When it comes to saving for retirement, many 401(k) plan participants rely on the plan’s target-date funds as their primary vehicle of investment—an approach that has come to be known as “set it and forget it.” Such plans involve an investment portfolio that automatically grows more conservative as the targeted date of retirement approaches, allowing even participants with limited investing knowledge to simply make regular contributions and forget about the rest.

While “set it and forget it” is popular with plan participants looking for an easy solution to an often confusing and overwhelming process, it’s not necessarily the most effective in terms of growing retirement savings.

By looking beyond target-date funds, defined contribution (DC) plan sponsors will find a range of options that can accommodate the needs of participants with various degrees of financial literacy, as well as differing levels of risk tolerance. The participant allocation and advice solutions available through the Milliman platform—including Morningstar Retirement Manager, which offers both managed accounts and point-in-time advice, and Milliman’s proprietary model portfolio solution, InvestMap™—offer a more flexible, comprehensive approach to retirement investing, enabling plan sponsors to choose a more customized solution that works best for them and their participants.

How customized allocation services benefit plan sponsors and participants

In recent years, more and more plan sponsors are offering customized account allocation services, including managed accounts for 401(k) and other defined contribution plans. According to market research by Cerulli Associates, 44% of large plan sponsors offered managed accounts as of the fourth quarter of 2020, while 17% of all plan sponsors planned to offer them in the next 12 months.1

For plan sponsors, adding managed account services to their retirement plan options creates an additional layer of fiduciary protection and adds value to retirement plans. It also amplifies a competitive benefits package to better attract employees in a tight labor market.

The benefits of managed account services are even greater for plan participants, including:

- Greater confidence: In an online survey conducted by Logica Research for Schwab Retirement Plan Services, Inc. in 2021, 40% of plan participants lacked confidence when it came to making decisions on their own about their 401(k) plans.2

- Increased savings rate: Of plan participants not on track to meet retirement goals, 71% increased their savings rate after entering a managed account service.3

- Maximized employer match: Among such off-track participants, the percentage maximizing employer match increased by 12%.4

- Customized investment portfolios: Participating in a managed account service results in well-suited funds with risk levels that are better calibrated to participants’ individual needs and situations.

- Potential for more retirement wealth: With managed accounts, a typical 30-year-old participant could end up with $5,548 more annual income—a 56% increase—during retirement.5

Considering different solutions

For those looking to move beyond “set it and forget it,” the Milliman platform supports a range of flexible solutions—including managed account services and custom model portfolios—to ensure that plan sponsors can find something that works for them and their participants.

Morningstar Retirement Manager

Morningstar Retirement Manager provides plan participants with a personalized savings and investment strategy at no cost to the plan sponsor. The platform offers two levels of service:

Point-in-time advice

With this free solution, participants receive savings and investment strategy advice based on their individual needs and risk tolerance. These are point-in-time recommendations, and participants must take the initiative to update their accounts to implement different strategies over time.

Managed accounts

With the Morningstar managed account solution, Morningstar will develop a personalized, ongoing savings and investment strategy customized for the participant. This includes selecting and allocating to investments from among the plan’s offerings, performing ongoing review, adjustment and rebalancing of accounts, and issuing detailed progress reports. Participants are assessed an annual fee for the managed account, which is based on whether the account is opt-in or used as a dynamic or traditional Qualified Default Investment Alternative (QDIA) for the plan.

Both solutions factor in:

|

And provide recommendations on:

|

Custom asset allocation models: InvestMap™

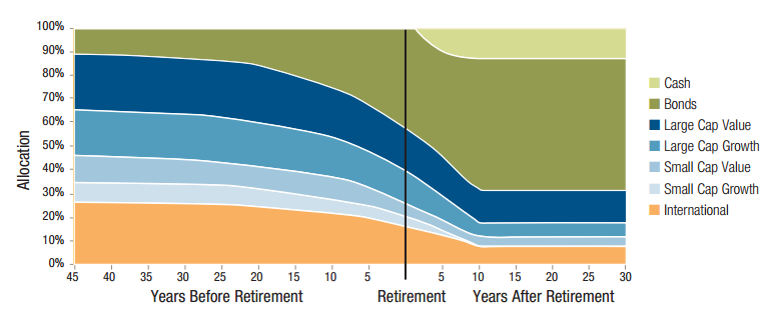

When it comes to assisting plan participants on how to invest their retirement savings, Milliman has long used a system of risk-based custom asset allocation models, ranging from conservative to aggressive. This system gives participants the flexibility to choose an investment strategy based on their own risk tolerance.

This system evolved into the Milliman proprietary solution InvestMap™, a sophisticated tool that provides an age-based, diversified asset allocation strategy for the core funds held within a defined contribution plan. Unlike the custom asset allocation models, which participants must adjust over time as their time horizons or needs change, InvestMap™ automatically readjusts to become more conservative over time. Because of this, participants can set up a lifelong investment strategy with a single click.

- Personal: InvestMap™ gives participants a moderate model as a recommendation, and they can dial the risk up or down depending on their risk tolerance.

- Simple: InvestMap™ creates a portfolio made up of existing funds in the plan.

- Automatic: Portfolios are automatically rebalanced every quarter and reallocated on the glide path every year following the participant’s birthday.

Self-directed brokerage accounts

For savvy investors who want total control over their retirement strategy and access to a plethora of options—the polar opposite of “set it and forget it”—Milliman provides plan sponsors with access to self-directed brokerage accounts through various alliance trustee relationships. This solution appeals to many defined contribution investors, especially those working in professional services, including physicians’ practices, law offices, and accounting and engineering firms.

The self-directed brokerage solution provides access to:

- Stock listed on the major U.S. exchanges, including over-the-counter stocks

- Thousands of retail and institutional mutual funds

- Bonds and other fixed income investments

- Money market funds

- Certain types of options

Milliman’s system maintains participants’ account balances, which are updated every business day, while participants receive detailed account statements directly from the brokerage (trustee).

Plan sponsors have flexibility with self-directed brokerage accounts and can choose to limit the spectrum of investments available to participants to limit responsibility and investing freedom.

Find the solution that works for you

Given the range of options available beyond target-date funds, it’s crucial for plan sponsors to consider which solution might best fit their needs and the needs of their participants. By working with your investment advisor, you can settle on a flexible, customizable solution that will both add value to your retirement plan offerings and help you to better meet fiduciary obligations by assisting participants in meeting their retirement savings goals.

Milliman InvestMap™ and Model Portfolios are services offered by Milliman Advisors, LLC. InvestMap™ may be managed by Milliman Advisors, LLC or another advisor as selected by the plan sponsor. While developed using established portfolio management techniques, there is no guarantee of success in providing future positive returns. Portfolio optimization is a systematic process that uses the historical relationships of various asset classes to construct prospective investment strategies. The optimization process does not imply that Milliman can predict future activity in financial markets, and there is no assurance of a successful investment result from using this methodology.

Morningstar® Retirement ManagerSM is offered by Morningstar, Inc. and is intended for citizens or legal residents of the United States or its territories. The investment advice delivered through Morningstar Retirement Manager is provided by Morningstar Investment Management LLC, a registered investment adviser and subsidiary of Morningstar, Inc. The Morningstar name and logo are registered marks of Morningstar, Inc.

1 Godbout, Ted (March 16, 2021). Cerulli: How Managed Accounts Are Evolving. National Association of Plan Advisors. Retrieved February 23, 2022, from https://www.napa-net.org/news-info/daily-news/cerulli-how-managed-accounts-are-evolving.

2 Charles Schwab (June 2021). 2021 401(k) Participant Study. Retrieved February 23, 2022, from https://content.schwab.com/web/retail/public/about-schwab/schwab_2021_401k_participant_survey_deck.pdf.

3 Blanchett, David, PhD, CFA, CFP® (January 22, 2019). The Impact of Managed Accounts on Participant Savings and Investment Decisions, p. 2. Morningstar Research. Retrieved February 23, 2022, from https://conferences.pionline.com/uploads/conference_admin/Morningstar_Research_Impact_of_Managed_Accounts_Paper.pdf.