Many investors have been anticipating a new era of low returns given years of surging asset prices. With the advent of coronavirus, which is wreaking havoc on markets (and toilet paper supplies), those predictions may be about to come true.

In such a low-return environment, the impact of small investment fees is about to get a lot bigger.

It's been all too easy to ignore fees when markets surge ahead, as they have done in recent years. A 0.5 percentage point fee eats up just 5% of a 10% annual investment return1.

But now that major share markets have posted double-digit falls from late February to early April, the full impact of fees may be exposed. That same 0.5 percentage point investment fee eats up 50% of a 1% annual return.

A correlation between low fees and performance

Consumers tend to buy higher-priced goods or services because they convey some benefit over the cheaper-priced alternative. But in funds management, that theory is turned on its head: higher-priced products often underperform their lower-priced rivals.

An analysis by the Productivity Commission found two out of three MySuper products that charged the highest fees (above 1.5%) were also ranked among the worst underperforming default products between 2008 and 20182.

This finding has also been replicated across different types of fund products. For example, actively managed mutual funds with relatively high expense ratios were associated with some of the worst performing U.S. equity managed funds, according to another recent analysis3.

A key reason is not just the level of fees, but their structure.

Massive index funds with enormous scale have allowed investors to gain market exposure at incredibly low cost. But for many actively-managed products, the base fee is still well above those levels – and base fees are charged whether outperformance eventuates or not.

Meeting the best interests duty

This is not to say that advisers should automatically choose index funds or others with the lowest fee or in order to meet their best interests duty, which requires benefits to be clearly identified and quantified.

ASIC's Regulatory guide 175 specifically acknowledges that, when taking into account all of a client's needs, a higher fee option can still satisfy the best interests duty. It gives an example of a client who wants better platform reporting and is prepared to pay 0.1% higher fees for that benefit.

However, it is harder to assume that a client will benefit from a substantially higher-fee fund when outperformance waxes and wanes. A fee increase of just 0.5% can cost a typical full-time worker about 12% of their final superannuation savings (or $100,000) by the time they reach retirement, according to the Productivity Commission4.

That is a substantial hurdle to justify, particularly in an environment where returns are expected to be lower for longer5.. These are difficult decisions, particularly given a greater focus on fiduciary standards and enforcement following the financial services Royal Commission.

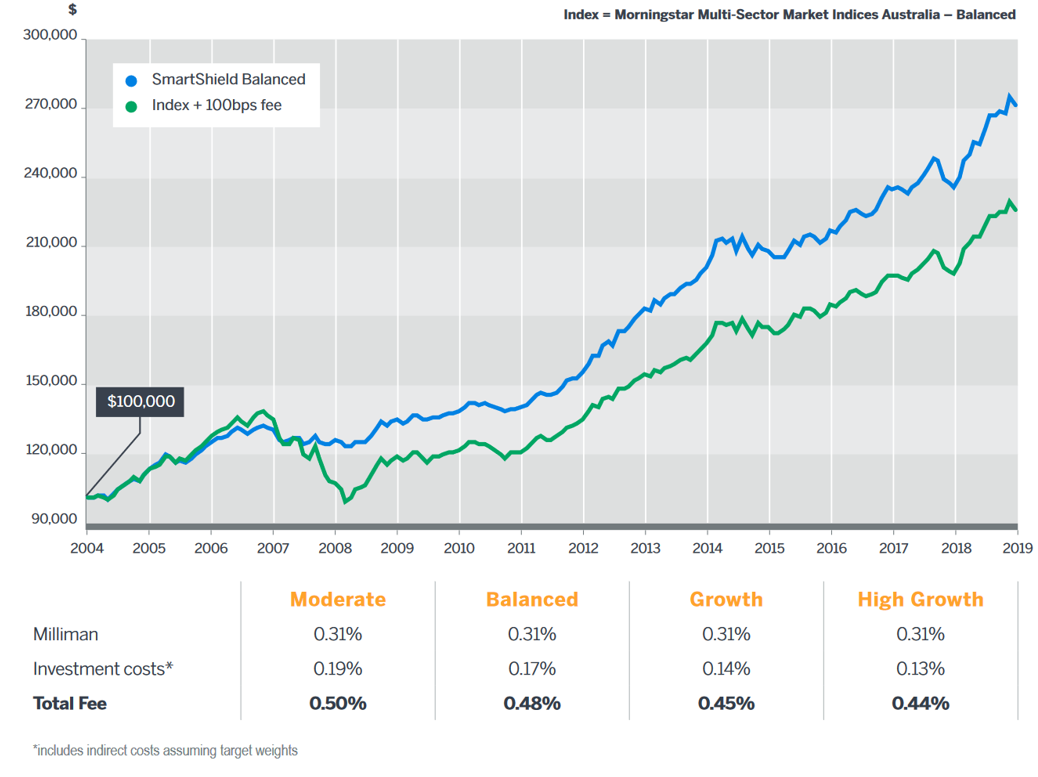

But focusing on the potential impact of fees makes it easier to demonstrate that advice is helping to meet a client's goals. For example, a back test of Milliman's recently launched SmartShield Balanced managed account shows significant outperformance against benchmark. Low fees around half the level of rival funds are a key reason.

What is value?

While fee levels are crucial determinants of investment outcomes, price does not always equal value6. and, as ASIC acknowledges, a higher fee can still be appropriate if it can be shown that the product or service better suits the needs of the client.

A myopic focus on fees can create a race to the bottom and even perverse outcomes such as negative fees. Some things are worth paying for – the trick is working out what.

Value is something that is personal and should be defined by each client, rather than dictated by the industry. An underrated skill of advisers is their ability to blend client interviews, data, and analysis to discern the answer.

At Milliman, we believe in giving advisers a bigger toolkit to meet clients’ needs without excessive costs. For example, the fee charged by our SmartShield managed accounts also includes a risk protection overlay that dampens volatility and the impact of sustained market downturns. It uses exchange-traded derivatives rather than higher-cost options and can be switched on or off without incurring capital gains tax.

Now, more than ever, it is important to evaluate that fees are delivering value. In a low return environment, making sure clients get what they pay for is essential for compliance and competition.

You can find more information about the Milliman SmartShield range at https://advice.milliman.com/en/smartshield.

Disclaimers

This document has been prepared by Milliman Pty Ltd ABN 51 093 828 418 AFSL 340679 (Milliman AU) for provision to Australian financial services (AFS) licensees and their representatives, and for other persons who are wholesale clients under section 761G of the Corporations Act.

To the extent that this document may contain financial product advice, it is general advice only as it does not take into account the objectives, financial situation or needs of any particular person. Further, any such general advice does not relate to any particular financial product and is not intended to influence any person in making a decision in relation to a particular financial product. No remuneration (including a commission) or other benefit is received by Milliman AU or its associates in relation to any advice in this document apart from that which it would receive without giving such advice. No recommendation, opinion, offer, solicitation or advertisement to buy or sell any financial products or acquire any services of the type referred to or to adopt any particular investment strategy is made in this document to any person.

The information in relation to the types of financial products or services referred to in this document reflects the opinions of Milliman AU at the time the information is prepared and may not be representative of the views of Milliman, Inc., Milliman Financial Risk Management LLC, or any other company in the Milliman group (Milliman group). If AFS licensees or their representatives give any advice to their clients based on the information in this document they must take full responsibility for that advice having satisfied themselves as to the accuracy of the information and opinions expressed and must not expressly or impliedly attribute the advice or any part of it to Milliman AU or any other company in the Milliman group. Further, any person making an investment decision taking into account the information in this document must satisfy themselves as to the accuracy of the information and opinions expressed. Many of the types of products and services described or referred to in this document involve significant risks and may not be suitable for all investors. No advice in relation to products or services of the type referred to should be given or any decision made or transaction entered into based on the information in this document. Any disclosure document for particular financial products should be obtained from the provider of those products and read and all relevant risks must be fully understood and an independent determination made, after obtaining any required professional advice, that such financial products, services or transactions are appropriate having regard to the investor's objectives, financial situation or needs.

All investment involves risks. Any discussion of risks contained in this document with respect to any type of product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved. Investing in foreign securities is subject to greater risks including: currency fluctuation, economic conditions, and different governmental and accounting standards. There are also risks associated with futures contracts. Futures contract positions may not provide an effective hedge because changes in futures contract prices may not track those of the securities they are intended to hedge. Futures create leverage, which can magnify the potential for gain or loss and, therefore, amplify the effects of market, which can significantly impact performance. There are also risks associated with investing in fixed income securities, including interest rate risk, and credit risk.

An investment in an underlying portfolio, whether with or without Milliman Managed Risk Strategy (MMRS) is subject to market and other risks and no guarantee or assurance is given by Milliman AU or any company in the Milliman group that the use of MMRS in connection with an underlying portfolio will not give rise to losses or that the performance of the MMRS in relation to the underlying portfolio will remove volatility completely or to the extent depicted in an illustration or fully replace losses in the underlying portfolio or to the extent depicted. While generally assets used in connection with the MMRS are liquid, this may not be the case in all circumstances. Further, during periods of sustained market growth, the return to clients from the combination of an underlying portfolio and MMRS should be less than if a client had no MMRS.

Any source material included in this document has been sourced from providers that Milliman AU believe to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by any company in the Milliman group as to the accuracy or completeness of the source material or any other information in this document.

Past performance information provided in this document is not indicative of future results and the illustrations are not intended to project or predict future investment returns.

Any index performance information is for illustrative purposes only, does not represent the performance of any actual investment or portfolio. It is not possible to invest directly in an index.

Any hypothetical, backtested data illustrated herein is for illustrative purposes only, and is not representative of any investment or product. RESULTS BASED ON SIMULATED OR HYPOTHETICAL PERFORMANCE RESULTS HAVE CERTAIN INHERENT LIMITATIONS. UNLIKE THE RESULTS SHOWN IN AN ACTUAL PERFORMANCE RECORD, THESE RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, BECAUSE THESE TRADES HAVE NOT ACTUALLY BEEN EXECUTED, THESE RESULTS MAY HAVE UNDER-OR OVER-COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED OR HYPOTHETICAL TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THESE BEING SHOWN. For any hypothetical simulations illustrated, Milliman AU does not manage, control or influence the investment decisions in the underlying portfolio. The underlying portfolio in hypothetical simulations use historically reported returns of widely known indices. In certain cases where live index history is unavailable, the index methodology provided by the index may be used to extend return history. To the extent the index providers have included fees and expenses in their returns, this information will be reflected in the hypothetical performance.

1 Such returns have become common due to central bank accommodative policy. The S&P/ASX 200 posted total annualised returns of 9.33% over the five years to January 31, 2020. The MSCI World Ex Australia (AUD) posted 12.44% annualised return over the same period.

2Productivity Commission Inquiry Report: Superannuation: Assessing Efficiency and Competitiveness, December 2018. p179. Retrieved from https://www.pc.gov.au/inquiries/completed/superannuation/assessment/report.

3Horstmeyer, D. (2019). Double Whammy: High-Fee Mutual Funds Do Worse. WSJ. Retrieved fromhttps://www.wsj.com/articles/double-whammy-high-fee-mutual-funds-do-worse-11546630477.

4Productivity Commission Inquiry Report: Superannuation: Assessing Efficiency and Competitiveness, December 2018. p179. Retrieved from https://www.pc.gov.au/inquiries/completed/superannuation/assessment/report.

5For example, the Reserve Bank of Australia warned in its October 2019 Financial Stability Review that "Financial market compensation for risk remains low despite the greater chance of weak global growth." Retrieved from https://www.rba.gov.au/publications/fsr/2019/oct/.

6Or, as Warren Buffett has said: “Price is what you pay. Value is what you get.”