Introduction

With the passing of the Medicare Access and CHIP Reauthorization Act of 2015 (MACRA), Centers for Medicare and Medicaid Services (CMS) is making a push to move healthcare providers into alternative payment models (APM). The Department of Health and Human Services’ (HHS) goal is lofty – link 50% of Medicare payments to alternative payment models by 20181. To achieve this, a large bet has been placed on physician reimbursement incentives tied to APM participation brought on by the new Merit-Based Incentive Payments System (MIPS). With adjustments based on MIPS ranging from -9% to +27% by 2022 (a spread of 36%*), many provider organizations must give stronger consideration to CMS-sponsored alternative payment models.

One such model is the Next Generation Accountable Care Organization (NGACO). Currently, 21 organizations have the option to participate in the NGACO Model for 20162 (the first performance year). However, each of these organizations had until April 1 to withdraw from the program altogether or defer participation until 2017. The 2017 performance year may bring on new entrants who are either new applicants or deferred their application from 2016. As the 2017 NGACO application deadline quickly approaches (Letter of Intent is due by May 20, 2016) and MIPS3 incentives/penalties draw closer (the first year that MIPS will be in place is 2019), many organizations find themselves evaluating it as an option. While an array of financial and operational questions need to be asked and contemplated, we have identified five key financial considerations that all ACOs should closely review before deciding whether or not to take the plunge.

Next Generation ACO Model: A primer

The Next Generation ACO Model (NGACO Model) is an attribution-based risk sharing model similar to the Medicare Shared Savings Program (MSSP) and the Pioneer ACO program. The NGACO Model, like the MSSP and Pioneer ACO programs, is built around Medicare fee-for-service (FFS) payments, where the actual FFS payments for the ACO-aligned beneficiaries are compared to a population-specific cost benchmark. Financial savings and losses are determined based on how the actual FFS payments compare to the benchmark.

The NGACO Model is aimed at ACOs with considerable experience managing and coordinating care for Medicare patients that want to assume a higher level of financial risk/reward than the current models offer.

Outlined below are the key features of the NGACO Model:

- Alignment

- Prospective

- Voluntary alignment begins in 2017

- ACOs must maintain at least 10,000 aligned Medicare beneficiaries to stay eligible

- Rural ACOs must maintain at least 7,500 aligned Medicare beneficiaries

- Benchmark (target)

- Baseline population: Based on Calendar Year (CY) 2014 experience for NGACO’s aligned beneficiaries

- Baseline Year: CY 2014 for Performance Years (PY) 2016, 2017, and 2018

- Separate benchmarks for the aged and disabled (A+D) population and the end stage renal disease (ESRD) population

- Trend

- National trend with a regional adjustment

- The national trend benchmark is calculated prospectively (the quarter before the start of the performance period) based on CMS’s estimate of United States Per Capita FFS Costs (USPCC). This is the same trend benchmark used to determine the Medicare Advantage payment rates.

- Risk adjustment

- Hierarchical Condition Categories (HCC)-based risk score by enrollment type

- Risk scores are normalized relative to the national reference population (all alignment eligible beneficiaries)

- Baseline to performance year risk score changes are capped at +/-3%

- Discount

- 0.5% to 4.5% benchmark reduction

- Reduction is based on ACO quality score and regional and national efficiency estimates

- Agreement period

- 2016 entrants: Performance years CY2016, CY2017, and CY2018

- 2017 entrants: Performance years CY2017 and CY2018

- Potential for up to two one-year extensions regardless of entry year

- Risk sharing

- 80% or 100% savings/losses

- No risk corridors

- Maximum savings or loss of 15% of the target

- Savings are subject to sequestration (2% reduction)

While the higher degree of shared savings being offered by the NGACO Model may be appealing to many potential participants, there are a number of characteristics of the model that make the decision to participate in the program complicated and participant-specific. Through our work researching the components of the NGACO Model, we have identified five major financial considerations that we feel potential participants should thoroughly understand and evaluate before committing to participate (ranked by our perceived importance with 1 being the most important, this may vary by ACO).

5. ACO’s CY2014 experience is the baseline for the first three performance years

The NGACO benchmark is based exclusively on the ACO’s CY2014 aligned beneficiary experience. This is similar to other ACO models such as the Pioneer ACO in that the ACO’s historical experience is used as the foundation of the benchmark. However, under the NGACO program, a single year (CY 2014) is used to develop the benchmark for performance years 2016, 2017, and 2018. In contrast, the Pioneer ACO benchmark is based on three years of the ACO’s experience for aligned beneficiaries.

Therefore, up to three years of NGACO shared savings or losses will be tied to a benchmark based on a single baseline year (CY 2014). ACOs should carefully review their CY 2014 experience to determine if it accurately reflects their baseline costs. Smaller ACOs should consider conducting a volatility analysis to assess the potential impact of a random fluctuation in costs. The ACO should also consider what percentage of the aligned beneficiaries from CY2014 might still be aligned in future periods. Additional analysis may be required, but the bottom line is that the ACO needs to evaluate the likelihood that it can perform better in 2016 and beyond versus 2014.

4. Risk score changes are capped at 3% from the baseline year to each performance year

In previous ACO demonstrations, the benchmark payment is adjusted using the CMS-HCC model to compare risk scores between the baseline and performance year. However, in the NGACO Model, the risk score difference between the baseline and performance year is capped at 3% (i.e., a maximum 3% increase or decrease).

The intent of CMS seems clear, which is to avoid paying more simply for better documentation (i.e., coding improvement). However, there are many plausible scenarios where one would expect changes in the population’s risk profile to fluctuate by more than 3%. This is especially true as time passes and the performance period extends further out from the baseline period (CY2014 for performance years one to three). Two potential drivers of this risk profile change are changes to the participating provider list and changes due to the alignment methodology.

1) For each performance year, the baseline year (CY2014) experience is recalculated for the ACO’s current provider list, so changes to the participating providers could change the aligned population’s risk profile.

2) As Medicare beneficiaries have freedom to seek services with providers of their choice, the alignment methodology may not provide a stable population over time. In a recently published study performed by Partners Health System, it observed significant year-to-year turnover in the ACO-aligned population for its large Pioneer ACO (approximately two-thirds of aligned members in a given year were aligned in the previous year)4.

The 3% cap on risk score changes, beneficiary turnover, and the impact of new beneficiaries could prove either financially problematic or fortuitous for an ACO. If the beneficiaries exiting the ACO are less costly than the newly aligned beneficiaries, the ACO could experience significant losses. On the other hand, if the beneficiaries exiting the ACO are more costly than the newly aligned beneficiaries, the ACO could find itself competing against a favorable benchmark. It is worth noting that risk scores are “re-normalized” each year relative to all alignment-eligible beneficiaries contributing experience to each entitlement category (A+D or ESRD). This could mitigate some of the risk of hitting the cap, although this re-normalization will magnify the risk score change adjustment if the NGACO’s risk score moves in the opposite direction of the reference population.

Because the benchmark targets are based on CY2014 experience and the cumulative risk score adjustment is capped at 3%, the impact of high beneficiary turnover could compound over time and result in a very different population profile in 2017 (or beyond) than the 2014 benchmark population. The risk of the high year-to-year member turnover may be mitigated with the introduction of the voluntary alignment beginning in 2017. Voluntary alignment allows individuals to indicate the ACO they should be aligned with instead of being aligned programmatically using the NGACO alignment algorithm. This allows NGACOs to actively pursue a more consistent member base. However, the impact of voluntary alignment may be unknown for ACOs applying to the NGACO program. Given the potential financial consequences of significant population changes, each ACO will need to actively monitor the changing dynamics of its aligned population.

3. First dollar savings and losses

In previous ACO demonstrations, CMS introduced the concept of the Minimum Savings Rate and the Minimum Loss Rate. These rates represented thresholds under which the ACO would not share in either the losses or the savings resulting from the ACO (i.e., a loss of less than the Minimum Loss Rate or a savings of less than the Minimum Savings Rate would result in no loss or savings for the ACO).

However, the NGACO Model is a first dollar shared savings and loss model where the ACO is responsible for spending above the discounted benchmark (losses) and savings below the discounted benchmark (savings). In other words, there is not a corridor in the NGACO Model where small savings and losses are ignored. Furthermore, savings are only paid in excess of the discounted benchmark, not from the original benchmark, in contrast with the Pioneer ACO program and the MSSP.

This becomes a bigger issue when an ACO considers potential loss scenarios (poor performing) relative to savings scenarios (well performing). For an ACO to achieve savings, it must first overcome the benchmark discount, similar to a Minimum Savings Rate. However, there is no Minimum Loss Rate (for example, 1.5%) to shield the ACO from losses. With the discount methodology, the ACO is penalized if it does not achieve the target savings. Therefore, an ACO with a 1.5% discount that did not achieve any savings would simply have a 1.5% loss.

We have provided the below table to illustrate the previous points. The table compares shared savings/(losses) expressed as a percentage of the benchmark (not discounted for NGACO). We used MSSP Track 3 which provides 75% shared savings and assumed a minimum risk corridor of 1.5%. For the Next Gen ACO scenario, we assumed Risk Arrangement A, which provides 80% shared savings and a benchmark discounted by 1.5%.

| Actual performance versus target* | ||||||

| Program | Risk corridor | Discount | Savings/(loss) sharing percentage | 1% higher | 1% lower | 2% lower |

| MSSP Track 3 | 1.5% | N/A | 75% | no loss | no savings | 1.5% savings |

| Next Gen: Risk Arrangement A | N/A | 1.5% | 80% | 2.0% loss | 0.4% loss | 0.4% savings |

*Actual performance versus target before the 1.5% discount. For example, if the NGACO’s target trend before discount was 3.3% and the NGACO’s experience was 1% higher than this target, then the NGACO’s trend would have been approximately 4.3%. This translates into a 2.0% loss for the NGACO because the experience would be 2.5% above the discounted benchmark (i.e., 1% higher due to experience plus the 1.5% discount), and 80% of 2.5% is 2.0%.

2. The 2016 benchmark trends are likely understated

The NGACO’s 2016 benchmark cost is trended from the CY2014 baseline using a prospective trend rate developed by CMS in the fourth quarter of 2015. We have identified two key risks pertaining to the current trend methodology:

1. The trend is fixed.

2. The trend appears to be understated.

Unlike the Pioneer ACO and MSSP programs, which use a reference population trend benchmark, the NGACO program uses a fixed benchmark trend. A benefit of the fixed prospective trend is that the ACO’s benchmark will be known before the start of the performance year. However, as with any prospective trend, there is uncertainty in the trend projection, which may create additional risk to the ACO. For example, the trend will not be adjusted to reflect a worse than expected flu season or the introduction of a new high cost treatment.

Additionally, we believe the initial prospective trend between 2014 and 2016 is understated for the following reasons:

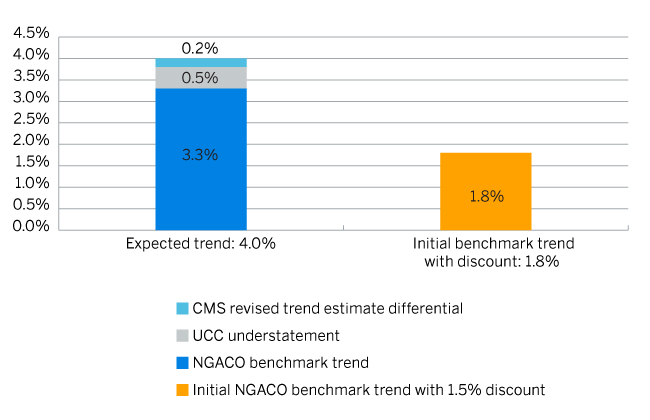

1. CMS’s initial 2014-2016 nationwide A+D trend estimate of 3.3% is 0.2% lower than CMS’s revised A+D trend estimate from the 2017 Medicare Advantage Advanced Notice5 released on February 19, 2016.

2. The NGACO Model explicitly excludes inpatient Uncompensated Care (UCC) payments from all of its calculations. However, the fixed trend rate utilized in the NGACO model for 2016 includes UCC payments. Because UCC payments have decreased by approximately 15% per year from 2014 to 2016 and because UCC payments make up about 7% of inpatient acute hospital payments or roughly 1% to 2% of total Medicare payments, the trend is understated by approximately 0.5%.

Given these understatements, we recommend that potential NGACOs check with their CMS representative to see if the benchmark trend will be updated and to review the development of the final benchmark trend for overall reasonableness. Note that the benchmark trend has an area adjustment component. Therefore, the trends and the potential understatement will vary by area.

Chart 1 below illustrates the estimated impact of the initial A+D benchmark trend understatement and shows an illustrative A+D benchmark trend for an NGACO with a 1.5% discount.

Chart 1: 2014 to 2016 expected trend versus benchmark trend for an NGACO with a 1.5% discount

1. In order to achieve savings, participants must outperform trended baseline less discount

One of the defining characteristics of the NGACO Model is the inclusion of a discount which is applied to the trended, risk-adjusted baseline expenditures to develop performance-year benchmarks.

The standard discount is 3%. Adjustments are then made (upwards or downwards) based on quality performance, regional efficiency, and national efficiency as summarized below.

| Discount adjustment | Minimum impact | Maximum impact |

| Standard discount | 3.0% | 3.0% |

| Regional efficiency adjustment | -1% | +1% |

| National efficiency adjustment | -0.5% | +0.5% |

| ACO quality adjustment | -1.0% | +0.0% |

| Total discount adjustment | -2.5% | +1.5% |

| Total discount | 0.5% | 4.5% |

It is worth noting that both the regional and national efficiency adjustments will be calculated based on the baseline year (CY2014 for performance years one to three). This means that these adjustments are static for performance years one to three and will be a known factor in calculating potential profitability. The ACO Quality Adjustment is directly correlated with the ACO quality score: an ACO quality score of 100% reduces the discount by 1% and a quality score of 50% reduces the discount by 0.5%. We expect many NGACOs will have a discount between 1.5% and 2.5% for the first performance year (CY 2016) because all NGACOs that comply with quality reporting requirements will receive the full -1.0% quality adjustment for their first performance year (this is also true for plans whose first performance year is CY 2017). In future performance years, the ACO quality score will reflect quality results from the previous performance year. Therefore, for most ACOs, the discount applied will be greater in future performance years than it will be in performance year one. Note that this discount is not cumulative and will be applied only once when calculating each performance year’s benchmark.

Conclusion

Despite the potentially large savings hurdle associated with the NGACO Model, there are significant incentives under MACRA for providers to participate in APMs. Currently, the two primary ACO options available to Medicare providers are NGACO and MSSP Track 3. Both models have their own sets of advantages and disadvantages. Therefore, the specific circumstances of a given ACO will determine whether the NGACO Model provides significant financial opportunity or significant financial risks.

Across the above five financial considerations alone, many NGACOs could have a 2% to 3% or higher savings hurdle in the first performance year. Once an NGACO overcomes this savings hurdle, it will be well positioned for continued success in future performance years due to the stability of the benchmark. However, NGACOs that find themselves in a loss position will have a significant uphill battle to achieve savings. Thus, potential NGACOs should work with an actuary to develop a realistic picture of their expected financial performance to help the NGACOs understand the risks and make strategic decisions before committing to the program. Fortunately, due to the prospective nature of the NGACO Model benchmarking methodology, an ACO can gain a basic understanding of where it stands and the range of possible financial outcomes before entering the first performance year.

*Due to the budget neutrality of MIPS adjustments, an upward or downward scaling factor may be applied to the adjustment percentages.

1 https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2015-Fact-sheets-items/2015-01-26-3.html

2 https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2016-Fact-sheets-items/2016-01-11.html

3 https://www.cms.gov/Medicare/Quality-Initiatives-Patient-Assessment-Instruments/Value-Based-Programs/MACRA-MIPS-and-APMs/MACRA-MIPS-and-APMs.html

4John Hsu, Mary Price, Jenna Spirt, Christine Vogeli, Richard Brand, Michael E. Chernew, Sreekanth K. Chaguturu, Namita Mohta, Eric Weil and Timothy Ferris. Patient Population Loss At A Large Pioneer Accountable Care Organization And Implications For Refining The Program

5 https://www.cms.gov/Medicare/Health-Plans/MedicareAdvtgSpecRateStats/Downloads/Advance2017.pdf