Problems connected with high levels of student loan debt continue to make headlines.1 Today, the controversy centers around for-profit colleges, which, according to The Wall Street Journal, teach about 11% of higher education students, but whose students account for 44% of defaults on federal loans.2 After the bankruptcy of for-profit Corinthian Colleges Inc. in July 2014, six U.S Senators, led by Tom Harkin (D- Iowa) wrote a letter to the Education Department saying Corinthian’s failure “raises serious questions about the financial integrity of other similarly situated, publicly traded, for-profit colleges… We urgently need to bring all relevant federal agency expertise to bear in assessing the risk to students and taxpayers of another massive institutional failure.”3

Trends: Student Loan Debt and Delinquencies

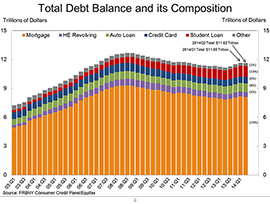

The Federal Reserve Bank of New York recently released its 2nd quarter 2014 report on household debt and credit, which allows us to compare the trends in student loan debt and delinquencies since our last article published in June 2012.10 Figure 1 shows the growth and composition of all categories of outstanding U.S. household debt. As in 2012, outstanding student debt is second only to mortgage debt in terms of total debt outstanding. Student loan debt is the only type of consumer debt that has grown since consumer debt peaked in 2008.

Source: Federal Reserve Bank of New York Consumer Credit Panel / Equifax.

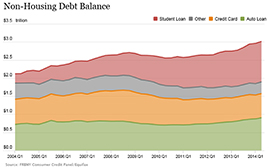

Additionally, since the 1st quarter of 2012, student loan debt has grown from $0.90 to $1.12 trillion as shown in Figure 2, an increase of nearly 25% in nine quarters. While auto debt has grown at a similar rate, mortgage debt, credit card, and other consumer debt have remained stagnant over the same time period.

Source: Federal Reserve Bank of New York Consumer Credit Panel / Equifax.

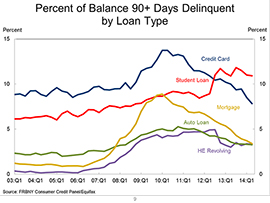

Figure 3 shows how the seriously delinquent rate for student loans has been trending and how this compares with other types of loans. Approximately 10.9% of aggregate student loan debt is either 90+ days delinquent or in default as of 2014Q2. Even though the recent trend since 2013Q3 has been positive, student loan delinquencies remain elevated relative to all other kinds of consumer debt and have actually increased from 2012Q1, whereas delinquent loans for all other debt has declined, and in some cases has done so significantly.

Source: Federal Reserve Bank of New York Consumer Credit Panel / Equifax.

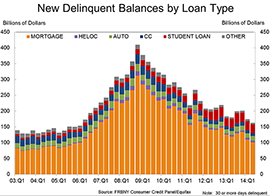

Figure 4 shows that new student loans entering delinquency have remained consistent over the last nine quarters in terms of loan balance. Contrast this to credit card and mortgage delinquencies, which have shrunk in terms of balances over the same period. This demonstrates that student loan delinquencies have not yet fully abated.

Source: Federal Reserve Bank of New York Consumer Credit Panel / Equifax.

The cumulative impact of the weighing student loan debt may be starting to be felt in other important areas of the economy. In the second quarter of 2014, only 35.9% of those under 35 were homeowners—the lowest figure over the last 21 years.11 The overall annual homeownership rate dropped to 64.7% in 2014Q2, the lowest rate since 1995 (this rate was near 69% at the peak in 2004). While there are many contributing factors for this phenomenon, student loan debt has undoubtedly had an impact. Credit has been much tighter since the Great Recession, and lenders cannot ignore student debt when calculating certain lending measures such as debt- to- income ratios when extending loans to consumers.

Students need to be keenly aware of the pros and cons of for-profits when making their school choice. Let’s take a closer look at for-profit colleges to see exactly what’s at risk for students and taxpayers.

What are for-profit colleges?

What are the legal distinctions between for-profit and non-profit colleges? Traditional colleges are set up as non-profits. This means they are tax-exempt and contributions from alumni and other interested parties are tax-deductible for the donor. Governance officially resides in the board of trustees, but powerful factions including alumni, faculty, and donor groups, as well as government (i.e., political) interests can have considerable influence.

For-profit colleges are set up as businesses and generally choose a corporate structure under which to organize. This means they pay taxes on profits and any contributions they might receive would not be tax-deductible for the donor. Also, corporations are governed by boards, which, like the boards of non-profits, must balance the interests of different stakeholders.

We learn more about what distinguishes for-profit colleges when we look at them empirically:

- Traditional non-profits include everything from private liberal arts colleges to state universities and local two-year community colleges. For-profits often resemble technical colleges that provide specialized training directed toward jobs in business, technology, nursing, education, or criminal justice.

- For-profits may offer certificate programs as well as two-year programs leading to an associate’s degree and four-year-bachelor’s degree programs.

- For-profit colleges may be small, single-location schools serving a local community. Others are chains, operating in many states across the country and, in some cases, with international locations.

- Some for-profit colleges are owned by publicly traded companies. Kaplan University is part of Graham Holdings Company and the University of Phoenix is owned by the Apollo Education Group.

- For-profits tend to rely on advertising or active recruiting to attract students much more than their traditional non-profit counterparts.

What’s controversial about for-profit colleges?

From the set of facts listed above, it’s possible to infer a worthwhile mission. As the Public Agenda report notes:

…the for-profit sector has increased access to higher education for older students with substantial family responsibilities and those who are looking to gain postsecondary credentials that are directly applicable in the workplace and can be completed in a relatively efficient manner. For-profit colleges have also been lauded for their ability to respond quickly to changing labor market demands and for using both teacher and student performance data to improve services and streamline curricula.4

But critics view the exact same set of facts and conclude:

…in too many instances for-profit schools lure students to enroll in comparatively expensive programs when these students could instead get a less expensive degree—and perhaps a better education—from a public institution.5

Combine this criticism with for-profits’ high share of defaults on federal loans, cited above as 44%, and you can understand the source of concern. With the amount of student loan debt exceeding $1 trillion, we are obviously talking about a significant amount of money. When you do the math ($1.12 trillion x a delinquency/default rate of 10.9%), the dollar amount of seriously delinquent student loans is in the neighborhood of $122 billion with a significant portion of these loans attributable to for-profit college students.

So what is causing such a high level of for-profit defaults?

Social costs

Are the students of for-profit colleges getting the right educational value for the cost?

Karen Weise, writing for Businessweek6, cites a study that purports to show that graduates of non-profits earn more than those of for-profit colleges. However, Melissa Korn reports in The Wall Street Journal7 on a different study that indicates hiring prospects are about the same for graduates of either type of institution.

The authors of the Public Agenda report support the view that outcomes are essentially equal:

Compared with public and private not-for-profit colleges, the graduation rates of for-profits are better for certificate programs, about the same for associate’s degree programs and worse for bachelor’s degree programs. And most recent research suggests that labor market outcomes for graduates of for-profit colleges are comparable to those for graduates of not-for-profit institutions once demographic differences and other selection factors are taken into account.8

While the job prospects may be on equal footing, the fact remains that for-profit college graduates often end up with more debt with almost 90% of 2012 for-profit graduates having loans averaging a total of about $40,000, according to the Institute for College Access & Success.9 One could argue that these students are simply paying a premium for the flexibility of a program with little to no entrance requirements that allows them to earn a degree at convenient times and locations—at their own pace.

That said, carrying heavy debt load into an entry-level job makes it harder to pursue other social goods such as starting a family or saving for a down payment on a home. Worse, a student attending a college that falls into bankruptcy, like Corinthian, could be stuck with the debt—without the opportunity of completing the course of study and earning a degree.

Moving Forward

For-profit colleges have attracted students through innovative scheduling and leading the way in creating online educational opportunities. Traditional non-profits can certainly learn a few things from these kinds of schools.

However, it remains clear that tough scrutiny of the value delivered to students is warranted. Some for-profit colleges need to address the cost of the education they’re providing. Tuition and fees need to be commensurate with the salary for the types of jobs students can realistically expect to secure. To put it in simpler terms, students shouldn't be paying $100,000 for a professional certificate to get a job where the average salary of that position will make it difficult, if not impossible, to repay the debt. At the same time, students need to shop around to find a program that suits their needs and fits their budget.

While for-profit schools can continue to be a successful vehicle for higher education, the execution of delivering that education to the student needs to be in the best interest of the student. The recent legal proceedings surrounding these types of schools should sound a horn of caution for future students. Like with all important choices in life, students need to weigh carefully the pros and cons when selecting a school. With more careful consideration given to school choice, the natural market balance for both availability and cost of for-profits should be achieved, allowing for students to be financially prepared to pay off their debts upon graduation.

1 http://us.milliman.com/insight/insurance/The-student-loan-debt-crisis-in-perspective/

2 http://online.wsj.com/articles/for-profit-college-rules-not-as-tough-as-proposed-1414641663?KEYWORDS=for-profit+colleges

3 http://online.wsj.com/articles/senate-democrats-question-for-profit-college-oversight-1407272184?KEYWORDS=for-profit+colleges

6“For-Profit college Alums Make Less Money.” 1/28/14

7 http://blogs.wsj.com/atwork/2014/08/18/for-profit-college-degrees-dont-help-or-hurt-hiring-prospects/?KEYWORDS=for-profit+colleges

9 http://www.usnews.com/education/best-colleges/paying-for-college/articles/2014/10/01/3-facts-for-students-to-know-about-for-profit-colleges-and-student-debt

10Figures 1 through 4 are from the Federal Reserve Bank of New York, Quarterly Report on Household Debt and Credit, August 2014, http://www.newyorkfed.org/householdcredit/2014-q2/data/pdf/HHDC_2014Q2.pdf. Our June 2012 article used the Federal Reserve Bank of New York’s 2012 Q1 Quarterly Report.

11Census Bureau. Figure 5 from: http://cnsnews.com/news/article/terence-p-jeffrey/homeownership-rate-americans-under-35-peaked-2004