California Assembly Bill (AB) 1048 requires that, as of January 1, 2025, dental insurers must submit rate filings for commercial dental products under the jurisdiction of the California Department of Managed Health Care (DMHC) or the California Department of Insurance (CDI).1 As we worked with clients over the first filing cycle, we have uncovered important details and some surprises. Here we share the basics of the new law, along with lessons learned that are critical for dental insurers to understand to stay compliant and ensure premium rates can be changed when needed.

The basics

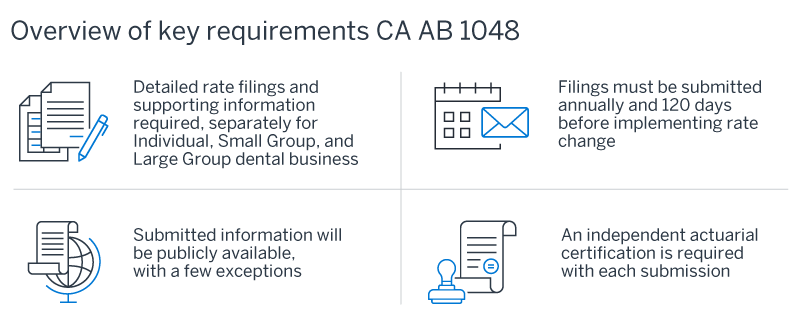

- Lots to share. Filings must include “information regarding the methodology, factors, and assumptions used to determine rates.”2 Standardized “Dental Rate Review” templates must be completed, requiring not just rating methodology and the rate change requested but also in-depth supporting data including number of policies and enrollment, California and nationwide experience, per member per month (PMPM) administrative cost detail including any proposed changes, trend assumption development, and more. Separate filings must be submitted for individual, small group, and large group business.

- This is only the beginning. Filings must be submitted annually, even if no rate changes are being requested. In addition to the annual process, a filing must be submitted at least 120 days before implementing any change in the methodology, factors, or assumptions that would affect rates.

- For everyone’s eyes. The DMHC and CDI (the departments) will make submitted information publicly available except for contracted rates between a health plan or insurer and provider and contracted rates between a health plan or insurer and group pursuant to Health and Safety Code section 1385.07 and Insurance Code section 10181.7.

- Check my work. An independent actuarial certification attesting to rating methodology soundness is required with each submission.

Lessons we learned so you don’t have to

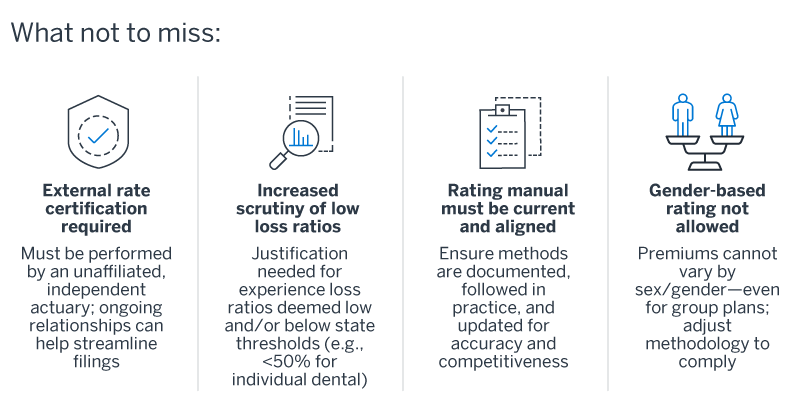

- “Independent actuarial certification” means external to your company. The independent actuarial certification must be from a qualified actuary who, per California law, “must not be affiliated with, a subsidiary of, owned by, or controlled by a health insurer or a trade association of health insurers.” To our knowledge this is the first state to require a certification of dental rate filings beyond that of the company’s own actuary. Though an independent certification requirement has been in place for California health plans for some time, the application to dental plans took many dental insurers by surprise. You will need to engage an actuary outside your company to review and certify your annual filings as well as any interim rate change filings; having an ongoing relationship with an independent actuary who can maintain familiarity with your rate manual and book of business can make the certification process more straightforward year-to-year.

- New rate filing requirements mean increased scrutiny of loss ratios. While mandated annual dental loss ratio reporting has been in place for years in California, this new filing process pairing historical experience with rating methodology has resulted in the departments requesting justification for blocks of business with low loss ratios. Some dental carriers have longstanding or even closed blocks of business for which premium rates have been renewed at a rate pass or trend increase for years, and experience loss ratios may be below what the departments consider reasonable. For individual dental, state reviewers have referred to California Insurance Code Title 10 California Code of Regulations (CCR) Section 2222.12(c), which indicates that “benefits provided by supplemental policies of individual health insurance that provide coverage for…dental care expenses only…shall be deemed to be reasonable in relation to premiums if the lifetime anticipated loss ratio is not less than 50%.”3 Insurers may need to work with the state’s reviewers to implement changes to move loss ratios upward over time.

- A solid rating manual is a must. As dental rate filings were not previously required in California, some insurers had outdated, poorly (or un!)documented rate manuals and/or presale and renewal rating processes that no longer aligned with the manuals they did have. The first iteration of filing rates under this new law has forced a shoring-up of manual rating methodology and ensured that the methods are followed in the sales and underwriting process. It also presents an opportunity for carriers to take a good look at their manual rates and make potentially overdue updates and improvements to base claim costs, rating factors, and other assumptions to enhance rating accuracy and competitiveness.

- Rating by gender is not permitted. Many dental insurers were surprised to receive objections from the departments related to manual rating factors differentiating rates by gender. California Insurance Code Section 10140.2 prohibits any premium differentials based on sex or gender4; according to the state’s reviewers, this applies even for group premium rate development, where the underlying use of gender factors is still considered noncompliant. Again, due to the prior lack of a rate filing requirement, some insurers had been unaware that using standard gender factors that are commonly part of dental rating is not allowed in California. The need to adjust methodology to be gender-neutral presents another opportunity to take a fuller review of your dental manual rating process and identify other areas that may need a refresh.

Getting ahead of the game for 2026 and beyond

The law was effective at the beginning of this year, but the amount of work required to compile the rate filing packages, understand the new template and process, and respond to state objections has caused the 2025 rate approval cycle to be prolonged and indeed still be ongoing for many companies. For carriers that want to change premium rates for 2026 due to emerging experience, a revamping of their manual rating process, or any other reason, time is of the essence to file a new package of information so that rates can be approved and implemented on the desired effective date. Understanding the process, the focus areas of the state, and what is and is not permissible will be critical for dental insurers to make future iterations of the filing process smoother and ensure compliant, competitive rate-setting.

1 The full text of California AB 1048 is available at https://legiscan.com/CA/text/AB1048/id/2841730.

2 All PLan Letter 24-014. Department of Managed Health Care. https://www.dmhc.ca.gov/Portals/0/Docs/OPL/APL%2024-014%20%20Guidance%20Regarding%20Dental%20Rate%20Review%20Reporting%20Requirements%20(7_8_2024).pdf?ver=_X0rKf2HCbqC7OjcrHuuCA%3D%3D.

3 The full text of CCR Section 2222.12(c) is available at https://www.law.cornell.edu/regulations/california/10-CCR-2222.12.

4 The full text of California Insurance Code Section 10140.2 is available at https://law.justia.com/codes/california/code-ins/division-2/part-2/chapter-1/article-2-5/section-10140-2/.