The challenge

Our client is a large institutional pension fund in Italy. Participants have defined contribution accounts and are able to invest these in either a medium-risk “balanced” subfund or low-risk “guaranteed” subfund.

The guaranteed subfund currently accounts for around half of the pension fund’s total assets and is distinguished from the balanced subfund in that it offers a capital guarantee, i.e., minimum interest rate guarantee of 0% per annum. Some pension funds in Italy (such as our client’s fund) are legally obliged to offer a guaranteed subfund of this form.

An investment mandate for the guaranteed subfund is granted to an external asset manager, and the mandate effectively lays down that the overriding goal must be to respect the guarantee. Given that the asset manager backs the guarantee and costs are very competitive, typically the only logical option for the asset manager is to invest almost exclusively in short-term instruments.

At the same time, many participants see the guaranteed subfund as the safe option, and so tend to direct their contributions there. However, given the very short-term investment strategy followed by the asset manager, these contributions end up being invested in a way that does not best meet members’ long-term retirement objectives.

Growing awareness of asset-liability management (ALM) techniques in Italy led the client to contact Milliman’s Milan office to develop an ALM projection model for these two subfunds. The client’s main aims were twofold:

- To better understand the fit between asset allocation and expected future liabilities given the constraint of having to respect the capital guarantee of the guaranteed subfund

- To better inform participants regarding the likely evolution of their account balances, and in particular, provide fund-specific projections that can help guide members in their choice of future contribution levels

The solution

We began by constructing a detailed model of the pension fund using Milliman’s MG-ALFA® actuarial projection system. The model projects the expected future asset and liability cashflows implied by the current asset portfolio and participant data.

An appropriate set of assumptions on expected future experience was constructed for input to the model, both for deterministic and stochastic projections (the latter for which a complete set of economic scenarios was built and calibrated reflecting the investment strategy of the pension fund).

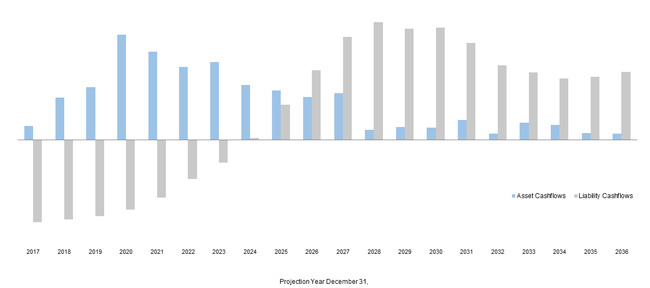

The following figure shows the resulting deterministic projection and demonstrates the clear mismatch between expected future asset (blue) and liability (grey) cashflows.

Figure 1: Asset v. liability cashflows: Deterministic projection

For the client, this was the first time that they had been able to see the likely future evolution of asset and liability cashflows, and in particular, to appreciate so vividly the much shorter nature of the asset cashflows compared to those of the liabilities.

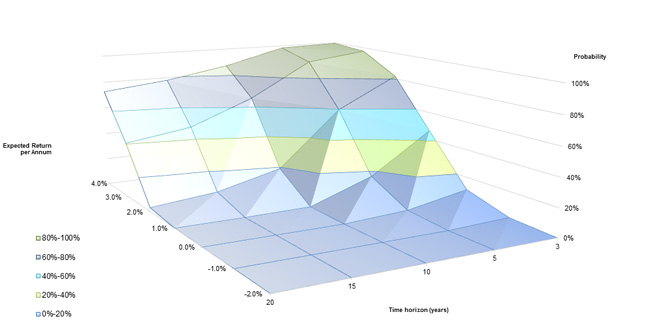

Stochastic runs of the model opened up further insight for the client. For example, we were able to test the likelihood that, based on the current asset allocation, future returns on the subfund may fall below the capital guarantee.

The following figure graphs how the stochastic results show some low probability of not achieving the capital guarantee at lower durations, but how this then becomes very unlikely over longer terms. There may, therefore, be some scope to take on more asset risk to improve returns:

The client also had the objective of improving the applicability and content of regular communications to participants, and in particular, wanted to aid members in deciding on the levels of contributions to make.

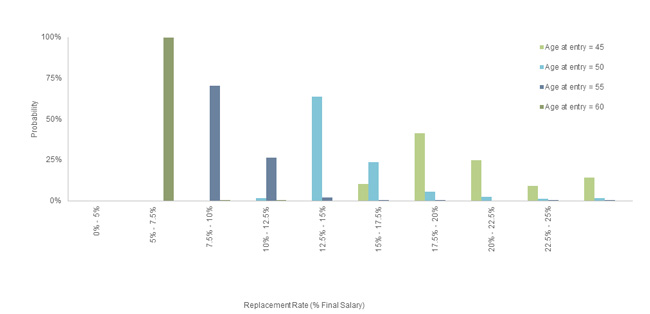

We, therefore, adapted our model to project the expected future replacement rates at retirement for a set of typical member profiles and to test distinct levels of future contributions into each of the subfunds.

Stochastic projections were again used, and the figure below indicates the resulting distributions for typical participant profiles, distinguished by age at entry:

As expected, lower replacement rates are indicated for higher ages at entry as well as less variation in the expected replacement rates. For lower ages at entry, the expected replacement rates are higher, but the range of possible replacement rates at retirement is wider.

Given that these results are calculated based on stochastic projections of actual subfund data, this information is directly applicable to the participants and is proving to be a valuable addition to the client’s communication strategy.

The outcome

The project has clearly demonstrated the benefits to our client of stochastic ALM analysis and tools such as Milliman’s MG-ALFA.

Working closely with Milliman on these analyses can lead directly to more effective investment management and asset allocation, and in turn achieving both better matching between assets and liabilities as well as reducing the risk of insolvency and achieving higher expected investment returns.

The results have also led to a recognition on the part of the client that the pension fund was effectively “flying blind”. This has been a key insight for the client given that they, like many pension funds in Italy, did not realise that this was the case because ALM techniques are not yet widespread in the sector.

Our client now requires us to report to them on a regular basis, and Milliman’s stochastic projection analyses directly inform their investment strategy, asset allocation and participant communications. The Milliman Milan office is also fielding enquiries regarding other large Italian pension funds that are now looking to set up similar ALM reporting frameworks.