The Patient Protection and Affordable Care Act (ACA) introduced rules around the richness of benefit plans offered by carriers in the marketplaces. By now, carriers have adjusted to the realities of bronze, silver, gold, and platinum metallic tiers. Prior to the introduction of these metallic levels, carriers faced very few restrictions with regard to how rich or lean benefit plans could be. Carriers in the pre-ACA world could in theory offer a continuous benefit richness slope composed of a wide variety of rich and lean benefit plans. Furthermore, a benefit plan’s marketed benefit richness, including the use of pricing plan factors in the small group market among brokers, was directly tied to that plan’s priced benefit richness. This is no longer the case under the ACA, as a plan’s de facto benefit richness for marketing purposes is designated via the Actuarial Value Calculator (AVC), yet that same plan’s pricing benefit richness is determined via the carrier’s pricing model of choice. As this paper discusses, consumers may not be aware of the differences between Actuarial Values (AVs) from the AVC and benefit richness values used in pricing. If they were known, they could lead consumers to make different benefit plan choices. Furthermore, we explore the extent to which the ACA has introduced discontinuities in what could otherwise be a continuous benefit richness slope. In short, the asymmetrical approach to different models may lead to a narrower range of choices for consumers.

How different models for marketing and pricing may get in the way of transparency for consumers

The ACA requires that all ACA-compliant non-grandfathered plan designs yield an Actuarial Value—determined using the AVC created by the U.S. Department of Health and Human Services (HHS)—that fits in the prescribed ranges by metallic level, shown in the table in Figure 1.

Figure 1: HHS-Permissible Actuarial Value Ranges

The Actuarial Value represents HHS’s interpretation of a plan’s benefit richness. Benefit plans that fail to meet the AV requirements cannot be offered. Once a plan meets the AV requirements for a desired metallic tier, it is assigned that metallic designation, which is then intended to assist consumers making selections in the marketplaces. Therefore, consumers picking a bronze plan may infer that the plan generally pays between 58% and 62% of medical costs. Likewise, the conclusion of picking a gold plan may be that in general it covers between 78% and 82% of medical costs. But how close are these assumptions to reality? That is, are consumers getting what they pick? The answer is that in many cases they are not, which is due to the potentially significant differences in results between the AVC and pricing models that use actual claims experience.

Although the AVC is the official HHS tool for designating a plan’s benefit richness for the purpose of helping consumers make informed purchasing decisions, carriers generally do not use the Actuarial Value Calculator to determine a plan’s benefit richness for pricing purposes. Rather, carriers use pricing models with data that is either representative of their own experience, or has been adjusted to reflect their unique single risk pool characteristics. Furthermore, pricing models in general tend to employ a higher level of accuracy and fewer simplifying assumptions than those used in the AVC.

The table in Figure 2 highlights the inconsistency between AVC values and those attained through a model that uses actual claims experience for a set of plans representative of the marketplace. We used the 2016 AVC and our pricing model represents values for 2016. The Methodology section of this paper explains how the plan designs in our analysis were chosen.

Figure 2: AVC Value Ranges vs. Ranges From Pricing Model That Uses Claims Experience

Although every benefit plan in our analysis meets the AV requirements, Figure 2 shows that many of the plans we tested have pricing values outside the allowable metallic ranges. For instance, a substantial number of gold plans in our analysis have levels of coverage above 82%, the maximum gold coverage designated by the AVC. Similarly, about half of the silver plans tested have coverage above 72%, which is beyond the maximum silver coverage in the AVC. Conversely, some plans have coverage below the minimum required by the AVC. Overall, because of the wider brackets in the pricing values, almost half of the plans tested offered levels of coverage outside the allowable AVC ranges by metallic tier when AV is measured by the pricing model.

There may be variations if the above comparison were to be conducted for a specific region. Furthermore, each carrier may have its own method for determining the pricing benefit richness of each benefit plan. However, our analysis of a representative set of benefit plans in the marketplaces priced using an actuarial pricing model based on claims experience indicates that a large percentage of plans in the marketplaces may be offering coverage that’s not in line with the level of coverage calculated by the AVC.

What does this mean to consumers? For one, consumers make purchasing decisions based on the levels of coverage advertised to them. The disconnect between AVs from the AVC and pricing values from actuarial pricing models may be misleading to consumers shopping for plans in the marketplaces. There are cases where consumers may be purchasing less coverage than advertised via the plan’s AV. In other cases, consumers are paying a higher price for plans with richer coverage than perhaps wanted. While these consumers may be happy to discover that they are purchasing richer coverage, they may be doing so unwittingly at the time of sale. Our analysis showed that roughly half of all plans tested had a benefit richness value outside the designated AV ranges. This means that a significant number of consumers may be unknowingly purchasing plans with actuarial values that when measured with the pricing model are outside the AVC ranges. Consequently, two plans that are supposedly equivalent and comparable (e.g., two silver plans) may not be so equivalent in reality. In the absence of this information, consumers may not be making the most informed choices when shopping for plans in the market places.

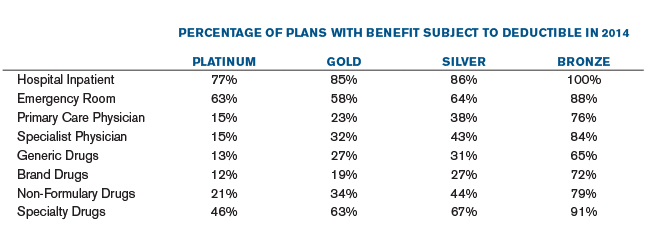

Furthermore, along with the annual limitations on the maximum out-of-pocket amount, the AVC places restraints on the plan designs that carriers can offer. As an example, approximately 80% of all bronze plans in 2014 applied deductible and coinsurance on primary care services in order to meet the bronze AV range, while only 15% of platinum plans did so. The table in Figure 3 shows the occurrence of deductible by type of service from the 2014 plan designs in the marketplaces.

Figure 3: Occurrence of Deductible by Benefit Type in 2014

The nature of the AVC combined with the annual limitation on the maximum out-of-pocket amount makes it very difficult to create bronze plan designs with copays on select services. The lower the AV, the less flexibility carriers have in creating plan designs that pass the AVC test. This means fewer choices for consumers, as there appears to be less diversity of plan designs at the lower AV levels.

How discontinuities in the benefit richness slope limit consumer choice

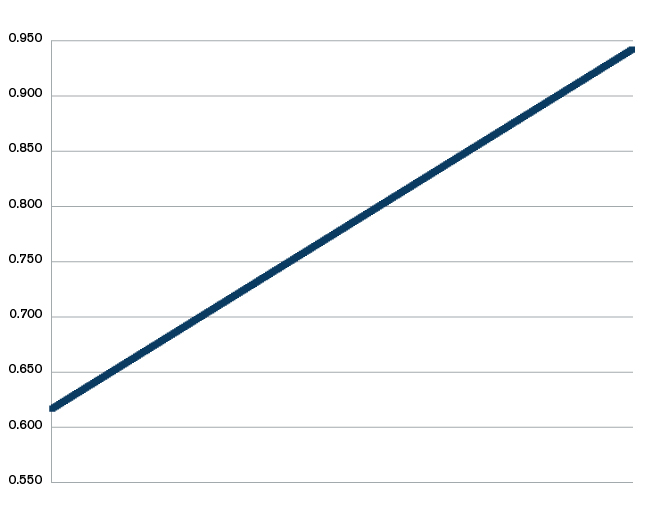

As previously discussed, the use of separate models to designate and price a plan’s benefit richness causes a disconnect between the perceived plan’s value and its true level of coverage. The use of different models also introduces a separate direct impact on consumer choice. Prior to the ACA, carriers in a given market were capable of offering what essentially amounted to a continuous spectrum of coverage levels. Consumers were often able to find plan designs along a benefit richness slope akin to the one depicted in Figure 4. For purposes of illustration, the starting and ending points are the same as those that we determined for the representative ACA slope using our pricing model.

Figure 4: Illustrative Pre-ACA Benefit Richness Slope

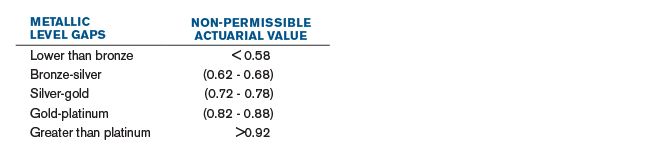

The permissible Actuarial Value ranges by metallic tier imply that carriers cannot design plans that yield Actuarial Values in the ranges outlined in the table in Figure 5.

Figure 5: HHS Non-Permissible Actuarial Value Ranges

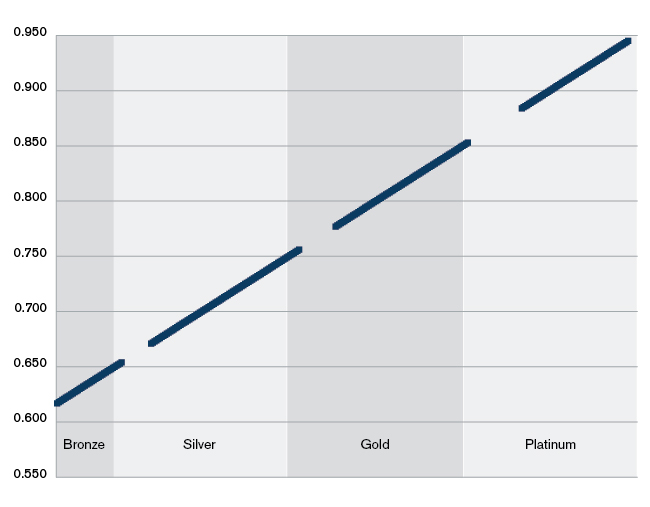

If pricing models yielded the same results as the AVC, the ACA benefit richness slope would have the entire range of discontinuities outlined in Figure 5. As we have seen, however, the use of actuarial pricing models leads to plans with benefit richness factors outside the AV permissible ranges, while still passing the AVC. This helps expand consumer choice, as the gaps above are closed and consumers are able to select plans with coverage outside the officially designated levels of coverage. Still, how much additional choice is introduced? Figure 6 displays the benefit richness slope of our set of plans representative of the 2014 marketplace.

Figure 6: Sample ACA Benefit Richness Slope

As Figure 6 illustrates, even if some plans end up with benefit richness values outside the AVC-permissible ranges, discontinuities in a given market’s benefit richness slope may still exist. This means that consumers who previously were able to purchase plans with a level of coverage between 86% and 88%, as an example for illustrative purposes, may no longer be able to do so under the ACA. Considering that one of the main tenets of the law was to expand choice for consumers, the imposition of metallic level requirements has a direct impact on the design and resulting benefit values that carriers can offer. Consumer choice may have been expanded with the number of carriers participating in the marketplaces, but the pre-ACA freedom to select benefit richness levels may have been eroded.

Can anything be done to address these issues?

Ultimately, the only metallic tier that matters for subsidy purposes is the silver tier. A way to restore choices to pre-ACA levels would be to simply have two plan tiers: eligible for subsidies and not eligible for subsidies. Plans eligible for subsidies would essentially replace the current silver tier, and would be used to determine the second-lowest plan in this category for the purpose of determining the advanced premium tax credit. Furthermore, only plans that pass the designated AVC subsidy range (either the current silver range or something else) would be eligible for cost share reduction subsidies. Any other plan outside the subsidy-eligible AVC range could still be offered in the marketplaces as long as it stays within a defined global range of permissible AVC values (0.55 to 0.95 for instance). Carriers would then be required to publish each plan’s benefit richness using a common measure among all carriers instead of using the current metallic tiers to identify a plan’s perceived level of coverage. This alternative would clearly have consequences on the entire program, so any changes to the current rules would have to be carefully designed and implemented. But, as this paper has discussed, having information on a plan’s true level of coverage may help consumers make more informed plan selection choices in the marketplaces.

Note that a carrier could presumably design plans with unusual cost-sharing schemes that would pass the AVC and may result in benefit richness values within the gaps shown in Figure 6. As an example, very low benefit richness values (and passing AVs) might be achieved by increasing the member cost sharing well past 50% for some benefits. However, in our analysis of all 2014 marketplace plans, these types of plans were not prevalent. Furthermore, states may prevent carriers from imposing member cost sharing past a certain threshold, as this may be considered discriminatory. Therefore, we did not include these types of plans in our analysis.

Methodology

Our sample of representative 2014 plan designs started with downloading all 2014 marketplace benefit information from the website managed by the Centers for Medicare and Medicaid Services (CMS) at https://www.healthcare.gov/health-and-dental-plan-datasets-for-researchers-and-issuers/. We then determined ranges for all the possible values of each AVC benefit feature from the entire 2014 set. We further expanded these ranges to include more possible values to choose from. Because some 2014 plan designs no longer pass the 2016 AVC, we used these ranges to randomly generate a large number of entire plan designs instead of only using actual 2014 plan designs. We also put rules in place to ensure that the plan designs generated were reasonable. For example, all plans had cost sharing for professional services equal to or lower than for specialist services. Therefore, our plan designs used actual 2014 marketplace plan attributes as the basis, adjusted as needed in order for each entire plan design to pass the 2016 AVC.

Our pricing model determines 2016 benefit richness on a seriatim basis. The pricing model simulates the adjudication of claims at the claim, member, and contract levels for each benefit plan, using one very large national-based risk pool. Consistent with ACA rules, health status was not considered in the calculation of each plan’s benefit richness factor. Furthermore, the underlying data was not adjusted for any morbidity differences such as pent-up demand that could occur in the projection period. And any provider contracting changes that could occur in the future have not been taken into consideration. We did, however, apply induced demand adjustment factors during the calculation of each plan’s benefit richness, based on the plan’s metallic designation. We used HHS’s induced demand adjustment factors included in the HHS risk adjustment model. In the absence of induced demand adjustments on benefit richness factors, the comparison of benefit richness factors to Actuarial Values would be inconsistent, as the AVC includes adjustments for induced demand in the calculation of Actuarial Values.

Disclosures

This communication has been prepared for the specific purpose of discussing the interactions between the Actuarial Value Calculator and benefit richness values determined by carriers using their own pricing models. This information may not be appropriate, and should not be used, for any other purpose.

In performing this analysis, we relied on information published by others. If this data or information is inaccurate or incomplete, the results of our analysis may likewise be inaccurate or incomplete.

Milliman does not intend to benefit or create a legal duty to any third-party recipient of this work. This communication must be read in its entirety. Differences between our estimates and actual amounts depend on the extent to which future experience conforms to the assumptions made in this work. Actual amounts will differ from projected amounts to the extent that actual experience deviates from expected experience.

Guidelines issued by the American Academy of Actuaries require actuaries to include their professional qualifications in actuarial communications. Pedro Alcocer is a member of the American Academy of Actuaries and meets its qualifications standard to perform the analysis and render the actuarial opinion contained herein. The author of this report is not a lawyer, and nothing in this report should be construed as legal advice.