown in Figure 3 and the indemnity payments in Figure 4.

Figure 5: Policyholders surplus — Q2 vs. full year ($billions)

Conclusion

Our composite’s financial performance through the second quarter of 2025 reflects resilience and growth. Record direct written premiums and policyholder surplus underscore the industry’s strong momentum. Premium increases have helped offset rising underwriting expenses, yet persistent upward trends in both underwriting costs and indemnity payments continue to pose challenges. Despite modest adverse reserve development remaining a concern, historical patterns suggest the potential for favorable full-year results.

Looking ahead, MPL insurers must stay vigilant, regularly reassessing pricing and claims strategies to maintain financial stability in a shifting risk environment.

The previous edition of this series can be read here, and the next quarter's edition can be found here.

Eric Wunder is a principal and consulting actuary, and Sarah Rice is an associate actuary, at Milliman Inc., an independent actuarial and consulting firm.

This article first appeared in the September 2025 issue of Medical Liability Monitor: http://www.medicalliabilitymonitor.com/.