This article summarizes key financial results for medical professional liability (MPL) specialty writers from the first quarter of 2025, marking our 16th consecutive year tracking and publishing these results in Medical Liability Monitor. As in previous years, the article compares historical first-quarter financial results with full-year figures to offer insight into where 2025 annual results may be headed.

The analysis is based on the collective financial performance of a large group of insurers specializing in MPL coverage. It draws on 20 years of aggregate statutory financial data compiled from S&P Global Market Intelligence. The current composite includes 168 MPL specialty companies, which reported nearly $8.4 billion in direct premium written in 2024.

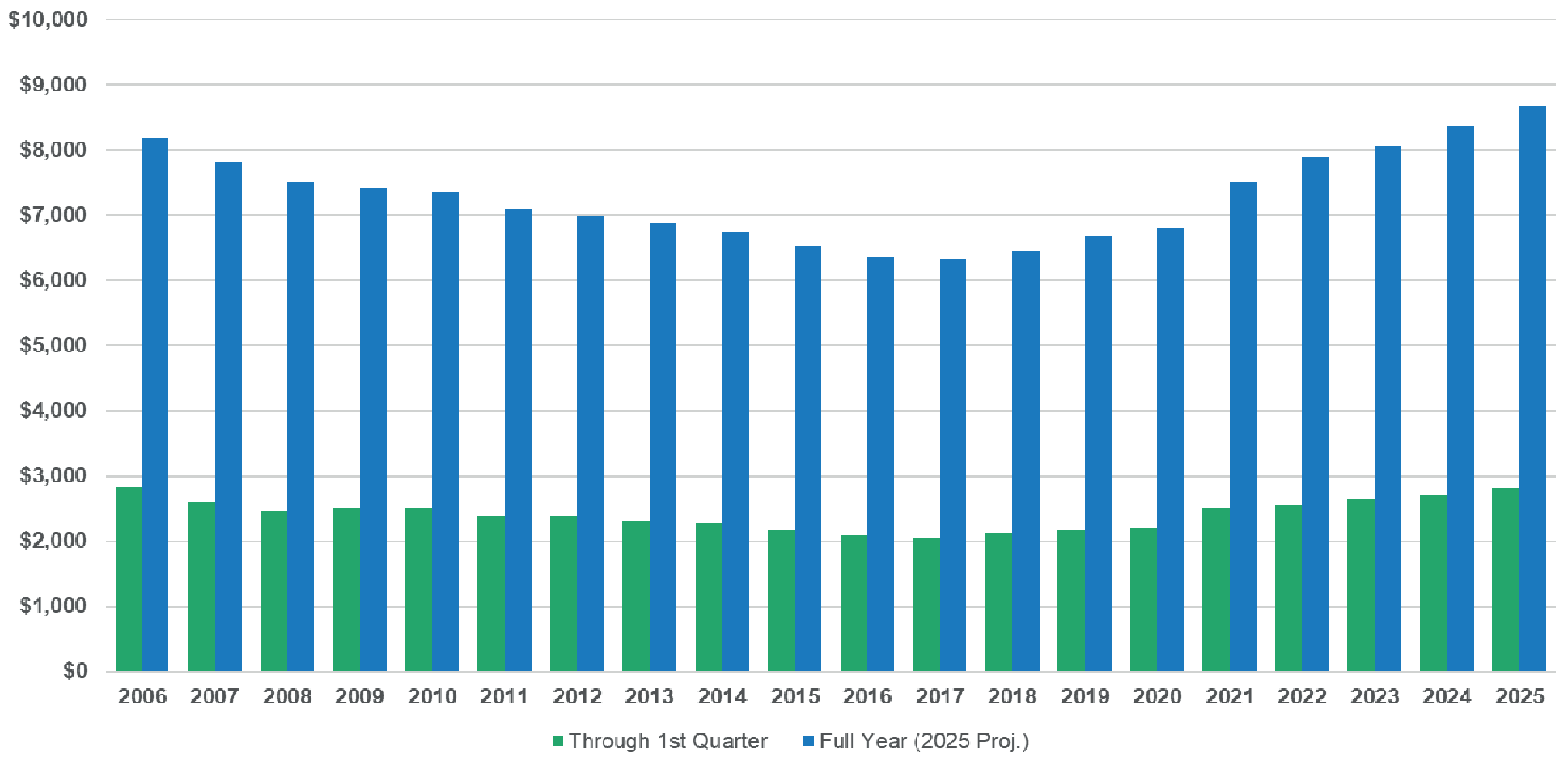

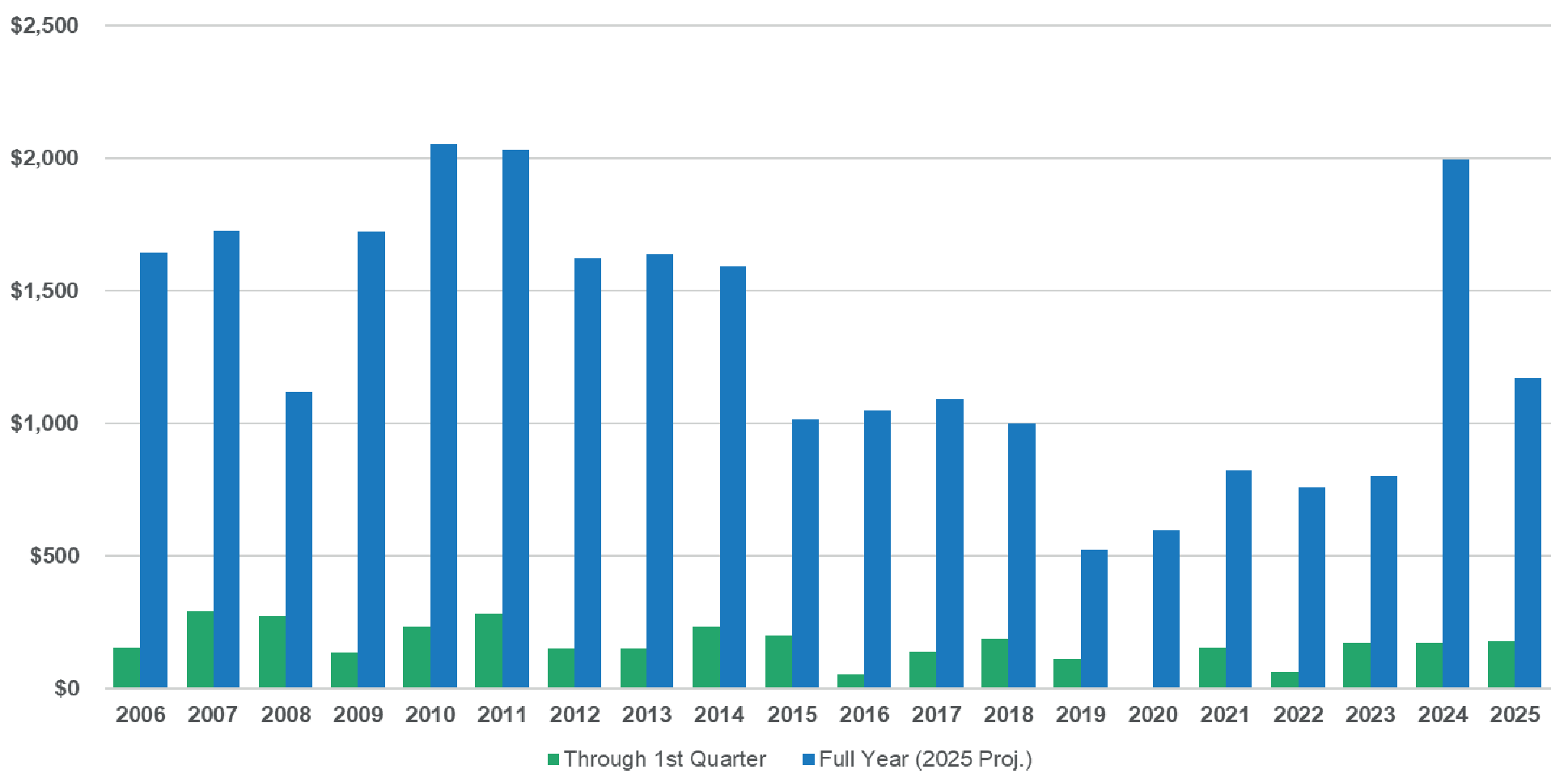

Continued premium growth

First-quarter premiums in 2025 increased compared to the first quarter of 2024, continuing an eight-year trend of first-quarter growth. The composite’s direct written premium rose by approximately 4% from the same period in 2024 (Figure 1, above), reflecting a slightly higher growth rate than seen in recent years.

A closer look shows that nearly 95% of the composite’s premium comes from MPL coverage, with the remainder primarily from general liability. Notably, after several years in which non-MPL premium growth outpaced MPL premium growth in the first quarter, MPL premium has led the way in each of the last three years.

Figure 1: Direct written premium — Q1 vs full year ($millions)

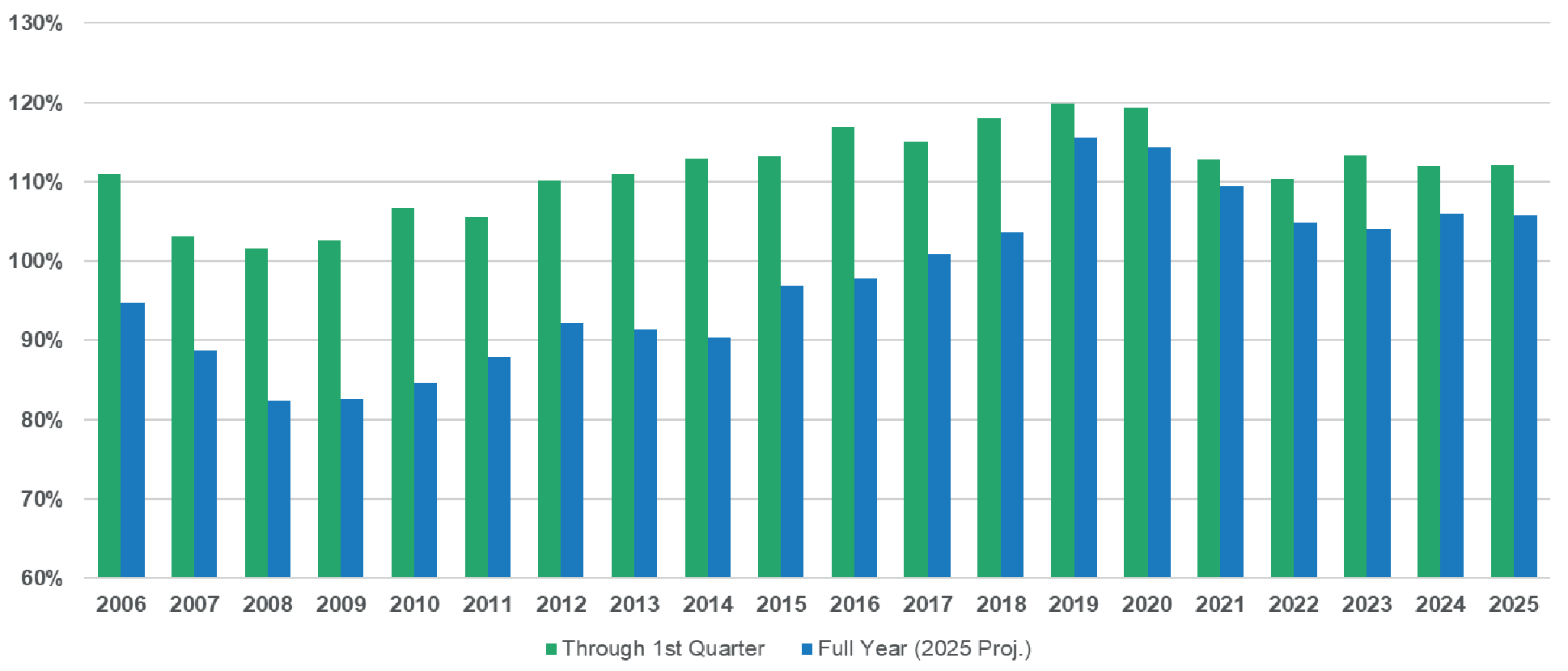

Rising combined ratios highlight underwriting concerns

The composite’s combined ratio for the first quarter of 2025 was nearly identical to that of the first quarter of 2024, holding at 112% (Figure 2, below). Increases in both the loss and LAE ratio and the fixed-expense ratio were offset by a decrease in the policyholder dividend ratio.

Figure 2 also shows the projected full-year 2025 combined ratio (blue bar), which is expected to decline compared to the first-quarter result (green bar) due to anticipated favorable reserve development throughout the year. Most reserve adjustments are typically made during the fourth quarter.

A combined ratio of approximately 105% has remained relatively stable over the past three years. While this continues to reflect challenges in underwriting performance for the MPL market, strong investment returns have helped the composite remain profitable.

Figure 2: Combined ratio (after PH dividends) — Q1 vs full year

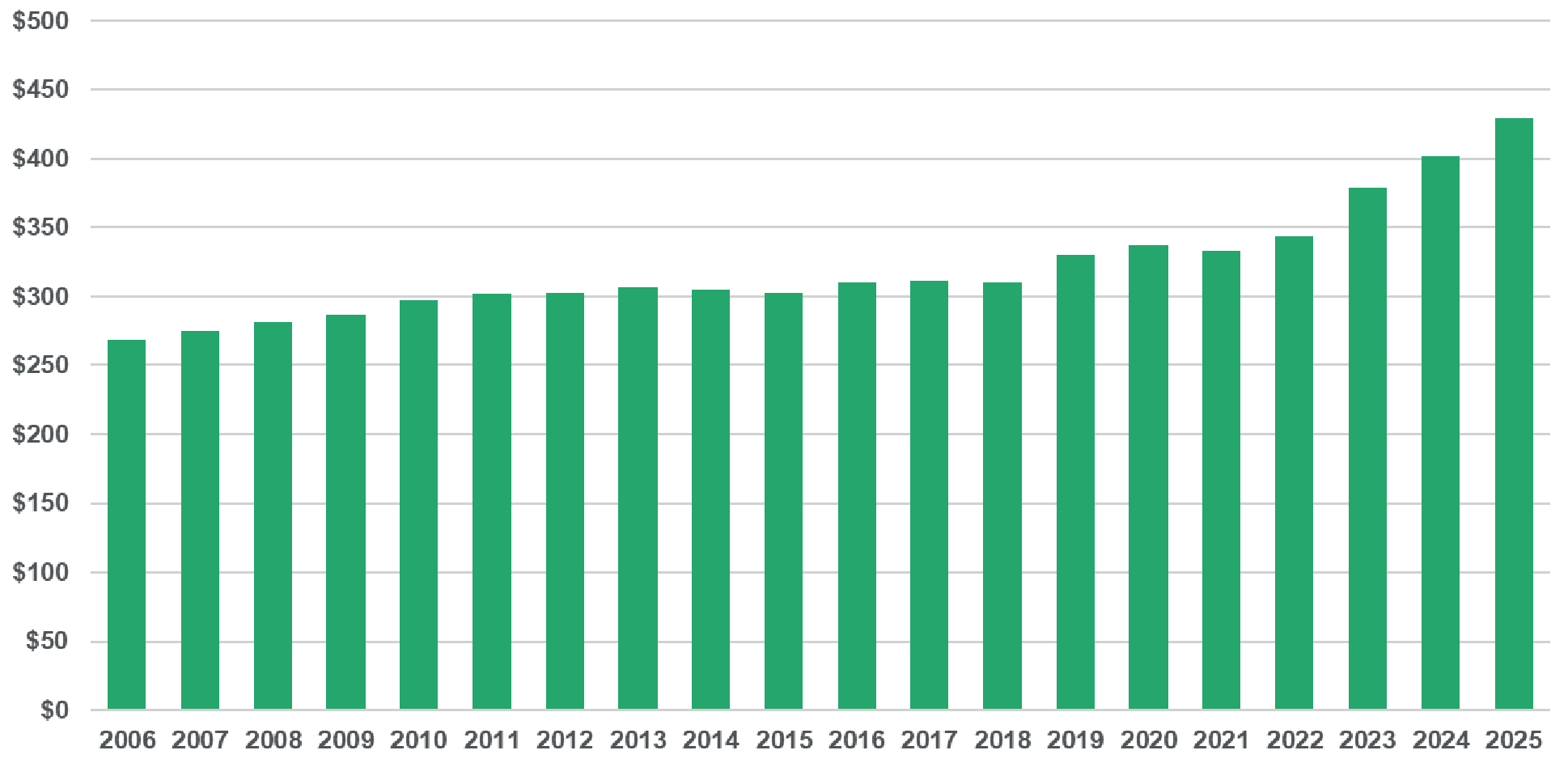

Underwriting expenses hit peak level

Underwriting expenses for the composite rose significantly in the first quarter of 2025, increasing by approximately 7% compared to the same period in 2024 (Figure 3, see page 7). While some growth in underwriting expenses is expected due to inflationary pressures, recent years have shown increases well above historical norms.

The percentage increases seen from 2023 through 2025 represent the highest rates of growth in the past 20 years, although general inflation began to ease about two years ago. Comparing recent inflation trends with the composite’s underwriting expenses suggests a one-year lag between broader inflationary cost increases and their impact on underwriting expenses. If inflation remains low in 2025, we may see underwriting expense growth begin to taper off in 2026.

This article previously highlighted the premium growth seen in recent years, which can help offset rising expenses. However, the underwriting expense ratio relative to net earned premium has increased by 1.8% since 2022, indicating that premium growth has not kept pace with the rise in underwriting expenses.

Figure 3: Underwriting expenses ($millions) through Q1

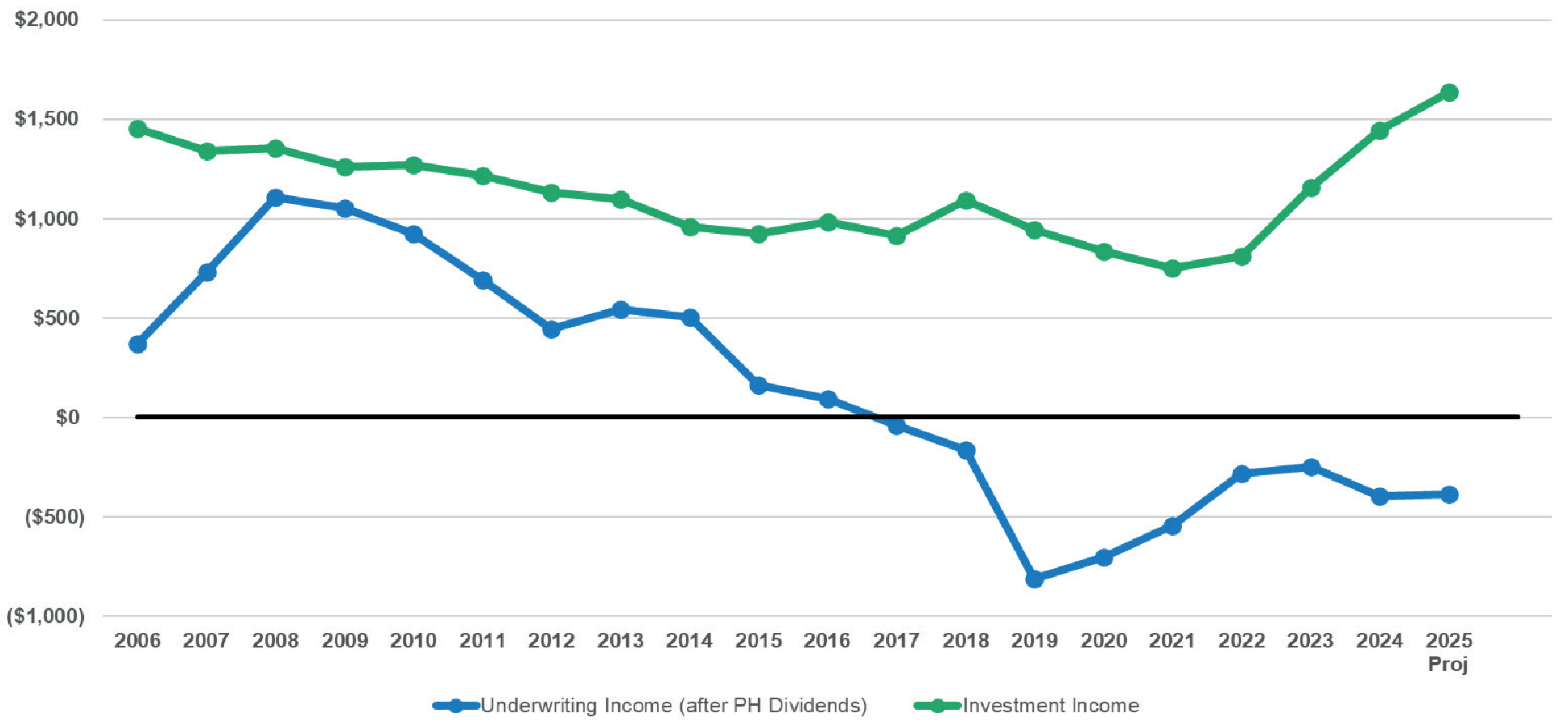

Investment income offset underwriting challenges

Figure 4 (see page 7) shows the composite’s under-writing performance (in dollar terms) alongside its investment performance over time. As discussed earlier in this article, MPL insurers continue to face underwriting challenges, reflected in the long-term decline of the blue line in Figure 4 — though that trend has stabilized somewhat in recent years. An underwriting loss is expected in 2025, continuing the pattern of negative results that has persisted since 2017.

In contrast, the composite’s investment income has continued to rise, more than offsetting underwriting losses. Investment income in the first quarter of 2025 exceeded the amount reported during the same period in 2024. If similar returns are achieved throughout the rest of the year — particularly given a growing pool of investable assets — total investment income for 2025 may surpass that of 2024. During the past 20 years, the peak in investment income occurred in 2006. With a strong start to the year, there is potential for investment income to reach a new high in 2025.

Figure 4: Underwriting income vs investment income ($millions)

Net

Last year marked the highest net income in more than a decade. The positive trend continued into the first quarter of 2025, with net income roughly equal to the same period in both 2023 and 2024. More than one-third of 2024’s annual net income came from realized capital gains by a single company within the composite. Even without that gain, net income for 2024 would have shown improvement over recent years.

Looking ahead, full-year net income for 2025 is projected to be lower than in 2024 but still significantly higher than the levels recorded from 2019 to 2023.

Figure 5: After-tax net income — Q1 vs. full year ($millions)

Conclusion

The first quarter of 2025 reflects the continuation of key trends for MPL specialty writers: sustained premium growth and strong investment returns alongside ongoing underwriting challenges and rising expense ratios. Although net income remains positive due to investment performance, it has moderated compared to the strong results of 2024.

These results underscore persistent concerns about underwriting profitability and indicate that the composite’s financial performance in 2025 will continue to depend heavily on investment gains. As the year progresses, closely monitoring these dynamics will be essential to evaluating the outlook for MPL insurers.

The previous edition of this series can be read here, and the next quarter's edition can be read here.

Eric Wunder is a principal and consulting actuary, and Leah Windt is a consulting actuary, at Milliman Inc., an independent actuarial and consulting firm.

This article first appeared in the July 2025 issue of Medical Liability Monitor: http://www.medicalliabilitymonitor.com/.