Background on CRT

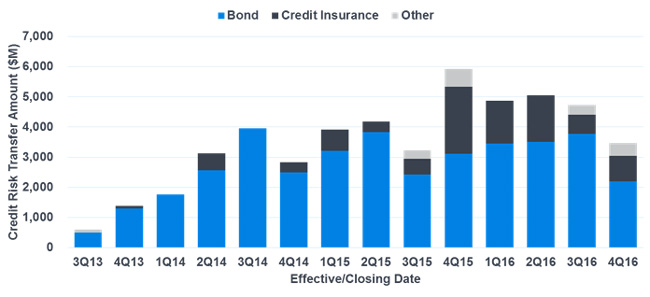

Since 2013, the government-sponsored enterprises Fannie Mae and Freddie Mac, referred to as the GSEs hereafter, have created many credit risk transfer (CRT) transactions to reduce taxpayer exposure to the mortgage credit risk assumed through their operations by transferring that credit risk to third-party investors. As of December 31, 2016, the GSEs covered a portion of the credit risk related to reference pools of mortgages totaling over $1.24 trillion at issuance.1 The GSEs have been investigating new ways to structure their CRT transactions and continue to reveal new structures as the CRT market grows, with their largest portion of credit risk transferred through their bond/debt offering transactions: Freddie Mac’s Structured Agency Credit Risk (STACR) and Fannie Mae’s Connecticut Avenue Securities (CAS). The GSEs have also transferred substantial credit risk through the Freddie Mac Agency Credit Insurance Structure (ACIS) and the Fannie Mae Credit Insurance Risk Transfer (CIRT) credit insurance transactions, pool mortgage insurance transactions (e.g., the Fannie Mae MIRT), and whole loan securities (WLS) transactions (e.g., the Freddie Mac WLS). The chart in Figure 1 shows a breakdown of the CRT transactions from the third quarter of 2013 through the fourth quarter of 2016.

Figure 1: History of GSE credit risk transfer transactions

MBS and the role of GSEs

The GSEs facilitate mortgage originations by purchasing single-family mortgages from financial institutions across the country, which frees up capital, allowing the lenders to originate additional mortgages. The GSEs aggregate mortgages and sell securities based on the associated cash flows of the mortgages, in securities known as mortgage-backed securities (MBS) to third-party investors.2 Investing through MBS allows investors to receive a portion of the principal and interest that the GSE receives from the borrowers of the underlying mortgages, essentially owning a piece of a tranche. The GSEs guarantee the timely payment of principal and interest on those MBS by charging a guarantee fee3 to the lender, which is passed on to the borrower through the interest rate charged to the mortgage. Through this structure, the GSEs retain all credit risk and thereby expose taxpayers to the risk of a government bailout in the case of significant defaults on the underlying collateral.

CRT bonds explained

CRT bonds, or credit risk transfer bonds, are different from typical GSE MBS in that most of the credit risk is transferred to investors. In CRT bonds, the tranches of loans from the reference pool are similarly tied to the mortgage collateral, but as loans default, the securities incur principal write-downs. The principal write-downs are allocated to the tranches within a deal according to the cash flow structure of securities.

The GSE debt offerings follow a waterfall cash flow structure: the senior tranches are paid in full before the subordinate tranches. Conversely, credit losses that occur on the underlying mortgages are applied in reverse sequential order, starting with the most subordinate tranches. Each tranche has an attachment and detachment point in which payments and losses are applied. They can be thought of as layers in a reinsurance agreement, where a layer is only activated once the loss breaches a certain percentage of total unpaid principal balance (UPB).

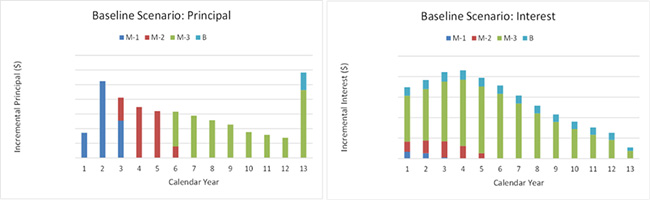

CRT bonds are issued at par and have historically been one-month LIBOR floating rate securities plus a credit spread. The chart in Figure 2 shows a simulated structure of payments for a representative CRT deal for multiple bonds (or tranches), with M-1 being the most senior and B being the most subordinate.

Figure 2: Simulated structure of payments

Risk profile of CRT

Interest rate risk and credit risk are the two most significant sources of risk in CRT bonds. The two main items to consider while evaluating the credit risk of mortgage collateral in CRT bonds are the credit quality of the underlying mortgages and the economic environment over the life of the mortgages. Some examples of variables used to estimate the credit quality of mortgages include the borrower’s credit score, loan-to-value (LTV) ratios,4 occupancy type, or prior delinquencies. The economic environment contributes the most to the probability of defaults on the underlying mortgages. Therefore, many forecasts and analyses are done by investors using a range of economic scenarios to try to predict the losses and coupons of their investments. Some economic indicators for mortgage performance used in these analyses include the regional house price index, home price appreciation, unemployment rates, and movement in interest rates. As a reference, there have been significantly larger credit events when home prices fall compared with when home prices rise.

Figure 3 provides an indication of cash flows for a middle layer tranche under various collateral loss scenarios. The collateral loss scenarios are dependent on the economic conditions where poor economic conditions result in write-downs. In this example, the Stress Scenario could be compared to economic conditions similar to, or more severe than, the 2007 economic crisis. The lower collateral loss scenarios would correspond to periods of economic expansion, particularly with respect to the housing market.

A useful metric used by investors to help analyze interest rate risk is a bond’s Macaulay duration (or simply “duration”). In short, a bond’s duration is the average number of years weighted by the portion of the present value of each cash flow with respect to the bond’s price. A shorter duration, measured in years since purchase, means the investor gets back the initial investment sooner. From the table in Figure 3, we see that the duration for this security could range from three years to 11 years, depending on the economic scenario. Therefore, the performance of the bonds, including principal and interest received, is sensitive to economic conditions. An investor should carefully evaluate the performance of the bonds under a wide range of economic scenarios to understand how the cash flows change under alternative economic conditions.

Comparison with corporate bonds

Institutional investors are large investors in the corporate bond space. CRT bonds could offer diversification to corporate bonds. The table in Figure 4 compares corporate bonds with CRT bonds:

Figure 4: Corporate bonds and CRT bonds

| Corporate bonds | Credit risk transfer bonds (based on transactions completed to date) | |

| Exposure | Individual corporate entity | Diversified pool of mortgages |

| Coupon | Fixed or floating rate coupon | Floating plus credit spread |

| Principal | Typically full repayment at expiration of the bond | Paid throughout the life of the asset consistent with the principal repayment of the underlying collateral |

| Expected credit loss | With a large portfolio, an investor would expect some level of defaults in most economic scenarios | Credit losses depend on the performance of the underlying mortgages; most investment grade CRT securities are expected to need a catastrophic economic scenario, similar to the 2007 crisis, to experience a credit loss |

Spreading the underlying exposures for CRT bonds across many geographic areas allows for a diversification of exposures (i.e., thousands of individual borrowers) as compared with corporate bonds, which is a single entity. In addition, for a portfolio of 1,000 corporate bonds, an investor might expect 50 to default, for a default rate of 5%. With CRT bonds, you may have an expected default rate of 5% weighted across all economic scenarios, but in most of the scenarios you would experience a 0% default rate.

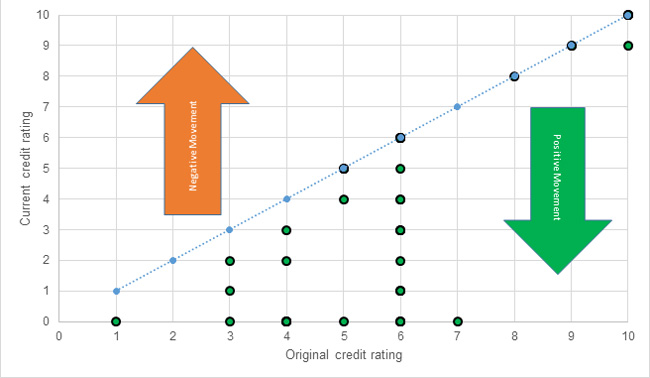

In terms of performance, as of February 2017, most of CRT bonds have shown positive movement in their credit ratings since issuance with none showing an unfavorable movement.

The table in Figure 6 provides a comparison of the average initial spread with corporate option-adjusted spread (OAS) over the last five years as of May 31, 2017. We can see that, historically, CRT bonds tend to have higher comparable spreads than corporate bonds. As the market for CRT bonds continues to grow and interest rates continue to rise in the short term, we can expect similar trends in spread.

Figure 6: Average initial spread versus corporate OAS

| Initial credit rating | Average initial spread to 1 million LIBOR | Corporate OAS as of May 31, 20175 |

| AA | 1.49 | 0.73 |

| AA- | N/A | 0.84* |

| A | 1.78 | 0.95 |

| A- | 1.78 | 1.07* |

| BBB | 1.78 | 1.48 |

| BBB- | 2.58 | 1.86* |

| BB+ | 3.89 | 2.08* |

| BB | 3.83 | 2.31 |

| B+ | 4.68 | 2.99* |

| B | 5.69 | 3.66 |

| NR | 4.91 | N/A |

| * Interpolated values. | ||

Conclusion

In the Federal Housing Finance Agency (FHFA) 2017 Conservatorship Scorecard, FHFA laid out its goals for 2017. There have not been any significant changes since 2016, which leads us to believe the GSEs have been performing well and are expected to continue to thrive in 2017 with these CRT deals. The CRT market is most likely to stay constant or increase in the future, depending on any legislative changes for the GSEs. Overall, as the market for CRT transactions continues to grow and diversify, investors should continue to look to them as valuable parts of their portfolios and consider them as one way to participate in the mortgage market.

Milliman M-PIRe is a valuation and securitization software that efficiently evaluates and manages exposure to the mortgage market including mortgage performance models, a complete cash flow library for bonds and reinsurance credit risk transfer securities, whole loan portfolio modeling, and benchmarking. To learn more about M-PIRe visit www.milliman.com/en/products/milliman-m-pire.

1 2016 Annual Reports on Form 10K for Fannie Mae and Freddie Mac.

2 MBS are bonds that are secured by a collection of mortgages.

3 The guarantee fee covers the projected credit losses for the underlying loans, any administrative costs, and the cost for holding the capital required to protect against any catastrophic economic scenarios.

4 LTV ratio: principal amount of the loan compared with the current value of the house. Lower LTV ratios tend to reflect less risky exposures.

5 CRT Ratings and Spreads: Bloomberg; Bond Spreads: BofA Merrill Lynch US Corporate Option-Adjusted Spread Index.