Milliman analysis: 2020 funded status craters by $73 billion in January due to discount rates’ steep decline

Milliman 100 PFI funded ratio plummets to 85.7%

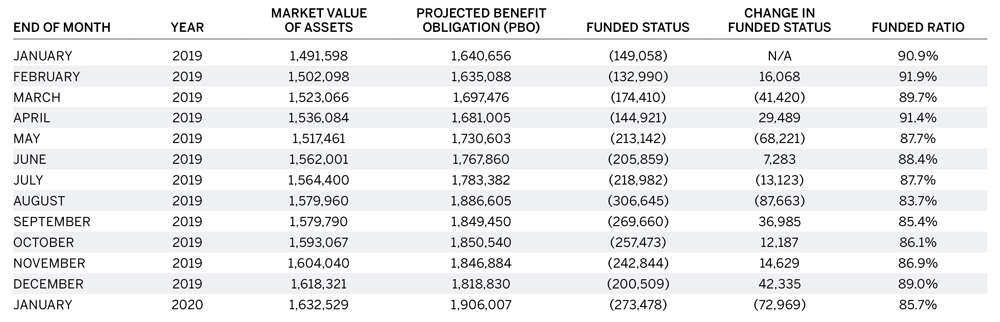

As we enter the 20th year of reporting the Milliman 100 Pension Funding Index (PFI), the funded status of the 100 largest corporate defined benefit pension plans fell by $73 billion during January. The funded status deficit swelled to $273 billion due to a decrease in the benchmark corporate bond interest rates used to value pension liabilities. The funded status decline was partially offset by strong investment gains during January, continuing the financial market rally seen at the end of the fourth quarter of 2019. As of January 31, 2020, the funded ratio fell to 85.7%, down from 89.0% at the end of December.

The market value of assets grew by $14 billion as a result of January’s robust investment gain. The Milliman 100 PFI asset value increased to $1.633 trillion at the end of January. By comparison, the 2019 Milliman Pension Funding Study (PFS) reported that the monthly median expected investment return during 2018 was 0.53% (6.6% annualized). The expected rate of return for 2019 will be updated in the 2020 Milliman Pension Funding Study, due out in April.

Highlights

| $ BILLION | ||||

| MV | PBO | FUNDED STATUS | FUNDED PERCENTAGE | |

|---|---|---|---|---|

| DECEMBER | 1,618 | 1,819 | (201) | 89.0% |

| JANUARY | 1,633 | 1,906 | (273) | 85.7% |

| MONTHLY CHANGE | +14 | +87 | (73) | -3.3% |

| YTD CHANGE | +14 | +87 | (73) | -3.3% |

Note: Numbers may not add up precisely due to rounding

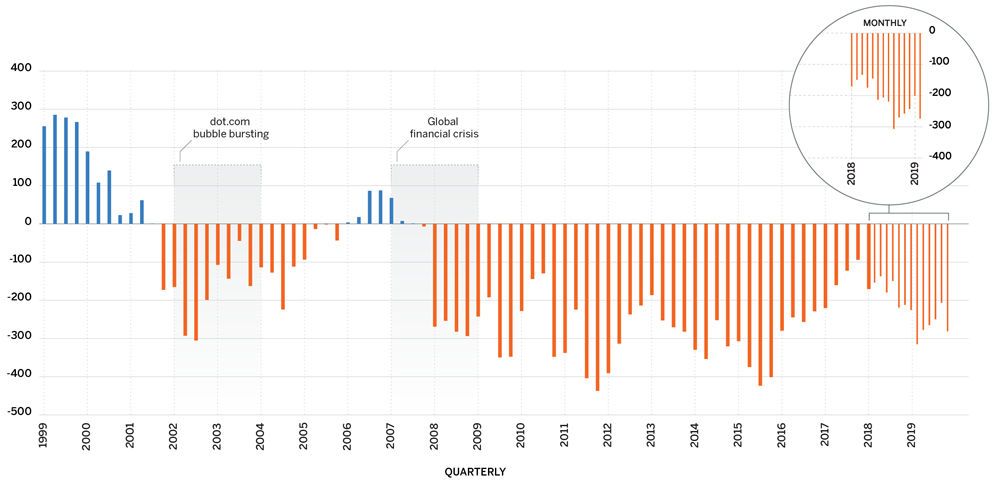

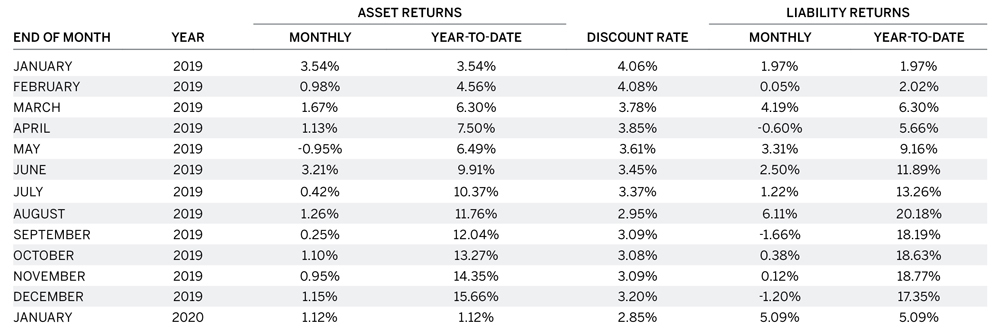

The projected benefit obligation (PBO), or pension liabilities, increased to $1.906 trillion at the end of January. The change resulted from a decrease of 35 basis points in the monthly discount rate to 2.85% for January from 3.20% for December 2019. January’s discount rate is the lowest recorded in the 20-year history of the Milliman 100 PFI. The only other time the PFI has reported a discount rate below 3.00% was in August 2019 when the discount rate stood at 2.95% and the corresponding funded status deficit was $307 billion.

FIGURE 1: MILLIMAN 100 PENSION FUNDING INDEX PENSION SURPLUS/DEFICIT

FIGURE 2: MILLIMAN 100 PENSION FUNDING INDEX — PENSION FUNDED RATIO

Over the last 12 months (February 2019 – January 2020), the cumulative asset return for these pensions has been 13.0%, but the Milliman 100 PFI funded status deficit has worsened by $124 billion. The funded status loss is the result of the steep decline in discount rates during most of 2019 and continuing into January. Discount rates one year ago were 4.06% compared to 2.85% as of January 31, 2020, signifying a 121 basis point drop.

The projected asset and liability figures presented in this analysis will be adjusted as part of Milliman’s annual 2020 Pension Funding Study, including summarizing and reporting the most recent plan sponsor SEC financials. The 2020 PFS will also reflect reported pension settlement and annuity purchase activities that occurred during 2019. De-risking transactions generally result in reductions in pension funded status because the assets paid to the participants or assumed by the insurance companies as part of the risk transfer are larger than the corresponding liabilities that are extinguished from the balance sheets. To offset this decrease effect, many companies engaging in de-risking transactions make additional cash contributions to their pension plans to improve the plan’s funded status.

Pension plan accounting information is disclosed in the footnotes of the Milliman 100 companies’ annual reports for the 2019 fiscal year, and is expected to be available during the first quarter of 2020. We expect to publish our comprehensive recap as part of the 2020 Milliman PFS this spring.

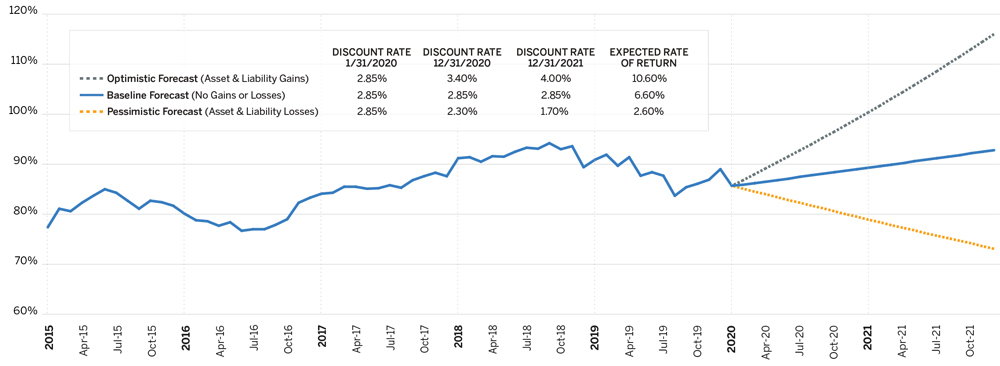

2020-2021 Projections

If the Milliman 100 PFI companies were to achieve the expected 6.6% median asset return (as per the 2019 pension funding study), and if the current discount rate of 2.85% were maintained during years 2020 through 2021, we forecast that the funded status of the surveyed plans would increase. This would result in a projected pension deficit of $209 billion (funded ratio of 89.0%) by the end of 2020 and a projected pension deficit of $135 billion (funded ratio of 92.8%) by the end of 2021. For purposes of this forecast, we have assumed 2020 and 2021 aggregate annual contributions of $50 billion.

Under an optimistic forecast with rising interest rates (reaching 3.40% by the end of 2020 and 4.00% by the end of 2021) and asset gains (10.6% annual returns), the funded ratio would climb to 99% by the end of 2020 and 116% by the end of 2021. Under a pessimistic forecast with similar interest rate and asset movements (2.30% discount rate at the end of 2020 and 1.70% by the end of 2021 and 2.6% annual returns), the funded ratio would decline to 80% by the end of 2020 and 73% by the end of 2021.

MILLIMAN 100 PENSION FUNDING INDEX — JANUARY 2020 (ALL DOLLAR AMOUNTS IN MILLIONS)

PENSION ASSET AND LIABILITY RETURNS

About the Milliman 100 Monthly Pension Funding Index

For the past 19 years, Milliman has conducted an annual study of the 100 largest defined benefit pension plans sponsored by U.S. public companies. The Milliman 100 Pension Funding Index projects the funded status for pension plans included in our study, reflecting the impact of market returns and interest rate changes on pension funded status, utilizing the actual reported asset values, liabilities, and asset allocations of the companies’ pension plans.

The results of the Milliman 100 Pension Funding Index were based on the actual pension plan accounting information disclosed in the footnotes to the companies’ annual reports for the 2018 fiscal year and for previous fiscal years. This pension plan accounting disclosure information was summarized as part of the Milliman 2019 Pension Funding Study, which was published on April 16, 2019. In addition to providing the financial information on the funded status of U.S. qualified pension plans, the footnotes may also include figures for the companies’ nonqualified and foreign plans, both of which are often unfunded or subject to different funding standards than those for U.S. qualified pension plans. They do not represent the funded status of the companies’ U.S. qualified pension plans under ERISA.