Earlier this summer, for the first time since the full implementation of the Patient Protection and Affordable Care Act (ACA) in 2014, the commercial individual and small group marketplaces received a point of comparison for the performance of the risk adjustment program.1 Risk adjustment has been a recurring part of the health insurance news cycle ever since the Centers for Medicare and Medicaid Services (CMS) released the initial 2014 results in June 2015.2,3,4 The dialogue has ranged widely from apprehension about perceived biases in the risk transfer calculation to reports suggesting the program is, for the most part, attaining its fundamental objectives. Regardless of narrative, the initial 2015 risk adjustment report shows that the magnitude of the transfer payments continues to significantly impact the financial results of many issuers.

At the aggregate level, why might total 2015 transfer payments have remained just as material as last year’s? To start, health plans did not know their 2014 transfer payments until halfway through 2015. Accordingly, any commitments made by a carrier to improve its 2015 risk adjustment position in response to the 2014 results immediately encountered a contracted timeline before the final data submission cutoff. Given the long lead times often needed for strategy design and execution, any amount of lost time in 2015 would have been a detriment to an initiative’s success. Compounding that, carriers were already locked into 2015 plan and benefit offerings, service areas, network options, exchange participation status, formulary designs, and other strategic decisions directly affecting risk transfers. Second, CMS made only minor updates to the 2015 risk adjustment program, which ensured relative risk score stability by condition. Finally, the variation in enrollee risk profile between different carriers does not appear to have increased or decreased considerably, as the 2015 aggregate absolute transfer payments as a percentage of premium decreased only a small amount in either market.

At present, we cannot specifically assess the risk adjustment program’s influence on the financial performance of any one carrier’s ACA business. We can, though, evaluate 2015 results at the state and national levels and make comparisons with 2014. In doing so, several patterns emerged from the data, most notably:

- Total risk adjustment transfer payments at the national level remained at about 10% of premium in the individual market and 6% of premium in the small group market.

- Roughly one in four issuers offering plans in a given state or market in both 2014 and 2015 switched between payer and receiver status.

- Statewide risk scores rose more year-over-year than the movements in market demographics and average plan benefit richness would have suggested.

- Where available, the interim risk adjustment report did not provide a reliable indication of the ultimate value of the 2015 risk score.

In the remainder of this paper, we explore each of these conclusions in greater depth.

Overview of 2015 transfer payments

Market insights

The 2015 CMS risk transfer payment summary report offers useful, although limited, insights into how risk adjustment affected the ACA market and provides a comparison point with the final 2014 transfer results. While additional detail will not be available until later this year, the following themes are initially apparent:

- Both the individual and small group ACA markets grew significantly in 2015, which is consistent with previously published exchange reporting.

- The average 2015 premium per member per month (PMPM) increased for both markets over the average 2014 premium PMPM.

- Total transfer payments as a percentage of premium remained a large proportion of overall market premium.

We summarize these themes by market and plan year in the table in Figure 1.

Figure 1: 2015 Risk Adjustment Results Overview

| Individual Market | |||

| 2014 | 2015 | % Change | |

| Billable Member Months | 100,438,806 | 163,260,469 | 62.5% |

| Average Premium PMPM | $352.05 | $362.99 | 3.1% |

| Implied Market Premium | $35,359 M | $59,261 M | 67.6% |

| Transfer Payments (total) | $3,506 M | $5,615 M | 60.2% |

| Transfer Payments (% premium) | 9.9% | 9.5% | -4.4% |

| Small Group Market | |||

| 2014 | 2015 | % Change | |

| Billable Member Months | 43,803,609 | 85,676,442 | 95.6% |

| Average Premium PMPM | $441.48 | $446.68 | 1.2% |

| Implied Market Premium | $19,338 M | $38,270 M | 97.9% |

| Transfer Payments (total) | $1,131 M | $2,159 M | 90.9% |

| Transfer Payments (% premium) | 5.9% | 5.6% | -3.6% |

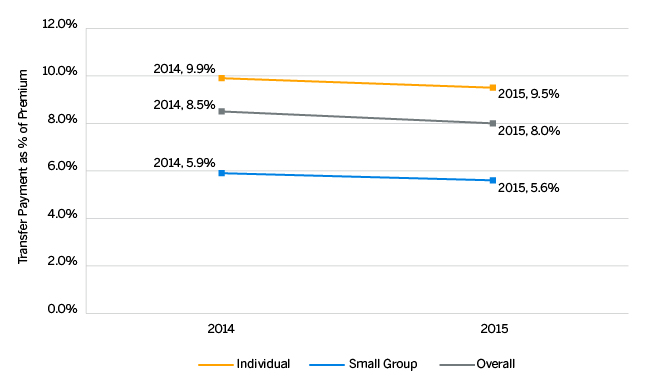

Total transfer payments, on average, continue to be a large portion of market premium but do compress slightly

As outlined in the CMS report5 and supported in Figure 1, the individual market continued to experience transfer payments of approximately 10% of market-wide premium while the small group market remained near 6%. These numbers changed only somewhat, despite the member month growth experienced in each market. To better frame the movement in risk transfer payments, we graph the aggregate 2014 and 2015 results in the chart in Figure 2.

Figure 2: Total Absolute Transfers as a Percentage of Market-Wide Premium

Across the program, transfer payments decreased a small amount as a percentage of premium in the individual and small group markets in 2015. This limited change seems to have been a reasonable expectation, in hindsight, because carriers could only work in a narrow window to implement strategic initiatives to improve 2015 risk scores after the release of the 2014 risk adjustment results. Some measure of compression is also realistic when considering natural improvements in EDGE data management and medical coding over time. Less clear, though, is the risk profile of the 2015 new market entrants. However, the relative uniformity of transfer payments as a percentage of premium year-over-year, while potentially resulting from any number of situations, likely suggests the risk profile distribution of 2015 new entrants among carriers in the market was reasonably consistent with 2014.

There is a risk, however, in placing too much stock in the levels or movements of transfer payments in just the first year or two of such a complex program. It is rather easy to list the various reasons why the results may or may not maintain a level of consistency over time (exchange enrollment issues, transitional plan extensions and eventual merger with the ACA market, growth of new entrants and the impact of carriers exiting, the EDGE learning curve, traction in medical coding improvement initiatives, etc.). As the ACA marketplace matures—settling down from population, carrier participation, and regulatory standpoints—it will be interesting to track the progression of risk adjustment results over a longer period of time.

2015 risk adjustment results: A little more in-depth

Thus far, we have presented a general summary illustrating the movement of 2015 enrollment, premium, and transfer payments, and have performed some basic comparisons with the 2014 plan year. In the next few sections, we focus on more targeted implications of the 2015 results.

One in four carriers switched transfer position from a payer to a receiver or vice versa

In the table in Figure 3, we display the distribution of issuers in 2014 and 2015 by risk transfer position.

Figure 3: Percentage of Issuers by Transfer Position

| Receipt to Payment | Same Position | Payment to Receipt | |

| Individual | 14.1% | 76.2% | 9.7% |

| Small Group | 13.0% | 73.0% | 14.0% |

| Total | 13.5% | 74.3% | 13.2% |

Figure 3 illustrates the consistency of transfer position in 2015 relative to 2014. In general, carriers that collected, collected again; those who paid in, paid in again. This result is reasonable, given consumer and carrier dynamics. Enrollment can be sticky—consumers are more willing to stay with a plan with which they are satisfied and can afford. And because a stable enrollment base is a valuable asset both financially and in setting rates, carriers often employ strategies to retain the existing membership and then supplement the block with new sales. Add to this the stabilizing impacts of the auto-enrollment process and a plan’s level of coding intensity (for better or for worse) carrying forward one year to the next, then the patterns in Figure 3 seem generally reasonable. At the same time, a measure of change in transfer positions is to be expected, as some carriers will inevitably experience shifting risk profiles, particularly with the market growth in 2015. Also, certain segments of members may have shopped for new plans,6 whether to lower their premium or to keep pace with changing premium subsidies, for those receiving financial assistance in the individual market.7

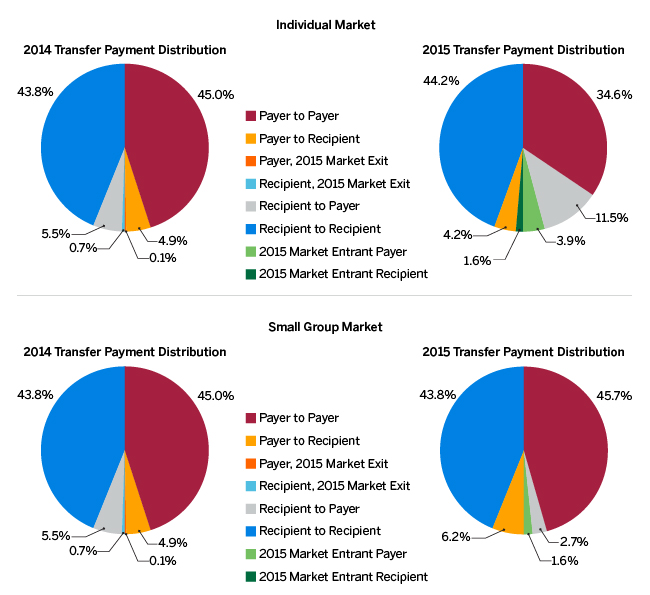

In 2015, though, a slightly higher proportion of issuers flipped from a receipt to a payment than vice versa. We present the distribution of absolute transfer payments in 2014 and 2015 by transfer position and issuer participation status in the charts in Figure 4. Each chart represents all transfer dollars in a given market and benefit year. Within each chart, the right half represents transfer payments from issuers in the benefit year, and the left half represents transfer payments to issuers in the benefit year.

Figure 4: 2014 and 2015 Absolute Payments by Position and Issuer Participation Status

In both the individual and small group market, over 85% of transfer payments in 2014 were experienced by carriers maintaining the same transfer position in both 2014 and 2015 (the sum of the blue and red slices). The majority of the remaining transfer amounts represents carriers whose transfer position flipped in 2015 (the yellow and gray slices). Carriers exiting any given state or market prior to the start of 2015 contributed less than 1% of 2014 transfers.

The 2015 transfer payments had slightly more variability. Carriers experiencing a risk adjustment receipt in both years had about the same total percentage of transfer payments in 2015 as in 2014 (comparing the blue slices). Further, in the individual market, carriers owing payments into the program in both 2014 and 2015 (the red slices) collectively contributed a smaller portion of total transfer payments in the second year of the program (45% of transfer payments versus 34.6% of transfer payments). This perhaps reflects an improvement in risk coding or EDGE data management in 2015 or a shifting risk profile that mitigated some of the transfer payments owed.

Another item of note in the individual market relates to issuers that received a transfer in 2014 but owed a transfer in 2015 (the gray slice). Those carriers contributed a receipt of 5.5% of total transfer payments in 2014 but collectively contributed an 11.5% payment in 2015. This large shift filled the void noted above in total transfers left by the shrinking payments in 2015 from those paying into the program both years (the red slices). It also means these health plans may have experienced much larger impacts to their financials, as the transfers not only shifted from a collection to a payment, but the total 2015 payments were more than double the previous year’s collections as a percentage of market premium.

In both individual and small group, new market entrants in 2015 paid more into the program than they received. This would suggest that new entrants continue to face headwinds from the risk adjustment program,8 although without more detailed data we cannot adequately determine either how strong these headwinds may be nor how the program impacted these carriers’ financials.

Risk scores increased between 2014 and 2015 significantly more than expected

The risk score is a paid claims estimator and varies based on the recorded diagnoses, ages, genders, and benefit levels of the risk pool’s members. In theory, then, it is positively correlated with the combined movements of the benefit richness and member demographics (i.e., age and gender).9 In the table in Figure 5, we compare the change in risk score with the combined change in the market average benefit richness and average age (represented by the demographic factor), which we define as the risk-rating ratio.

Figure 5: Risk Adjustment Report Parameter Comparison, Federal Age Curve States10

| Individual | Small Group | |||||

| 2014 Final | 2015 Initial | Change11 | 2014 Final | 2015 Initial | Change | |

| Risk Score | 1.5409 | 1.6028 | 2.7% | 1.2450 | 1.3457 | 9.7% |

| Benefit Richness Factor | 0.7011 | 0.6946 | -1.1% | 0.7682 | 0.7634 | -0.6% |

| Demographic Factor | 1.6040 | 1.5806 | -1.7% | 1.4137 | 1.4028 | -0.5% |

| Risk-Rating Ratio | 1.3702 | 1.4599 | 5.5% | 1.1464 | 1.2566 | 11.0% |

We define the risk-rating ratio as:

This metric measures market average risk after accounting for items carriers can address in premium rate development.

If the relative morbidity and diagnosis coding intensity in the markets had remained steady, then we would have expected the risk score to decrease commensurately with the decrease in the combined change in the benefit richness and demographic mix. Yet Figure 5 paints a different picture—risk scores actually increased. In fact, the risk-rating ratio increased by over 5% in the individual market and by 11% in the small group market.

The inconsistent movement in risk score relative to the other factors likely has several drivers. For example, the health status of enrollees could have materially changed. However, CMS has already reported that early 2015 results were indicative of a healthier population,12 which would tend to reduce risk scores. If CMS’s assertion is accurate and average morbidity levels decreased in 2015, then the market experienced some combination of the following:

- Carriers substantially improved diagnosis coding in 2015.

- The data shortfalls in the 2014 EDGE submission process were significant but were remedied in 2015.

- The effects of 2014 partial-year ACA enrollment, particularly in the small group market, were material.

While the first two are within a measure of control by a carrier, the financial effects would depend on the extent to which that carrier was influenced by the combination of all three items relative to the market as a whole.

Interim results published by CMS were an incomplete picture

In advance of the initial 2015 risk adjustment report, CMS provided a limited set of interim results by state in March 2016 as an aid for carriers submitting 2017 rates. Because of the strict data quality criteria, CMS only released interim results for 21 states. For various reasons, including inconsistent data submissions and differences in how aggressive carriers corrected medical record coding gaps throughout the year (as opposed to nearer the close of the plan year), it was unclear how useful the interim report would ultimately prove to be. CMS even cautioned that the “final risk adjustment data may differ significantly from the data” in the report, both “in magnitude and possibly direction of the transfers.”13 The table in Figure 6 compares various risk adjustment model parameters between the interim and initial 2015 reports.

Figure 6: Performance of Interim 2015 Risk Adjustment Report

| Individual | Small Group | |||||

| Interim | Initial | Change | Interim | Initial | Change | |

| Member Months | 45,810,394 | 46,177,561 | 0.8% | 32,220,814 | 32,909,258 | 2.2% |

| Statewide Average Premium PMPM | $368.14 | $367.67 | -0.2% | $488.74 | $487.50 | -0.3% |

| Risk Score | 1.5254 | 1.6393 | 7.7% | 1.4300 | 1.5048 | 5.2% |

| Benefit Richness Factor | 0.6969 | 0.6973 | 0.0% | 0.7643 | 0.7647 | 0.0% |

| Demographic Factor | 1.5096 | 1.5065 | -0.1% | 1.2590 | 1.2571 | 0.0% |

| Risk-Rating Ratio14 | 1.4174 | 1.5161 | 7.2% | 1.1911 | 1.2545 | 5.4% |

State average premium, member months, and the state average allowable rating factor and actuarial value remained generally consistent. The exception in both markets is the risk score, which increased materially as carriers worked to complete medical diagnosis coding and correct data issues in the EDGE environment. Those projecting the risk score from the CMS interim report had the difficult task of estimating the value of market-wide coding efforts and EDGE cleanup at the end of the year, all while accounting for the possibility of different claim paid-through dates by issuer. Looking at the 21 states where interim data was available, the change in risk score between the two reports ranged from 1.7% to 16.0%.15

By comparing the interim report with the initial report in aggregate and making some assumptions, we can develop a high-level estimate of the impact of runout on risk scores. While carriers were only required to submit EDGE information through the third quarter, the small differential in member months suggests that most included a full plan year of data. Further, it seems reasonable to assume most carriers could not have provided an entire month of runout in January and still hit the February 2, 2016, EDGE submission deadline for the interim 2015 report. This implies a little less than four months of pure risk score completion and any year-end EDGE data cleanup was worth more than 7.5% in the individual market and 5% in the small group market—much more than our internal research would have suggested. Caution should be used when relying on Figure 6 for an estimate of 2016 completion, as any one year of data for fewer than half of the states may not be indicative of future years or regions.

Conclusions

The ACA risk adjustment program is here for the long term, and commercial carriers just received a first look into the movement of their own results and of some marketplace metrics with the recent release of the initial 2015 risk adjustment report. At an aggregate level, we see evidence of a program that continues to be an impactful piece of many health plan financials. And underneath these aggregate results, each state, market, and carrier has its own story—one potentially very different from the market trends. At this time, any clear movements in transfer payment volatility on a PMPM or percentage of premium basis at the carrier level remain hidden from view but likely exhibit a range of variation as wide as the variation in the transfer payments themselves.

As the 2016 benefit year progresses, carriers will focus on maximizing the claim-risk score relationship through better medical coding, improvements in EDGE server data oversight, and targeted medical management. Beyond 2016, many will shift focus to the performance of subsegments of their ACA blocks following risk adjustment and will develop strategies around this lone “R” over the long term. The continued evolution of the program, the materiality of transfers on a health plan’s bottom line, and strong competitive pressures throughout the market will help solidify risk adjustment’s importance in all aspects of an ACA carrier’s pricing and planning.

Looking ahead

Most risk adjustment discussions seem to revolve around two main points: the transfer dollar amount and the degree of risk mitigation (i.e., how well the program actually works). While there certainly are benefits to estimating transfer amounts and analyzing potential correlations among the various subsegments, those participating in the ACA market tend to focus more on understanding how well (or not) the program actually mitigates issuer risk.

Given limitations in the current information available, we focus on the early results of 2015 ACA risk adjustment through a broader lens. A deeper analysis of true risk adjustment volatility and the realized levels of risk mitigation, although currently outside the scope of this discussion, will not be beyond reach later this year when additional carrier-specific financial data is made public. Such a detailed study will likely yield some extremely interesting results and could quite possibly lend some insights into the greater implications of the risk adjustment program.

Methodology, sources, and assumptions

In developing this analysis, we summarize several publicly available sources, where possible, to the state or market level. Most of these data sources do not separate the individual market into the component catastrophic and metallic tier risk pools. Thus, when necessary, we combine relevant risk adjustment parameters across the metallic tier and catastrophic pools to create an individual market total by weight-averaging on reported member months for the respective pools.

Although the Vermont ACA market is merged, we categorize this state in the individual market, given the existence of cost-sharing reduction (CSR) subsidies for low-income members, the treatment of the CSR population in the risk score calculation, and the overall size of the state’s individual market.

Throughout the paper, we reference the following CMS reports and publications:

-

Report: Summary Report on Transitional Reinsurance Payments and Permanent Risk Adjustment Transfers for the 2014 Benefit Year

Publication date: September 17, 2015

Information obtained: 2014 risk adjustment payments, along with statewide premiums, risk scores, and other statewide parameters necessary to the risk adjustment transfer payment calculation -

Report: Summary Report on Transitional Reinsurance Payments and Permanent Risk Adjustment Transfers for the 2015 Benefit Year

Publication date: June 30, 2016

Information obtained: 2015 risk adjustment payments, along with statewide premiums, risk scores, and other statewide parameters necessary to the risk adjustment transfer payment calculation -

Report: Interim Summary Report on Risk Adjustment for the 2015 Benefit Year

Publication date: March 18, 2016

Information obtained: Interim 2015 risk adjustment results from the available 21 states for comparison with the initial 2015 summary report

Limitations

Readers should consider the limitations outlined below when using the analyses we present in this paper.

All results are based upon publicly available data. We rely on this data as reported, although we do perform high-level evaluations for reasonability. If any information is revised at a future date, the results of our analysis may, likewise, change.

Our results could be affected at any time by the shifting legislative environment. Since full implementation of the ACA, aspects of the risk adjustment program alone have been modified several times. Should any salient feature of the ACA change, our conclusions may no longer apply.

Finally, the results presented utilize the initial 2015 CMS risk adjustment transfer report. Although not anticipated, our results could materially change if final 2015 transfer payments and statewide risk adjustment parameters deviate significantly between this initial report and the final report to be released in September 2016.

Fritz Busch, Jason Karcher, Jason Petroske, and Kaitlin Fink are members of the American Academy of Actuaries and are qualified to perform the analysis contained in this paper. The authors would like to thank Scott Jones, Doug Norris, Hans Leida, and Scott Weltz for their insights and review of this paper.

1Centers for Medicare and Medicaid Services (June 2016). June 30, 2016, Summary Report on Transitional Reinsurance Payments and Permanent Risk Adjustment Transfers for the 2015 Benefit Year. Retrieved June 30, 2016, from https://www.cms.gov/CCIIO/Programs-and-Initiatives/Premium-Stabilization-Programs/Downloads/June-30-2016-RA-and-RI-Summary-Report-5CR-063016.pdf

2Centers for Medicare and Medicaid Services (March 24, 2016). March 31, 2016, HHS-Operated Risk Adjustment Methodology Meeting: Discussion Paper. Retrieved July 21, 2016, from https://www.cms.gov/CCIIO/Resources/Forms-Reports-and-Other-Resources/Downloads/RA-March-31-White-Paper-032416.pdf.

3American Academy of Actuaries (April 2016). Insights on the ACA Risk Adjustment Program. Retrieved July 21, 2016, from http://actuary.org/files/imce/Insights_on_the_ACA_Risk_Adjustment_Program.pdf.

4Consumers for Health Options, Insurance Coverage in Exchanges in States (November 4, 2015). Technical Issues with Risk Adjustment and Risk Corridor Programs. Letter to U.S. Department of Health and Human Services Secretary Sylvia Burwell. Retrieved July 21, 2016, from http://nashco.org/wp-content/uploads/2015/11/CHOICES-White-Paper-on-Risk-Adjustment-Issues.pdf.

5CMS, Summary Report, ibid., p. 3.

6ASPE Report (October 28, 2015) Consumer Decisions Regarding Health Plan Choices, In the 2014 and 2015 Marketplaces. Retrieved July 23, 2016, from https://aspe.hhs.gov/sites/default/files/pdf/134556/Consumer_decisions_10282015.pdf.

7The study discussed at http://kff.org/health-reform/press-release/premiums-set-to-decline-slightly-for-benchmark-aca-marketplace-insurance-plans-in-2015/examined 16 cities across the country and found that, in 12 of those 16, at least one of the lowest-cost silver plans had changed from 2014 to 2015, meaning members who received financial assistance had some incentives to change carriers to maximize their subsidies.

8Liner, D. & Siegel, J. (July 2015) ACA Risk Adjustment: Special Considerations for New Health Plans. Retrieved July 23, 2016, from http://www.milliman.com/insight/2015/ACA-risk-adjustment-Special-considerations-for-new-health-plans/. The authors point out several factors may present risk adjustment challenges to new market entrants.

9The value of the risk score generally increases as age and benefit richness increase. With significant changes in age, we would expect the risk score to move more than the demographic factor because of the compression in the age curve used in rating. This is especially true in states with their own age curves and in community-rated states.

10We exclude community-rated states (New York and Vermont) and states with their own age curves (D.C., Utah, Minnesota, and, in the small group market only, New Jersey) because of their impact on the demographic factor. However, these states exhibited the same general patterns related to risk score and the risk-rating ratio as the federal age curve states.

11Note that these values represent the average change in these parameters, rather than the percentage difference in the values illustrated in this table.

12Centers for Medicare and Medicaid Services (July 21, 2015). Letter from Kevin J. Counihan, Director, Center for Consumer Information and Insurance Oversight (CIIO). Retrieved July 21, 2016, from https://www.cms.gov/cciio/resources/letters/downloads/doi-commissioner-letter-7-20-15.pdf.

13Centers for Medicare and Medicaid Services (March 2016). March 18, 2016, Interim Summary Report on Risk Adjustment for the 2015 Benefit Year, pp. 3-4. Retrieved June 30, 2016, from https://www.cms.gov/CCIIO/Programs-and-Initiatives/Premium-Stabilization-Programs/Downloads/InterimRAReport_BY2015_5CR_031816.pdf.

14As with our analysis in Figure 5, the risk-rating ratio here excludes the impact of community-rated states and those utilizing nonstandard age curves. Movement in the excluded states was similar to that illustrated in Figure 6.

15This range excludes the plan liability risk score (PLRS) change in the catastrophic risk pools, which varies from a decrease of 2.7% to an increase of 26.8%.