The U.S. Securities and Exchange Commission (SEC) has amended the executive compensation reporting requirements for proxy statements for fiscal years ending on or after December 16, 2022. The rules require the inclusion of a new table, intended to present a more accurate description of executive compensation. Additional information will be needed for any executives who actively participate in one or more defined benefit (DB) pension plans.

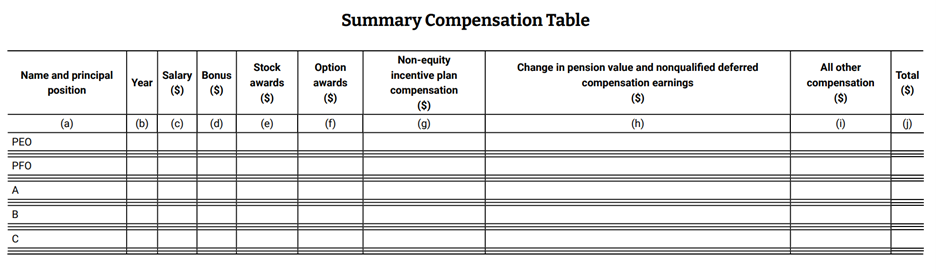

The current rules under Title 17, Chapter II of the Code of Federal Regulations require the inclusion of the change in the present value of accumulated benefits for the past three years in column (h) of the Summary Compensation Table (§229.402(c)), along with a separate Pension Benefits table (§229.402(h)). These amounts are to be provided for the following Named Executive Officers (NEOs):

- The Principal Executive Officer (PEO)

- The Principal Financial Officer (PFO)

- The three most highly compensated NEOs (other than the PEO and PFO) who were serving as executive officers at the end of the last completed fiscal year

- Up to two additional NEOs who would have been required to be reported, but for the fact that they were not serving as an executive officer at the end of the last completed fiscal year

Figure 1: Summary Compensation Table standard layout

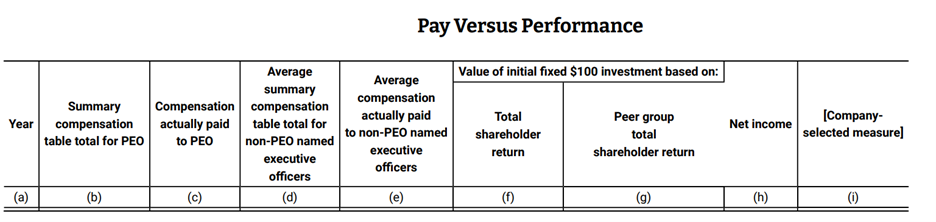

These requirements remain unchanged, but a new paragraph, §229.402(v), was added that requires the inclusion of a Pay Versus Performance table. This table takes the total compensation from the Summary Compensation Table (which includes the change in the present value of accumulated pension benefits) and adjusts it in order to develop a new item (“Compensation Actually Paid”). These adjustments are to:

- Reduce the total compensation by the aggregate change in the actuarial present value of accumulated benefits under all defined benefit and actuarial pension plans reported in the Summary Compensation Table, per §229.402(v)(2)(iii)(A).

- Increase, for all defined benefit and actuarial pension plans reported in the Summary Compensation Table, the total compensation by the sum of the service cost and prior service cost, per §229.402(v)(2)(iii)(B).

- Perform other compensation adjustments, as outlined in §229.402(v)(2)(iii)(B).

Figure 2: Pay Versus Performance table standard layout

For the PEO, the total amount from the Summary Compensation Table is shown in column (b), and the “Compensation Actually Paid” will appear in column (c). For the remaining NEOs (excluding the PEO), the calculations are performed in the same manner, except the table only requires that the average amount for these NEOs be reported. These amounts are to be reported in columns (d) and (e). The rules require a footnote that contains the names of the NEOs used in the averaging calculations, and the fiscal years for which they are included.

The service cost is calculated as the actuarial present value of each NEO’s benefit under all defined benefit and actuarial pension plans reported in the Summary Compensation Table attributable to services rendered during the covered fiscal year. The prior service cost is calculated as the entire cost of benefits granted (or credit for benefits reduced) in a plan amendment (or initiation) during the covered fiscal year that are attributed by the benefit formula to services rendered in periods prior to the amendment.

The service cost and the prior service cost must be calculated using the same methodology as used for the registrant's financial statements under generally accepted accounting principles.

The “Compensation Actually Paid” amounts in the Pay Versus Performance table are required to be provided for the past three years (except for smaller reporting companies). The table will be expanded to require up to five years of history in future proxy statements. In addition to this, in the event that there are multiple PEOs within a fiscal year, the Pay Versus Performance table would need to be expanded to provide information for each of the PEOs.

Your Milliman consultant is available to assist you with this compliance for upcoming proxy statements.