Price differentiation: A change in paradigm

A few years ago, it was stylish for retail insurers to suspect, look for, and find subtle risk effects within the market, taking the slightest indications of trends in the data as a proof for micro-segmenting risk portfolios into ever smaller pieces. Most insurers understand all too well how statistically dangerous the practice has been and how easily existing evidence can be undermined by the arrival of new data cohorts. But no one was much concerned about it because they thought clients wouldn’t notice, and because seeking and developing new segments makes for a nice growth story.

But the Internet is bringing a new truth to the game, where predictive power operates much like weather reports—everyone can check the predictive power! The main driver for price variation of 50% and more is the inherent uncertainty in the technical pricing rather than the different claims handling of insurers or the different portfolio mixes that they attract.

A trivial thing becoming a hot topic: Who knows the market prices (better)?

From the insurer’s perspective: Insurers don’t know what competitors do in detail. If you ask the responsible actuary or any salesperson, you will only get general opinions and at maximum they might be able to give you a few pricing points among the whole “cloud” of prices available on the market. As a result, traditional sales agents often panic when a client comes through the door, waving a few offerings, or saying that the market has been checked already. It ends up in giving a huge and securing discount if sales objectives need to be fulfilled or the client looks potentially interesting to the agent.

From the client’s perspective: Although clients can easily check the prices for retail products on the internet, most don’t yet understand their new power. They still often suspect that the insurers know their prices better and that differences will have meaning and so most still hesitate choosing the lowest price or taking offers from insurers that they don’t know yet. They can hardly believe that they know their individual prices better than the offering panel of insurers. This is no surprise—who would tell them, really?

Also, some clients would still assume that when they receive a huge discount, the insurance company will still make money (i.e., “they offered me this discount of X%, so they had at least X% profit within their offering!”).

This situation will certainly not remain forever. Clients will definitely become more efficient buyers once they understand that they can use those price differences to behave more opportunistically and they will more frequently move to another insurer. Examples of customer behavior of this kind in tough and differentiated markets, such as the U.K., point in that direction. Even in moderate markets, such as Switzerland, there is a strong tendency for clients to start picking and pressing sales agents, because of “cheaper” offerings from competitors.

Is the price variance on the market for commodity products sustainable?

Let’s take an example: Everyone would agree that third-party motor insurance cover is not very different across the market, at least in a given country. On the claims side, one cannot do much about an incurred liability claim. However, when the offered price differences on the market are examined one observes that they range from lowest to highest easily between +/-50%. The technical reasons for this phenomenon will be illustrated in the next section (Figure 3).

Figure 1 shows the development of prices over the years for the main panel of insurers on the Swiss market as a representative sample of risks. The average price across this sample is shown, together with the average of the lowest prices. The yellow line shows their relativity (so the average lowest price is about 23% lower than the market average in summer 2013). What this implies is that, unless the average in the market is unnecessarily high and represents the true average of real policies, we could expect a drop in price of more than 20% if clients consequently would go for their cheapest options. Luckily, in Switzerland this is not yet the case because combined ratios are still far below 100% and cancellation rates are single digit percentages, but both figures show a slight negative tendency in recent years.

Should actuaries really go for more price differentiation, and if so how?

About three years ago, I had some personal experience when I wanted to explain multivariate pricing to sales agents. I wanted to explain the price differences on the Internet and outlined the methods, such as the generalized linear model (GLM). At the end of the meeting, I could only tell them that I use the best possible methods at the moment. Unfortunately those methods produce the variances, as happens across the market, which means we have to accept them for a current lack of anything better.

In fact, all actuaries tell that to stakeholders and almost all companies claim that they use “best practice” in pricing. Actuaries are closest to this problem and hence need to take the first step toward a solution. From that moment I started questioning my own practices.

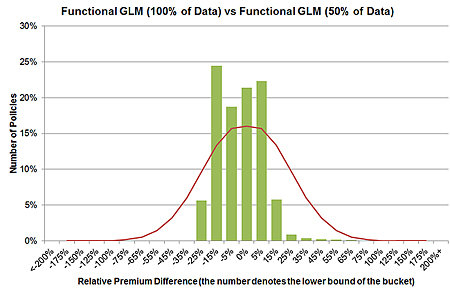

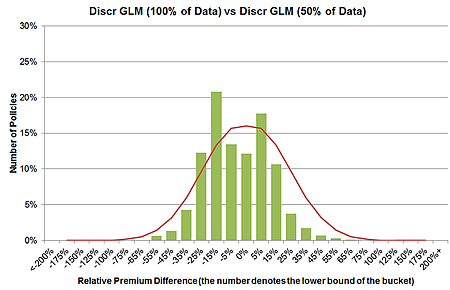

As a result, I had to admit that the granularity we usually produce in our technical prices may be too high, even when using clever and minimal pricing parameters. As a result, consider the induced relative price changes that occur when randomly reducing the data size by some percentage on which the model was built. This applies to a small portfolio—which is the size some insurers have to deal with to produce a rating scheme similar to bigger market players, and with this they can easily spoil the market. As a consequence, actuaries need to get hold of market price data to be able to relate and reason their pricing from this angle next to a very serious multivariate analysis and reasonably granular technical premiums. Of course, how one would get enough of such market prices is a different story.

The main cause for the variance in results among the statistical methods is due to the fact that actuaries usually look at the overall goodness of fit criteria, which helps reduce the total variance instead of the individual variance in each price cell. Often those criteria are “just” satisfactory. Furthermore, all those fitness criteria that explain the variance and give estimates of the model error assume that the models are right. In fact, there is an almost infinite number of competing models that all can produce substantially different results in individual pricing cells. This means that the multivariate methods themselves may not solve this problem of instability. It may be the case that looking much more to the market is more what's called for here. Knowing the market prices could add an extra stabilization to the insurers pricing model and would also reduce the current market irritations for sales agents and clients alike, resulting in more trust and loyalty.

What else can insurers do to stabilize their pricing?

Over the next couple of years, insurers will have to gain more insight into market pricing in order to establish a level playing field with clients. Already they often have market price analytics teams that either do mystery shopping or run some sort of crawling software to check a limited number of profiles on the Internet. However, knowing the market only for a few hundred or a few thousand profiles is not sufficient when dealing with a few million pricing cells.

Another way to receive prices is from broker platforms, although recently an interesting and almost unique service of this kind was prohibited by the German insurance authority for antitrust reasons. In Germany, a popular brokerage platform, NAFI, has offered insurers an extraction of competitor prices for whole risk portfolios in a batch process. That made it possible to retrieve almost complete rating plans of market players from this data. What this will imply for the German market, which so far has had acceptable combined ratios (around 100%), will become apparent in the next years. If the existence of the NAFI service has led to a reduction in price variance for Germany, it is possible that the market in Germany will become more like the one in the U.K.

Conclusions

Knowing what a market does in detail will certainly keep variances within a range. Further, not having this information will even increase variation in the future; consequently, well-informed clients will be able to take advantage. Insurers should be prepared, instead of hoping that clients remain uninformed and blindly loyal.