The Patient Protection and Affordable Care Act (ACA) includes risk mitigation programs, also known as the 3 Rs, for individual and small group health insurance markets.1 The 3 Rs include a permanent risk adjustment program, a transitional reinsurance program for the individual market, and a temporary risk corridor program. The transitional reinsurance and temporary risk corridor programs span from 2014 through 2016, while risk adjustment is a permanent program. The intent of these programs is to mitigate adverse selection and enhance market stability.2 The 3 Rs also affect financial reporting, and ACA health plan issuers faced many challenges when estimating the financial impact of the 3 Rs on 2014 financial statements. This paper summarizes 2014 3R estimates compared with actual amounts published by the Center for Consumer Information and Insurance Oversight (CCIIO).

Analysis of actual-to-estimated 3R amounts provides insight into the actual financial strength of ACA health plan issuers compared with the reported financial strength as of December 31, 2014.

Key insights

Our research suggests that ACA health plan issuers developed 2014 financial statements in a particularly uncertain environment. Key findings from our research include:

- $0 risk adjustment estimates. While half of the ACA health plan issuers included in our study accrued a $0 net risk adjustment transfer amount, no ACA health plan issuer realized a $0 net transfer amount. The proportion of ACA health plan issuers that accrued a $0 transfer amount, which potentially represents an inability to estimate as opposed to an actual estimate of $0, illustrates the degree of uncertainty inherent in developing risk adjustment estimates in 2014 financial statements.

- Risk adjustment directionality. Most of the ACA health plan issuers that estimated a nonzero risk adjustment transfer amount accurately predicted the direction of the transfer amount. We observe that the ACA health plan issuers that expected to receive a risk adjustment transfer underestimated the transfer amount in aggregate. Issuers that estimated a risk adjustment payment also underestimated the transfer amount in aggregate.

- Varying reinsurance parameters. ACA health plan issuers under-accrued for recoveries3 from the transitional reinsurance program by $1 billion. This is largely due to the increased coinsurance rate announced after financial statement estimates were developed.

- Risk corridor proration. Proration of the risk corridor program caused $2.5 billion in financial losses to ACA health plan issuers in 2014 relative to the actual results with no proration, based on payments made to date.4 ACA health plan issuers anticipated, perhaps inadvertently, $1.5 billion of the risk corridor proration loss in 2014 financial statements. The result is a $1 billion adverse financial impact of actual risk corridor results.

- Cumulative risk corridor uncertainty. Risk corridor estimates are a function of other estimates and contingent events, including incurred-but-not-reported (IBNR) claim liabilities, risk adjustment, reinsurance, and the collectability of the risk corridors. As a result, any degree of uncertainty in other estimates increases the uncertainty in risk corridor estimates. A similar degree of cumulative uncertainty exists for medical loss ratio (MLR) rebate estimates, which incorporate all 3R actual results.

- Issuer-specific variation. We observe a significant degree of variation in the ACA health plan issuer results. While the focus of this paper is on industry aggregate results, issuer-specific results vary widely from the industry averages.

Figure 1 presents the aggregate actual 3R results relative to ACA health plan issuer estimates as of December 31, 2014. The last column measures the aggregate industry-wide profit or loss attributable to 2014 that was not recognized on 2014 financial statements (and would need to be recognized in a subsequent reporting period).

Figure 1: Financial Gain/(Loss) of Actual 3R Results Relative to Accrued Amounts as of December 31, 2014 (millions)

| 3R Program | Accrued Amounts | Actual Results | Gain/(Loss)5 |

| Risk Adjustment | $230.2 | $0 | ($230.2) |

| Reinsurance | $6,873.0 | $7,886.0 | $1,013.0 |

| Risk Corridors | $1,038.6 | $0 | ($1,038.6) |

| Aggregate | $8,141.9 | $7,886.0 | ($255.9) |

The aggregate effect of the 3R results relative to 2014 ACA health plan issuer recognized earnings is a negative $255.9 million financial impact. In aggregate, the industry overstated the value of risk corridors and understated the value of reinsurance by approximately offsetting amounts (though likely for very different reasons). The published coinsurance parameter for the transitional reinsurance program was 80% at the time that 2014 financial statements were developed. The actual coinsurance parameter was revised to 100% after 2014 financial statements were submitted. ACA health plan issuers overestimated the value of risk adjustment by $230.2 million. While these results are aggregate industry-wide totals, actual-to-estimated 3R results vary widely across ACA health plan issuers.

Estimating accruals for the 3 Rs is complex. The level of complexity varies by program, largely as a function of the information available at the time the estimates are being developed.6 Figure 2 presents the complexity of estimation for each 3R component.

Figure 2: Complexity of 3R Estimates

| 3R Program | Complexity |

| Risk Adjustment | Very high |

| Reinsurance | Medium |

| Risk Corridors | High |

While the complexity of developing risk corridor estimates is “high,” the result of this estimate is partly a function of risk adjustment estimates, which have a “very high” degree of complexity. Risk corridor estimates also turned out to be subject to considerable legislative and political uncertainty.7 The remainder of this paper will examine each 3R component individually, the effect on ACA health plan financial strength, and considerations for developing 3R estimates for 2015 and future financial statements.

Key dates for 2014 3R information

- March 1, 2015: 2014 financial statements due to state regulators

- May 15, 2015: EDGE server data submission deadline (originally April 30)

- June 17, 2015: Final reinsurance coinsurance parameter released

- June 30, 2015: Risk adjustment and reinsurance results published for all ACA health plan issuers

- August 7, 2015: Postponement of preliminary risk corridor results

- October 1, 2015: Release of risk corridor proration percentage

- November 19, 2015: Risk corridor results released

Permanent risk adjustment

Risk adjustment transfers generally net to zero separately within the individual and small group markets in each state. Risk adjustment is a zero-sum program, which means that industry-wide payments must equal industry-wide receipts. The risk adjustment transfer is a function of an issuer’s own experience and the experience of the market as a whole. As of February 2015, when 2014 annual statements were prepared, there were no official market-wide risk score metrics available that would help issuers estimate what transfer payment their own experience might produce. This lack of published market-wide information made it challenging for issuers to develop estimates of risk adjustment accruals for their 2014 annual statements. It is possible that variation in risk adjustment transfer amount estimates may decrease if market-wide information is made available at the time that financial statements are developed.

Over half of ACA health plan issuers recorded $0 in risk adjustment transfers on their 2014 annual statements. Annual statements do not typically provide the issuer’s rationale behind the estimated amounts.8 We speculate that there were two general reasons for estimating a $0 risk adjustment transfer amount.

- An issuer may have conducted an analysis and determined that the most likely transfer amount was near zero. This would be a plausible result for an issuer with a large market share.

- The issuer, potentially in consultation with its auditors, may have determined that it was not possible to develop a reasonable estimate for the risk adjustment accrual and recorded $0.9 The $0 risk adjustment estimate could represent an acknowledgment that it was not possible to determine whether a receipt or payment was the more likely outcome, and using $0 should represent the market mean, which is a reasonable estimate absent reliable data.10

Of the 49% of issuers that did record a nonzero risk adjustment transfer amount on their 2014 annual statements, a majority of the estimates—84%—were directionally correct. Figure 3 shows how the direction of actual risk adjustment results compares with the estimated direction by proportion of ACA health plan issuers.11

Figure 3: Directionality of Risk Adjustment Transfer Amounts by Percent of ACA Health Plan Issuers as of December 31, 2014

| Actual Receipts | Actual Payments | No Actual Transfer | Total | |

| Accrued Receipts | 21% | 5% | 0% | 26% |

| Accrued Payments | 3% | 20% | 0% | 23% |

| Accrued No Transfer | 23% | 28% | 0% | 51% |

| Total | 47% | 53% | 0% | 100% |

The industry’s risk adjustment estimates were largely directionally correct for issuers that estimated a nonzero risk adjustment transfer amount. However, the industry’s total estimated risk adjustment accruals resulted in receivables of approximately $230.2 million. The risk adjustment program is defined to be a zero-sum program. This implies that there is $230.2 million in financial statement optimism from the risk adjustment program alone, because this variation must be corrected in future reporting periods. We observed two contributing factors to this result:

1. Among the issuers that correctly identified the direction of their risk adjustment transfers, the magnitude of transfer estimates was underestimated. This is the case for both receipts and payments, but is more significant for transfer receipts.

2. Among the issuers that incorrectly estimated the direction of their risk adjustment transfers, the net result was strongly unfavorable compared with what the issuers in this cohort estimated.

Figure 412 presents risk adjustment estimates by the direction of estimate on 2014 financial statements.

Figure 4: Risk Adjustment Receipts (Payments) by Accrued Directionality Issuer Cohort as of December 31, 2014 (millions)

| Accrued Direction | Accrued | Actual | Gain/(Loss) |

| Correctly Accrued Receipts | $852.9 | $1,180.0 | $327.1 |

| Correctly Accrued Payments | ($752.4) | ($944.3) | ($191.9) |

| Accrued Zero | $0 | $68.0 | $68.0 |

| Incorrectly Accrued Direction | $129.7 | ($303.7) | ($433.4) |

| Total | $230.2 | $0 | ($230.2) |

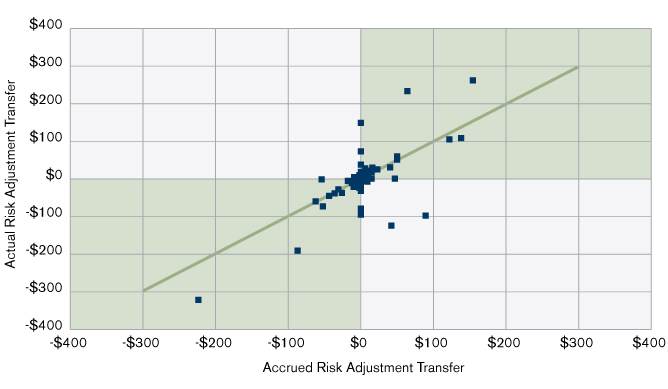

Figure 5 presents estimated risk adjustment transfers compared with actual risk adjustment transfer results for each health plan issuer.13 The diagonal line illustrates instances where estimated transfer amounts match actual transfer amounts.

Figure 5: Actual-to-Accrued ACA Health Plan Risk Adjustment Transfers as of December 31, 2014 ($ millions)

Each point in Figure 5 represents the actual-to-estimated results for a single ACA health plan issuer. The upper-right and lower-left quadrants are highlighted to illustrate the issuers that correctly estimated the direction of the risk adjustment transfer payment.

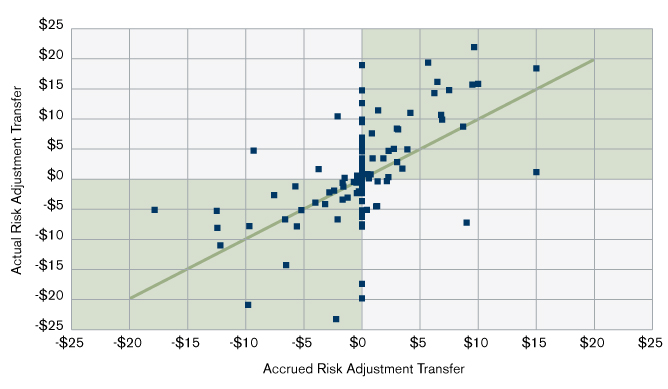

Figure 6 presents the same data as Figure 5, but truncated at $25 million to provide a detailed perspective on actual-to-estimated risk adjustment results. Larger transfer amounts that exceed $25 million in Figure 5 are excluded from Figure 6.

Figure 6: Actual-to-Accrued ACA Health Plan Risk Adjustment Transfers as of December 31, 2014 ($ millions)

Figure 6 illustrates two important observations on risk adjustment estimates relative to actual amounts. First, approximately half of all ACA health plan issuers recorded a $0 risk adjustment accrual. This is illustrated in Figure 6 by the number of points that fall along the vertical axis. Second, most ACA health plan issuers that estimated a nonzero risk adjustment accrual correctly anticipated the directionality of the actual accrual. This is illustrated in Figure 6 by the number points that fall in either the lower-left (transfer payment) or upper-right (transfer receipt) quadrants of the plot area, which are highlighted in green.

Transitional reinsurance

Industry-wide reinsurance estimates were less than actual amounts, which is the only 3R program with this observed relationship. This result is primarily driven by an increase in the coinsurance parameter from 80% to 100%, which CCIIO announced on June 17, 2015, after annual statements had already been developed.14 Figure 7 presents an attribution of the actual-to-estimated reinsurance amounts.

Figure 7: Transitional Reinsurance Estimate Attribution as of December 31, 2014 (millions)

| Amount Accrued by ACA Plan Issuers | $6,873.0 |

| Coinsurance Variation | $1,718.3 |

| Other Variation | ($705.3) |

| Actual Reinsurance Amount | $7,886.0 |

It is challenging to allocate the difference between the last two rows of the figure (i.e., coinsurance variation versus other variation). The details behind an issuer’s accruals are not available in annual statements, and so it is possible that some issuers anticipated an increase in the coinsurance rate. The other possible explanation is that some issuers overestimated the volume of their claims that would be eligible for reimbursement.

Related articles

- Risk Corridors Episode IV: No New Hope

- Transitional reinsurance at 100% coinsurance: What it means for 2014 and beyond

- Headwinds cause 2014 risk corridor funding shortfall

- Update on canceled plans: Will changes to 2014 reinsurance and risk corridor programs provide financial relief?

- Risk adjustment: Overview and opportunity

- Risk corridors under the ACA

A new consideration for 2015 financial statement transitional reinsurance estimates is the 2014 reinsurance assessments collected that will be applied to 2015. With a total 2014 assessment of $9.7 billion, approximately $1.8 billion will be carried forward to 2015. While additional funds carried forward to 2015 could benefit ACA health plan issuers that sell individual products, it is unclear to what extent the current published 2015 reinsurance parameters already anticipate 2014 carryover funds.15

Temporary risk corridors

The risk corridor program has a long and complicated history, which has been chronicled elsewhere.16 Although the ACA requires payments to be made to issuers if owed, Congress has not appropriated any funds for that purpose at this time. Current congressional appropriations essentially render risk corridor a budget-neutral program. Therefore, as with risk adjustment, industry-wide payments must equal or exceed industry-wide receipts for this program. On October 1, 2015, CCIIO announced a risk corridor payment proration rate of 12.6% for 2014 plans because requests for reimbursement greatly exceeded payments into the program.17 With this announcement, ACA plan issuers that expected to receive risk corridor payments will initially receive 12.6% of the full anticipated payment.

Based on current regulatory guidance, outstanding risk corridor receivables from 2014 take priority over receivables from the 2015 and 2016 plan years.18 This prioritization should be considered when estimating the collectability of risk corridors for 2015 and future financial statement periods. The most recent guidance from the National Association of Insurance Commissioners (NAIC) is to include risk corridor receivables for the 2015 and 2016 plan years as non-admitted assets until the 2014 shortfall is paid in full and there is sufficient information to support the likelihood that receivables from later years will be collected. The guidance also provides for nonadmission of additional recoveries from 2014 until additional information becomes available about the amount and timing of payments.19 Payments into the risk corridor program are still expected to be included as covered liabilities for 2015 and 2016 financial reporting periods.

ACA health plan issuer profitability

In an effort to contextualize the degree of uncertainty related to the 3 Rs, we estimated the financial actual-to-estimated results in Figure 1 above on a percent of premium basis. Figure 8 presents our results in these bases.

Figure 8: Financial Gain/(Loss) of Actual-to-Accrued 3R Results as of December 31, 2014 (millions)

| Program | Total Dollars | % of Premium |

| Risk Adjustment | ($230.2) | (0.4%) |

| Reinsurance | $1,013.0 | 1.8% |

| Risk Corridors | ($1,038.6) | (1.8%) |

| Aggregate | ($255.9) | (0.4%) |

Based on our consulting experience, typical industry targeted profit margin provisions typically range from 2% to 4% of premium for individual and small group comprehensive major medical products (though actual results have fallen short of this range in recent years in the individual market). The percent of premium column in Figure 8 relative to typical industry profit margin provisions demonstrate the extent to which 3R uncertainty affects the financial performance of ACA health plan issuers.

ACA health plan issuer solvency

Reviewing our results in the context of risk-based capital (RBC) provides additional insight into the effect of the 3 Rs on ACA health plan issuer financial strength. Actual 3R settlements relative to estimated values improve the financial position for 51% of ACA health plan issuers and deteriorates the financial position for 49% of ACA health plan issuers. Figure 9 presents the number of ACA health plan issuers that would have triggered an RBC event if actual 3R results were accurately estimated on 2014 financial statements.

Figure 9: Number of ACA Health Plan Issuers With Potential RBC Event Triggered by Actual-to-Accrued 3R Variation as of December 31, 2014

| RBC Event | RBC Range | Number of Plans |

| Company Action Level | 150% - 200% | 3 |

| Regulatory Action Level | 100% - 150% | 0 |

| Authorized Control Level | 70% - 100% | 0 |

| Mandatory Control Level | 0% - 70% | 4 |

| Accounting Insolvency | < 0% | 5 |

It is difficult to report aggregate RBC results because of the nuances of the RBC formula, including the diversification benefit and affiliate risk. This difficulty is exacerbated by the legal structure of some ACA health plan issuers, with multiple subsidiaries and differing ownership structures (which also makes it difficult to aggregate total adjusted capital). As a result, we focused on the effect of solvency for individual ACA health plan issuers at the individual statutory entity level rather than the aggregate effect on industry-wide solvency. All issuers included in Figure 9 transitioned from a stronger solvency position. Issuers that remained within the company action level with estimated and actual 3R results are excluded from this table.

Larger issuers generally have capital and surplus to support other lines of business. As a result, the effect of 3R actual-to-estimated variation on RBC levels is generally less impactful for larger ACA health plan issuers.

Figure 9 re-calculates RBC position by substituting final 3R settlements for the 3R amounts accrued on the 2014 annual statements. The 3 Rs are not the only accrual that is subject to uncertainty. Although this table assumes no changes to any accruals besides the 3 Rs, it is possible that other accruals could have emerged differently than expected.

Methodology

Note 24 in the National Association of Insurance Commissioners (NAIC) 2014 health annual statement includes detail related to 3R estimates. Titled Retrospectively Rated Contracts & Contracts Subject to Redetermination, Note 24 summarizes balance sheet and income statement estimates for risk adjustment, risk corridors, and reinsurance. In general, we summarized 3R estimates for ACA health plans using SNL Financial. Some issuers in California are regulated by the California Department of Managed Health Care. Our solvency analysis does not include these plans because RBC information for them is not readily available. These issuers, as well as some domiciled in New York, do not file publicly available financial statements, including Note 24. As a result, disclosures for these issuers were retrieved from footnotes where available, but such detail was not always available. Companies that did not file a 2014 annual statement because of insolvency are likewise not included in the summaries of annual statement data. Note 24 data is reported at the issuer level. As a result, we were not able to perform an analysis of actual-to-estimated results at a more granular level, including by market (individual/small group) or by state.

Actual 3R amounts are based generally on two CCIIO publications: one publication for risk adjustment and reinsurance results20 and a separate publication for risk corridor results.21 Risk adjustment transfer amounts in Massachusetts are based on a state-specific risk adjustment methodology. We summarized actual risk adjustment transfer amounts for ACA health plans in Massachusetts based on information published by the Commonwealth Health Insurance Connector Authority.22 We computed premiums in Figure 8 premiums using the risk adjustment information published by CCIIO and the Commonwealth Health Insurance Connector Authority. The CCIIO risk adjustment publication includes information related to national average premium and billable member months.

The CCIIO publications summarize information by Health Insurance Oversight System (HIOS) Issuer ID, created for each issuer that must submit data under the ACA. Statutory data do not include the HIOS Issuer ID but do include a separate NAIC ID, which is a unique identifier for each statutory insurance entity assigned by the NAIC. We matched HIOS Issuer ID to NAIC ID using federal Employer Identification Number (EIN) to form the basis for our research. There is a many-to-one relationship between HIOS Issuer ID and NAIC ID, which is due to the fact that separate HIOS IDs are assigned by state. The Note 24 data do not break down accruals by state or market (individual, small group), and our research therefore aggregates the actual 3R data at the issuer level in order to be comparable to the level of detail included in the Note 24 data. While we conducted our research at the individual NAIC entity level, some exhibits in this paper present results at the parent company level.

Important disclosures

This paper has been prepared for the specific purpose of discussing the results of our ACA risk mitigation program research. This information may not be appropriate, and should not be used, for any other purpose. This paper does not intend to provide any accounting or legal advice. We recommend that you consult with your accounting or legal advisors for accounting or legal advice. The authors of this paper are neither accountants nor attorneys.

In performing this analysis, we relied on publicly available information and data. We did not perform an audit of the data but did perform a high-level review for reasonability and modified certain data points that were clearly erroneous. If this data or information is inaccurate or incomplete, the results of our analysis may likewise be inaccurate or incomplete.

This report relies on data and information available as of the date of publication. Rules and regulations regarding the ACA and accounting standards have evolved over time and may continue to do so, which could affect the conclusions in this paper.

Guidelines issued by the American Academy of Actuaries require actuaries to disclose their professional qualifications in actuarial communications. The authors are members of the American Academy of Actuaries and meet the qualification standards for performing this analysis.

1U.S. Congress, Patient Protection and Affordable Care Act, Sections 1341-43. Retrieved February 3, 2016, from https://www.gpo.gov/fdsys/pkg/PLAW-111publ148/pdf/PLAW-111publ148.pdf.

2Federal Register (March 23, 2012). Patient Protection and Affordable Care Act; Standards Related to Reinsurance, Risk Corridors and Risk Adjustment; Final Rule. Retrieved February 3, 2016, from https://www.gpo.gov/fdsys/pkg/FR-2012-03-23/pdf/2012-6594.pdf.

3Transitional reinsurance is funded by assessments on health insurers and self-funded health plans. These assessments are also reported on financial statements and are potentially subject to mis-estimation, but this paper only analyzes receivables from the program rather than contributions to it.

4The Centers for Medicare and Medicaid Services (CMS) has stated that any collections from the risk corridor program for the 2015 and 2016 plan years would first be used to pay down any deficit from 2014 (see “Risk Corridors and Budget Neutrality, retrieved February 3, 2016, from https://www.cms.gov/CCIIO/Resources/Fact-Sheets-and-FAQs/Downloads/faq-risk-corridors-04-11-2014.pdf). The final shortfall will therefore likely be less than $2.5 billion, although if 2015-2016 collections are of approximately the same magnitude as 2014 collections, the shortfall would still be substantial without additional appropriations to fill in the gap.

5 The “Actual Results” column and the “Gain/(Loss)” column include results from a few companies for which we did not have 2014 annual statements, and the estimated risk adjustment transfers for such companies are recorded as $0 in this figure. Companies that were insolvent did not submit annual statements, and a few companies domiciled in New York are regulated as Prepaid Health Services Plans and did not have annual statements available. Had estimates been available for these companies, it likely would have moved the Gain/(Loss) values, but it is not possible to know by how much or in which direction.

6Chamblee, M. P. (March 20, 2014). ACA’s Impact on Financial Statements. Retrieved February 3, 2016, from http://us.milliman.com/insight/2014/ACAs-impact-on-financial-statements/.

7Norris, D,, Perlman, D., & Leida, H.K. (December 2014). Risk Corridors Episode IV: No New Hope. Milliman Healthcare Reform Briefing Paper. Retrieved February 3, 2016, from /-/media/Milliman/importedfiles/uploadedFiles/insight/2014/risk-corridors-no-new-hope.ashx.

8This information would typically be discussed in the actuarial memorandum accompanying the annual statement, but the memorandum is not publicly available.

9 Statutory accounting guidance related to risk adjustment (as well as transitional reinsurance and temporary risk corridors) can be found in SSAP No. 107 (National Association of Insurance Commissioners [NAIC], Accounting Practices and Procedures Manual as of March 2015). This accounting standard acknowledges the uncertainties in the estimate and cites the statutory accounting principle of conservatism. This principle may have led to issuers recording $0 rather than a very uncertain receivable. However, with risk adjustment, $0 is not necessarily conservative.

10Both SSAP Nos. 4 and 5, in defining assets and liabilities, respectively, require that the future receipt or payment be probable. See NAIC Accounting Practices and Procedures Manual as of March 2015.

11Figure 3 is based on statutory data aggregated at the parent company level.

12Figure 4 is based on statutory data aggregated at the parent company level.

13Figure 5 is based on statutory data aggregated at the parent company level.

14Center for Consumer Information and Insurance Oversight (June 17, 2015). Transitional Reinsurance Program: Pro Rata Adjustment to the National Coinsurance Rate for the 2014 Benefit Year. Retrieved February 3, 2016, from https://www.cms.gov/CCIIO/Programs-and-Initiatives/Premium-Stabilization-Programs/The-Transitional-Reinsurance-Program/Downloads/RI-Payments-National-Proration-Memo-With-Numbers-6-17-15.pdf.

15Perlman, D, Norris, D., & Leida, H.K. (June 2015). Transitional reinsurance at 100% coinsurance: What it means for 2014 and beyond. Milliman Healthcare Reform Briefing Paper. Retrieved February 3, 2016, from /-/media/Milliman/importedfiles/uploadedFiles/insight/2015/2044hdp_20150710.ashx.

16Katterman, S (October 2015). Headwinds Cause 2014 Risk Corridor Funding Shortfall. Milliman Healthcare Reform Briefing Paper. Retrieved February 3, 2016, from /-/media/Milliman/importedfiles/uploadedFiles/insight/2015/2105hdp_20151103.ashx.

17Center for Consumer Information and Insurance Oversight (October 1, 2015). Risk Corridors Payment Proration Rate for 2014. Retrieved February 3, 2016, from https://www.cms.gov/CCIIO/Programs-and-Initiatives/Premium-Stabilization-Programs/Downloads/RiskCorridorsPaymentProrationRatefor2014.pdf.

18Katterman, S (October 2015). Headwinds Cause 2014 Risk Corridor Funding Shortfall. Milliman Healthcare Reform Briefing Paper. Retrieved February 3, 2016, from /-/media/Milliman/importedfiles/uploadedFiles/insight/2015/2105hdp_20151103.ashx.

19NAIC (November 5, 2015). INT 15-01: ACA Risk Corridors Collectibility. Retrieved February 3, 2016, from http://www.naic.org/documents/committees_e_app_eaiwg_related_int_1501_risk_corridors.pdf.

20Center for Consumer Information and Insurance Oversight (September 17, 2015). Summary Report on Transitional Reinsurance Payments and Permanent Risk Adjustment Transfers for the 2014 Benefit Year. Retrieved February 3, 2016, from https://www.cms.gov/CCIIO/Programs-and-Initiatives/Premium-Stabilization-Programs/Downloads/RI-RA-Report-REVISED-9-17-15.pdf.

21Center for Consumer Information and Insurance Oversight (November 19, 2015). Risk Corridors Payment and Charge Amounts for Benefit Year 2014. Retrieved February 3, 2016, from https://www.cms.gov/CCIIO/Programs-and-Initiatives/Premium-Stabilization-Programs/Downloads/RC-Issuer-level-Report.pdf.

22Massachusetts Health Connector (July 6, 2015). 2014 Risk Adjustment Settlement Update. Retrieved February 3, 2016, from https://betterhealthconnector.com/wp-content/uploads/board_meetings/2015/2015-07-09/Board-Memo-Risk-Adjustment-Update-070615.pdf.