The 2018 annual report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance (OASDI) trust funds was released in June 2018. While this 270-page document contains a lot of information, there are two key items that will be of interest to group disability insurers. First, the disability trust fund is expected to be depleted in 2032, which is four years later than was reported in last year’s report. This is primarily due to the second key item, the assumption of lower disability applications and other underlying assumption changes since the prior report.

The depletion date for the disability trust fund is now estimated to be 2032 instead of 2028, which was reported in the summer of 2017. This represents the first year that the trust fund would not be able to pay 100% of the expected benefits. The key date that legislators will be looking at, though, is 2034, when both the disability income and the old-age and survivors trust funds are depleted.

According to projections, assuming no legislative changes, only 83% of disability income benefits would be payable after the trust fund is depleted. The projection also shows that the trust fund balance begins to fall in 2019. That means that starting next year, the total cost of the disability income program exceeds the total income on the program, including interest.

Steve Goss, the chief actuary of the Social Security Administration (SSA), urges that an administrative change should be implemented before 2034 for both trust funds. This change would need to increase scheduled revenues by 29%, reduce scheduled benefits by 23%, or be some combination of these changes. While neither would be politically desirable, cutting benefits could have substantial impacts to group insurers that would likely need to increase claim reserves for future benefit payments on their policies. (Lower Social Security disability insurance [SSDI] benefits would mean lower benefit offsets and thus higher long-term disability [LTD] benefit payments.)

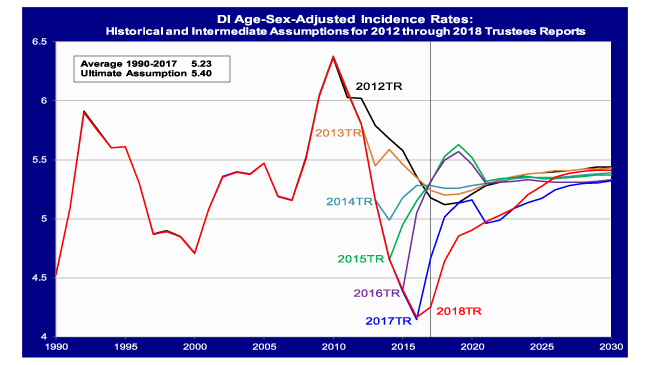

One of the underlying assumptions in the projection of the disability trust fund is the disability incidence rate. Social Security disability incidence rates tend to move with the economy. Increases in the unemployment rate generally lead to increases in new disability claims as workers who fear they will lose their jobs find ways to file for disability. The last increase in Social Security disability incidence was in 2010, just after the peak of the last U.S. recession. Unemployment rates and disability incidence rates have both been falling since that point. The Office of the Chief Actuary feels that this trend is not sustainable and is projecting an increase in disability incidence rates over the next 10 years to an ultimate rate of 5.4 new awards per thousand eligible workers. Recent industry studies of group disability insurance experience do not include incidence rates, so it is unclear whether this trend is also affecting the group insurance carriers to the same extent. If the incidence rate trends are different between SSDI and private group disability insurance programs, it could result in inaccurate reserving and pricing assumptions for Social Security offsets.

The graph in Figure 1 is taken from a presentation made by Steve Goss at the Penn Wharton Budget Model’s first Spring Policy Forum on June 22, 2018. It illustrates the continuing lower trends in disability incidence rates and the recognition of the potential for another increase following the next recession.

Figure 1: Disability incidence rate falls to historic low

SSDI disabled worker incidence rate rose sharply in the recession and has declined since the peak in 2010 to extraordinarily low levels for 2016 and 2017

The actuarial assumption report also mentions that a small portion of the decline in incidence rates is due to the backlog in the approval process. The SSA is assuming that the backlog will be eliminated by 2022. If this is true, it could also have implications for group insurers because Social Security disability payments represent offsets to their benefits. They should note that the lag for approvals of benefits is expected to shorten over the next four years and reserve assumptions should be monitored closely.

Finally, while recovery from Social Security disability has historically been very low, the most recent years are showing an increase in recovery rates. The report attributes this to an ongoing effort to reduce the backlog of continuing disability reviews. It is expected to decrease back to historical levels as they work through the backlog. The projected ultimate recovery rate is 10.3 per thousand beneficiaries. This compares to about 169 per thousand beneficiaries for private long-term disability policies, which cover many more temporary and partial disabilities.

Death rates are being projected at about 450% of the general population mortality. The Office of the Chief Actuary of the SSA is projecting population mortality to continue to decrease over time, resulting in a slightly decreasing curve for total terminations.

It is important that actuaries working with group disability insurance pay attention to changes in the SSDI program. Many changes could affect their results and may require careful planning.