Among the key rating classifications for Medicare Supplement (MedSupp) business is attained age-based rate adjustments as reflected in the premium rate schedule.1 However, this classification can become neglected as a key component of rate structure alignment and an area of opportunity for new market entrants as well as existing carriers. This article delves into the theoretical actuarial considerations and the areas of opportunity in the market today.

Theoretical perspective

Historical claims data, not to mention general rationale, support the understanding that medical claims generally increase with age.2 However, the rate of increase varies from one age to another as well as the underlying benefit structure (i.e., plan option). Each of the 11 standardized plan options is unique in the underlying coverage it provides beneficiaries as a result of the various Medicare out-of-pocket obligations in the form of deductibles, copays, and coinsurance.3 The change in claim cost by age (referred to as age slope or “slope” in this paper) for total allowed charges will be different from the slope for MedSupp Plans due to “deductible leveraging,” a concept explained in the example below.

Assume that the underlying medical benefit claim cost per member per month (PMPM) is expected to increase from $100 at age 70 to $105 at age 71, a 5% increase. However, if a fixed deductible of $10 PMPM (assumed claim cost value for both ages) is introduced, the benefit change increases from $90 ($100 - $10) to $95 ($105 - $10), a higher increase of 5.6%. The introduction of a deductible serves to steepen the slope. The greater the proportional value of the deductible, the greater the leveraging impact.

Based on this deductible leveraging concept, this paper focuses on Plan G and high-deductible Plan F as two primary examples, with the potential implications for the market today.4

Market considerations: New entrants and existing carriers

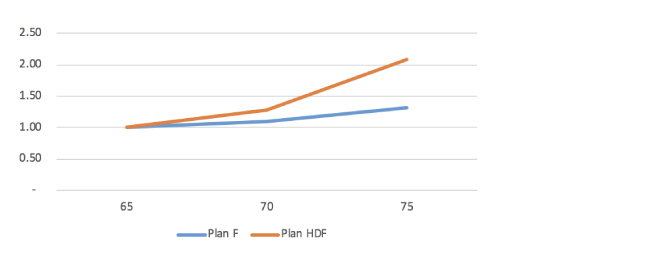

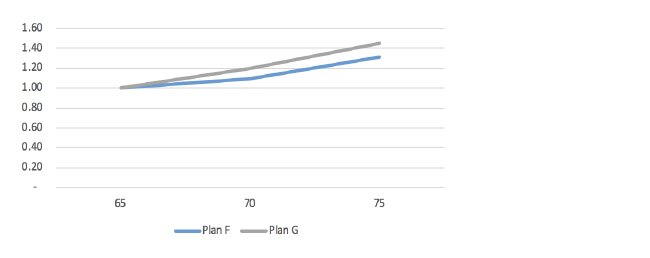

Continuing the discussion of slope with a focus on Plan G, Plan F, and high-deductible Plan F (Plan HDF) practical applications, Figure 1 provides an example of expected claim cost slopes relative to age 65 for Plan F, Plan HDF, and Plan G for two sample ages relative to age 65 (1.000).5 The charts in Figures 2 and 3 provide a visual representation to get a sense of true differences. Note that slopes to other ages may not necessarily be linear and that, in practice, this evaluation and/or analysis would consist of multiple key ages.

Figure 1: Expected Claim Cost Slopes

| Age | Plan F | Plan HDF | Plan G |

| 65 | 1.00 | 1.00 | 1.00 |

| 70 | 1.10 | 1.29 | 1.20 |

| 75 | 1.32 | 2.08 | 1.45 |

Figure 2: Expected Claim Cost Slopes

Figure 3: Expected Claim Cost Slopes

These charts show the impact and relative significance of deductible leveraging of these different plan designs. The Plan G slope reflects a $185 Part B deductible while the Plan HDF slope is reflective of an upfront $2,300 deductible.

A rate schedule with age slopes consistent with the expected claim slopes has advantages such as the following:

- Internal rate consistency and alignment that reflects the underlying risk and removes subsidization between ages and the risk that subsidization brings. A primary risk is vulnerability to shifts in age distribution away from original expectations brought about by subsidization, where more competitive but less profitable rate cells, subsidized by less competitive but more profitable rate cells, end up representing a higher proportion of the total than might originally be expected.

- In the case of Plan G and Plan HDF, reflecting the steeper slope in the rate schedule (relative to Plan F) allows for more competitive rates at the younger ages (as noted above), particularly the typical target market of ages 65 to 67, while still pricing for overall required rate levels.

Leading carriers in the market may use uniform rate slopes across all plans. However, it is rare to find Plan HDF rate slopes close to the expectations of claim costs for that plan. The rate slope approach typically used in the market provides opportunities for new market entrants as well as considerations for existing MedSupp carriers:

- For new entrants, there is the opportunity to market premium rates at relatively more competitive levels at the lower ages.

- Existing carriers can incorporate this approach into overall rate change strategies.

- For Plan HDF, this phenomenon is magnified. However, carriers must also consider corporate profit objectives in light of fixed expenses, with the challenge of current age 65 market rates already set significantly below $100 PMPM

Other considerations and specific processes dealing with regulatory considerations are beyond the scope of this article.

Conclusion

Whether you are a new entrant in the product development stage or an established carrier evaluating plan performance and alternatives, a diligent management strategy should include recognition of the rate slope when compared against the market and expected claim levels.

Limitations

This information is presented for demonstration purposes only.

Guidelines issued by the American Academy of Actuaries require actuaries to include their professional qualifications in actuarial communications. I, Kenneth L. Clark, am a consulting actuary for Milliman, Inc. and am a member of the American Academy of Actuaries. I meet the qualification standards of the American Academy of Actuaries to render the analysis contained herein.

The opinions expressed in this article are those of the author alone and do not necessarily reflect the opinions of Milliman or other employees of Milliman.

1 Note that some states require an issue age rate structure. This is beyond the scope of this publication.

2 This may not always be the case, especially at ages 65 and 66, due to potential pent-up demand for medical services upon receiving Medicare coverage with subsequent flat or reduced service use at age 66.

3 Medicare. How to Compare Medigap Policies. Retrieved July 3, 2019, from https://www.medicare.gov/supplements-other-insurance/how-to-compare-medigap-policies.

4 A high-deductible Plan G will be introduced in 2020 and we may expect the characteristics with respect to slope to be similar to high-deductible Plan F.

5 Based on internal research, assuming a split of 55% female and 45% male applied to gender-specific expected claim costs.